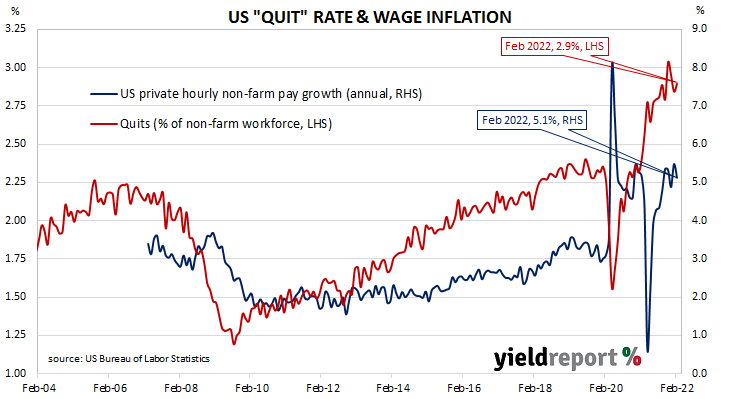

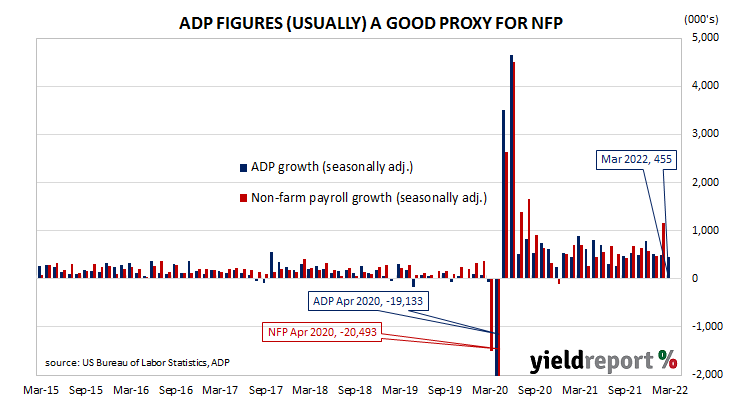

Summary: ADP payrolls up 455,000 in March; greater than consensus expectations; February rise revised up by 11,000; suggests high inflation, Russia-Ukraine war, haven’t dented employment growth yet; positions up in businesses of all sizes; little over 80% of gains in services sector, led by leisure/hospitality sector.

The ADP National Employment Report is a monthly report which provides an estimate of US non-farm employment in the private sector. Since publishing of the report began in 2006, its employment figures have exhibited a high correlation with official non-farm payroll figures, although a large difference can arise in any individual month.

The latest ADP report indicated private sector employment increased by 455,000 in March, greater than the 413,000 increase which had been generally expected. February’s rise was revised up by 11,000.

“Jobs growth is broad-based across goods and services industries and it suggests that high inflation and the Russia-Ukraine war haven’t dented employment growth yet,” said ANZ economist John Bromhead.

Treasury bond yields fell on the day. At the close of business, the 2-year Treasury bond yield had shed 6bps to 2.31%, the 10-year yield had lost 5bps to 2.35% while the 30-year yield finished 2bps lower at 2.48%.

In terms of US Fed policy, expectations for higher federal funds rates over the next 12 months firmed considerably. At the close of business, May contracts implied an effective federal funds rate of 0.72%, 39bps higher than the current spot rate. July contracts implied 1.235% and March 2023 futures contracts implied an effective federal funds rate of 2.65%, 232bps above the spot rate.

Employment numbers in net terms increased across businesses of all sizes. Firms with less than 50 employees gained a net 90,000 positions, mid-sized firms (50-499 employees) added 188,000 positions while large businesses (500 or more employees) accounted for 177,000 more employees.

Employment at service providers accounted for a little over 88% of the total net increase, or 377,000 positions. The “Leisure & Hospitality” sector was the largest single source of gains, with 161,000 more positions. The “Education & Health” and “Professional & Business” sectors were also significant sources, each adding 72,000 positions and 61,000 positions respectively. Total jobs among goods producers increased by a net 79,000 positions.

Prior to the ADP report, the consensus estimate of the change in March’s official non-farm employment figure was +450,000. The non-farm payroll report will be released by the Bureau of Labor Statistics this coming Friday night (AEST), 1 April.