12 April 2022

Summary: Business conditions improve markedly in March; confidence also improves; conditions index largely driven by retail; further escalation of cost pressures, including labour costs; businesses no longer absorbing cost increases; capacity utilisation rate up, 7 of 8 sectors of economy at/above respective long-run averages.

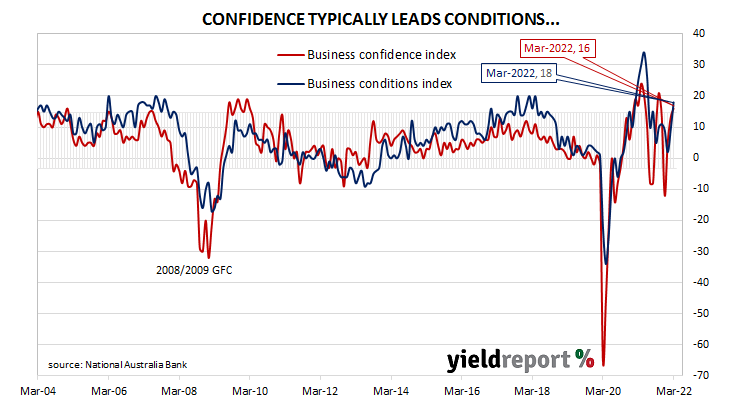

NAB’s business survey indicated Australian business conditions were robust in the first half of 2018, with a cyclical-peak reached in April of that year. Readings from NAB’s index then began to slip and forecasts of a slowdown in the domestic economy began to emerge in the first half of 2019 as the index trended lower. It hit a nadir in April 2020 as pandemic restrictions were introduced but then conditions improved markedly over the next twelve months. More normal readings have been present since.

According to NAB’s latest monthly business survey of over 400 firms conducted over the last week and a half of March, business conditions have improved markedly. NAB’s conditions index registered 18, up from February’s reading of 9.

NAB senior economist Brody Viney said the rise in the index “was largely driven” by retail businesses while the recreation and personal services, finance, business and property sectors also contributed.

Business confidence also improved. NAB’s confidence index rose from February’s reading of 13 to 16, well above the long-term average. Typically, NAB’s confidence index leads the conditions index by approximately one month, although some divergences have appeared in the past from time to time.

Commonwealth Government bond yields increased moderately on the day. By the close of business, the 3-year ACGB yield had added 4bps to 2.76%, the 10-year yield had gained 7bps to 3.14% while the 20-year yield finished 8bps higher at 3.41%.

In the cash futures market, expectations of any material change in the actual cash rate, currently at 0.06%, eased slightly. At the end of the day, contract prices implied the cash rate would not exceed the RBA’s 0.10% target rate until May and then rise to 0.81% by August. February 2023 contracts implied a cash rate of 2.245%.

“The Australian economy improved further in March, with both business conditions and business confidence up. The downside is that this is associated with a further escalation of cost and price pressures, including labour costs,” said Westpac senior economist Andrew Hanlan.

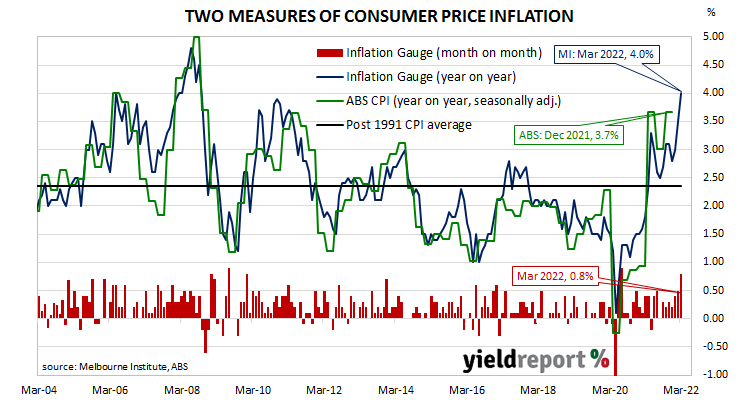

Cost pressures featured prominently in the NAB report. “Cost growth escalated further in the month, with labour-cost growth hitting 2.7% in quarterly terms and purchase-cost growth up to 4.2%, both tracking at considerably higher rates than at any other point in the history of the survey.”

Those pressures have begun to flow through to customers and ANZ senior economist Catherine Birch attributed this to two factors. “Firstly, some businesses have reached the point where they can no longer absorb cost increases. Secondly, with households expecting higher inflation and more businesses prepared to lift their prices, there is less risk of an individual business losing customers or market share due to a price rise.”

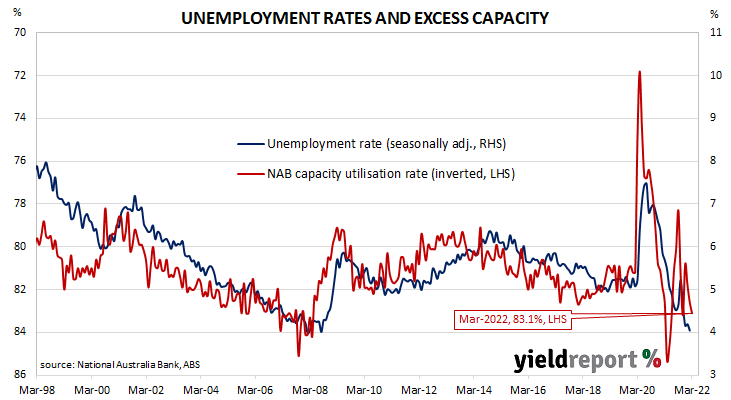

NAB’s measure of national capacity utilisation continued to recover from December’s drop and it rose from February’s revised figure of 82.6% to 83.1%. Seven of the eight sectors of the economy were reported to be operating at or above their respective long-run averages. The Recreation/Personal Services sector was the exception.

Capacity utilisation is generally accepted as an indicator of future investment expenditure and it also has a strong inverse relationship with the unemployment rate.