20 October 2016

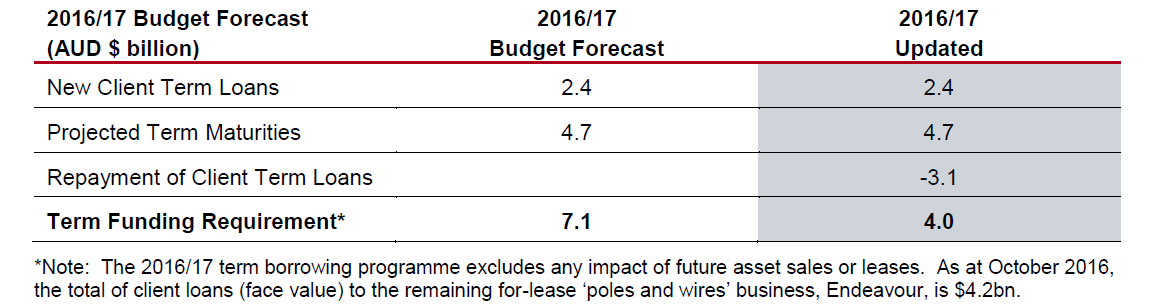

Now Ausgrid has been leased, it has repaid $9.5 billion of loans formerly provided by TCorp. As such TCorp’s funding requirement for 2016/2017 has just been substantially reduced. In June, it estimated it would require $7.1 billion to cover maturing bonds and other shortfalls of the NSW Government. This figures has now been reduced to $4.0 billion, with the balance of the $9.5 billion used to repay the NSW Government $4 billion while $2 billion less is borrowed in the short term market.

While TCorp will not be conducting any more buybacks of ordinary bonds, it did say it would seek to repurchase about $150 million 2020 index-linked bonds. It has also made it known it wishes to lengthen the duration of the bonds it has outstanding and is thus open to reverse enquiries.

TCorp’s next funding update will be in mid-December.

19 October 2016

Central banks around the world want higher inflation and they are doing their best to create it with a suite of measures. Ultra-low interest rates and injections of new cash in exchange for bonds have been used to stimulate investment and consumer spending in the economies of the US, Europe, the UK and Japan. Whether these policies have been or will be successful is a matter for debate but so far, only the US has halted additional bond purchases and only after USD$3.7 trillion was injected into its economy over the past eight years.

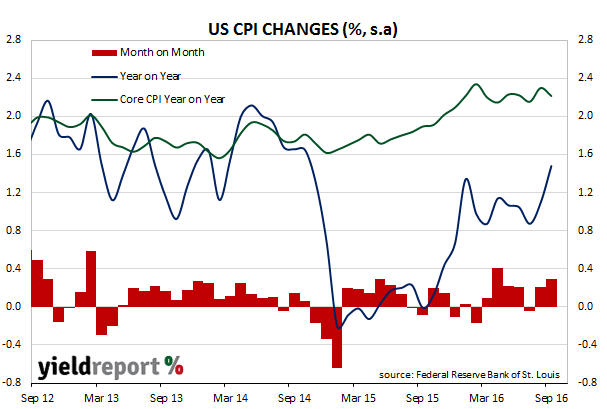

Monthly inflation figures are the scoreboard, so to speak, measuring whether central banks are winning or not and in the US, the game is still in progress. September CPI figures released by the Bureau of Labor Statistics indicate consumer prices rose 0.3% for the month, 1.5% for the year and in line with market forecasts. Core prices, the measure of prices which strips out food and energy prices changes, rose 0.1% for the month, which is less than expected. Over the last 12 months, core inflation slipped from August’s 2.3% to 2.2% (seasonally adjusted).

According to the Bureau, the rise in the overall price level was driven by housing costs and fuel prices, with fuel accounting for half of the overall rise. In the core CPI measure, prescription drug prices had the largest increase at 0.8% for the month. ANZ Research viewed the figures as “good news for the FOMC achieving its dual mandate” but Westpac was less positive and said the figures were “slightly disappointing” as the core measure of CPI was lower than the previous month.

US yields initially rose on the news but finished the day lower. The US 2 year yield fell 2bps to 0.80% and 10 year yield finished 3bps lower at 1.74%. The USD was slightly higher against other currencies, which is the currency markets’ way of implying a higher probability on US rate rises but cash markets contract implied a slightly lower probability of a rate rise at December’s FOMC meeting.

18 October 2016

Although the minutes of the October RBA meeting were not expected to provide much in the way of news, observers were looking forward to hints and clues as to how the views of new Governor Lowe would differ from his predecessor.

The short answer; not much. However, there was the odd section which was noteworthy. Westpac chief economist Bill Evans pointed to the part of the minutes regarding underemployment, which is a theme which has emerged this year, both here and in the US. “The minutes point out that even though the unemployment rate has fallen by half a percentage point over the past year the underemployment rate, which captures workers who would like to work more hours, has increased.” He also noted then reference to the next CPI report out at the end of October. “Explicitly recognising the upcoming inflation report is not a standard approach. Certainly it was referred to explicitly in the July minutes when we were clearly conditioned to see the June quarter inflation report as critical to the August policy decision.…We have not been of the view that the next inflation report will have the same significance.”

Here’s what the economists said:

Bill Evans, Westpac

Less emphasis on specific inflation targeting and direct consideration of the implications of policy for housing and labour markets is clearly spelled out. Based on the Governor’s apparent uncertainty around housing and the labour market at the moment it is clear that he would not welcome a sharp negative surprise on current inflation. We do not think that such an outcome is at all likely and we also believe that his tolerance for a very low number will be high but not infinite.

Commonwealth Bank Global Markets Research

The Governor will be keeping his eye on the labour market and the housing market, but at the end of the day, the RBA still targets CPI. And with neither the labour market nor the housing market actively suggesting a further rate cut would be deleterious, the RBA will be forced to lower the cash rate further to shorten the long wait.

Jo Horton, St George

The minutes of the RBA’s October board meeting highlighted the need to look carefully at the CPI data due on 26th October. A downward shock would raise the prospect of a November or December rate cut. A benign outcome could take rate cuts in 2016 off the table. The RBA believes that under its current settings there is “a reasonable prospect of sustaining growth in economic activity that would support further employment growth and, in time, a gradual increase in wage growth and inflation.” We have our doubts.

18 October 2016

Challenger, the funds management and annuities company, is planning another issue of Additional Tier 1 capital notes to add to its existing Notes (ASX code: CGFPA) which are already listed on the ASX. In a September quarter update to the market, Challenger said it would issue AT1 capital notes before June 2017, subject to market conditions.

Challenger is required by APRA to have a minimum amount of capital for each dollar of assets in its life business. The company prefers to keep this ratio in the range 1.3 to 1.6 times APRA’s minimum requirement and as its life business is growing, additional capital will be necessary.

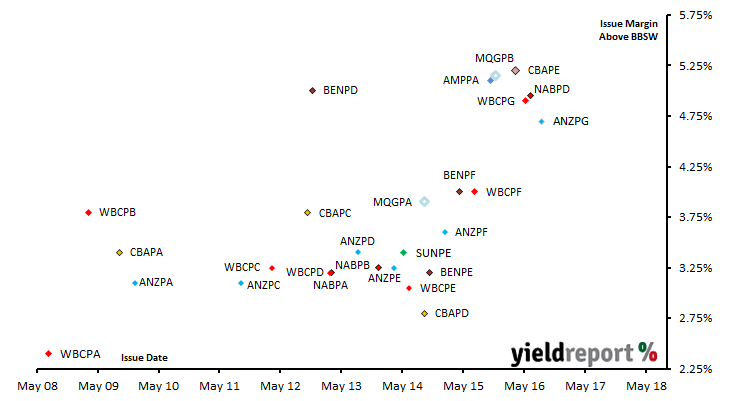

Its existing capital notes (ASX code: CGFPA) were issued in 2014 at a margin of 340bps over 3m BBSW. Challenger’s senior debt is rated BBB+ by S&P Global Ratings. AA- issuers have issued AT1 securities with margins between 470bps (ANZPG) and 495bps (NABPD), so unless conditions change substantially between now and the end of June, Challenger can expect its second hybrid to warrant a much higher margin than the first.

13 October 2016

The September minutes of the FOMC confirmed a rate increase this year is more likely, although most market pundits think a rise before the US presidential election is out of the question. “The Committee judges that the case for an increase in the federal funds rate has strengthened but decided, for the time being, to wait for further evidence of continued progress toward its objectives.” However, there was not much new in what the minutes said. As ANZ put it “Overall, the minutes provided little new news, and are therefore unlikely to result in the market taking the chances of a November hike any more seriously, but they also provided nothing to stand in the way of the current market moves, ie: increasingly pricing-in a December hike but being a little nervous about it.”

What was unusual was the level of disagreement within the committee. Almost everyone on the FOMC agrees a rate increase is coming but those who wish to delay think there is more spare capacity in the labour market and those who argued for a rate increase think the labour market is close to full employment. Three members want a 25bps increase immediately and they are worried FOMC credibility is being eroded. According to the minutes “several participants expressed concern that continuing to delay an increase in the target range implied a further divergence from policy benchmarks based on the Committee’s past behavior (sic) or risked eroding its credibility…” However, Westpac took the view signs of dissent would not change the Fed’s intended path for interest rates. “All in all, the above tension amongst FOMC members means little for our expectation that December will see a 25bp hike.”

13 October 2016

StockCo, a New Zealand agriculture finance business, has raised $30 million via the issue of October 2022 subordinated notes securities. It joins a growing number of companies without credit ratings which have raised funds by issuing high yield bonds in Australia. As interest rates have fallen, some investors have been willing to take on more risk in exchange for a higher rate of interest. This latest bond issue has come at a time when investors are hard-pressed to find yields which will satisfy their income requirements.

StockCo’s notes have an 8.75% coupon which is within the 7.50% – 9.00% range established over the last two years by similar unrated issuers. The notes are callable by StockCo on interest payment dates in 2019 at $103, 2020 at $101.50 and 2021 at par ($100) and a 0.75% step-up will apply if not called by October 2021. The proceeds from the notes’ sale will be used for working capital as StockCo expands its Australian operations.

12 October 2016

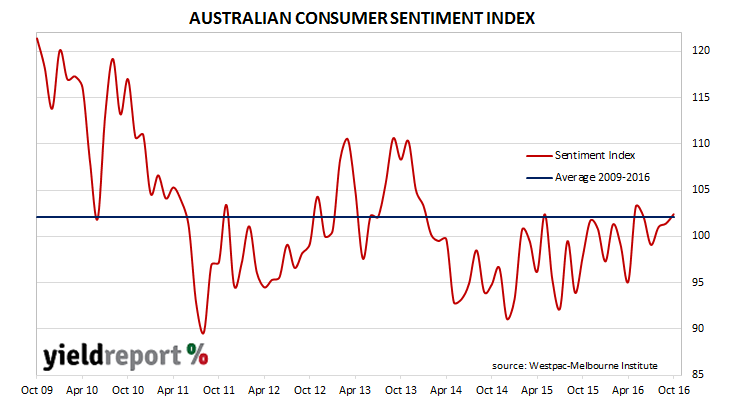

Consumer confidence has extended a “remarkable run of stability” through to October as optimists still slightly outweigh pessimists, according to the latest consumer survey. The October Westpac-Melbourne Institute consumer sentiment index rose from September’s reading of 101.4 to 102.4. Any reading above 100 indicates the number of consumers who are optimistic is more than the number of consumers who are pessimistic.

Westpac’s chief economist Bill Evans pointed to one segment of the survey which stood out. “The Current Conditions components of the Index have been steady while the Expectations components of the Index are up 8.1% on the previous year…The largest average boost of the components has been the outlook for the economy over the next 12 months.” He put it down to stable labour market conditions and pointed to a drop in the Unemployment Index which indicated a marked improvement in employees’ views of labour market conditions.

The result was not a surprise to financial markets although the AUD rose marginally against the major currencies on the day and the probability of a February rate cut fell from 26% to 20%. Bond market yields were already up before the figures were released on the back of large rises offshore. By the end of the day the 3 year bond yield was 5bps higher at 1.71% and the 10 year rate was up 6bps at 2.28%.

12 October 2016

Plans for the issue of the Australian government’s first 30 year fixed rate bond have finally come to fruition. Today, the Australian Office of Financial Management (AOFM) announced it had issued bonds worth $7.6 billion in face value terms with a maturity date March 2047. The bonds were priced with a yield to maturity of 3.27% (or EFP + 101bps) and reported to have attracted over $13 billion of orders.

The AOFM made its intentions of extending the Australian Commonwealth yield curve public in May 2015 but little occurred until August this year when the possibility re-emerged. That possibility resolved into a certainty when the AOFM mandated local and foreign banks to arrange buyers of the bonds yesterday.

There has been talk this bond sale led some investors to sell out of other long-dated bonds in order to finance taking part. 10 year and 20 year bond yields have been rising around the world but comparable yields in Australia have moved further, steepening our yield curve. Perhaps with this in mind, the AOFM said there would be no further issuance prior to March 2017, signalling to bond holders there would not be a need to make switching arrangements for some time but also to allow the new benchmark sized issue time to settle in secondary market trading.

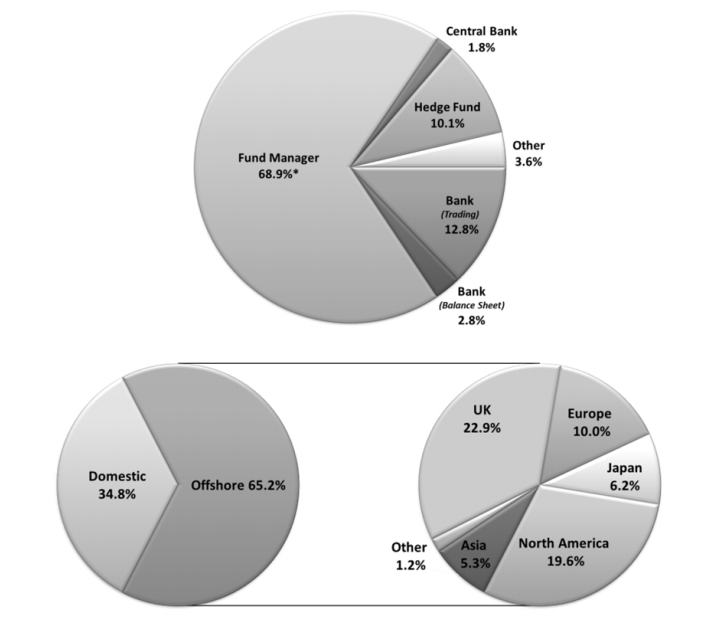

The new bonds will be a boon for insurance and life offices which have long term liabilities and struggle to find matching assets. It is highly likely many of these bonds will be tucked away in portfolios never to see the light of day. Nearly 70% of the bonds were purchased by investors defined by the AOFM as asset managers, insurers and pension funds.

There has been a concerted push for Australia to lengthen its debt profile with interest rates at or near record lows. Many countries have already done so, including Mexico and Ireland, both of which issued 100 year bonds in the past 18 months. It makes sense for governments to borrow money for long periods at low rates and yield-hungry investors have been keen to snap up sovereign debt, almost at any price.

Related articles

Aussie 30 year bond to debut

New Aussie 30 year bond is nearly here

11 October 2016

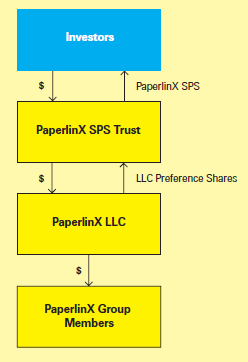

At the 2015 AGM of PaperlinX, now known as Spicers, the chairman stated the company was seeking an agreement between equity holders and step-up preference unit (SPS) holders. SPS holders had been attempting to enforce what they see as their right to conversion into ordinary shares at a ratio which would add over 7 billion additional shares to the 665 million already on issue – a massive ten times increase. The issue of so many new ordinary shares would dilute existing shareholders and thus met with huge resistance from the board.

This week the company made a compromise proposal, one which would lead to SPS holders controlling 70% of the company if it were accepted. SPS holders would exchange each of their units for 545 newly-issued ordinary shares in a deal with is similar to a debt-for–equity arrangement. At a price of 2.5 cents per ordinary share, the offer equates to $13.625 per SPS, well up on the previous closing price but a long way from the $100 worth of shares to which some SPS holders said they were entitled.

Prior to the proposal, the last sale price was $9.00 and the units have been trading at between $6 and $16 from some years now. The market has not placed a high probability of conversion at $100 and, although the units immediately jumped to a price of $13.45 (11 October) upon the ASX announcement, the large discount to $100 still indicates such an outcome is not given much weighting.

SPS units were issued from the PaperlinX SPS Trust. Perpetual is the responsible entity for the SPS Trust and it has advised holders to do nothing until it has properly considered the proposal. Perpetual said an independent expert review and a vote of unit holders will be required.

source: 2007 PaperlinX Step-up Preference Share product disclosure statement

11 October 2016

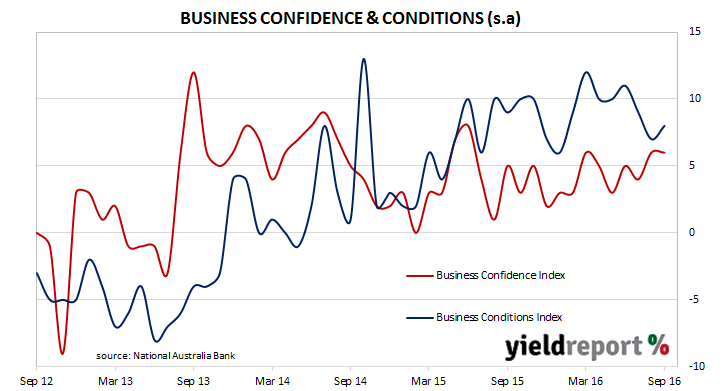

Australian businesses sentiment remained at elevated levels in September, as business conditions improved slightly and despite a deterioration in retailing conditions. In NAB’s latest monthly business survey, the Business Conditions Index moved 1 point higher to 8 while the Business Confidence Index remained at 6.

In August NAB’s chief economist Alan Oster said the bank had changed its view on official interest rates over the next 12-18 months on the basis GDP growth is likely to slow, following a deterioration in conditions in the transport and wholesale sectors. This month NAB’s head of Australian Economics, Riki Polygenis, referred to any strength in business conditions as becoming “increasingly narrow-based”, while conditions in specific parts of the economy were troubling. “The recent deterioration in retail conditions is of particular concern given the implications for consumption, the largest component of domestic demand.”

The NAB Group Economics team remains of the view Australia is due for an economic slowdown which will persuade the RBA to hand out rate cuts in 2017. “Beyond the near-term, we still expect the economy to slow into 2018 as momentum from commodity exports, housing construction and AUD depreciation is lost. Ongoing low inflation combined with a more subdued growth outlook is expected to jolt the RBA into action, cutting the cash rate by 25bp two more times in H2 2017.”