Summary: Number of home loan approvals up 4.0% in November; value of loan commitments up 6.3%; approvals excluding refinancing near record highs; ANZ expects rate rises to trigger material fall in lending eventually; value of owner-occupier loan approvals up 7.6%, investor approvals up 3.8%; rate rises to trigger “material fall in lending” eventually.

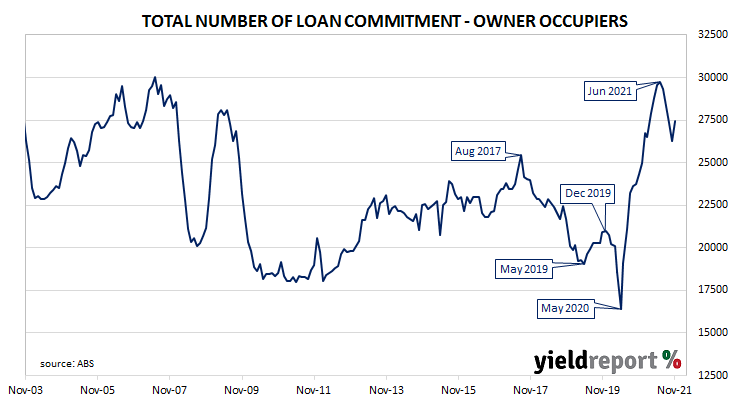

After the RBA reduced its cash rate target in a series of cuts beginning in mid-2019 the number and value of approvals began to noticeably increase, potentially ending the downtrend which had been in place since mid-2017. Figures from February through to May of 2020 provided an indication the downtrend was still intact but subsequent figures then pushed both back to elevated levels.

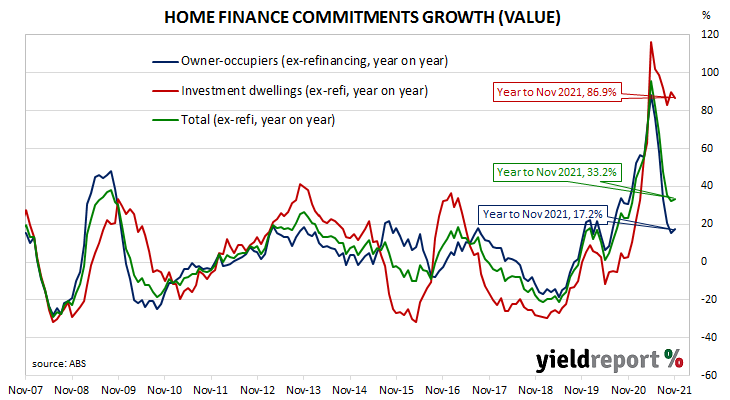

November’s housing finance figures have now been released and the total number of loan commitments (excluding refinancing loans) to owner-occupiers increased by 4.0%. The rise reversed October’s 4% fall and took the annual growth rate from October’s figure of 0.6% to 1.0%.

Commonwealth Government bond yields finished the day higher at the short end but lower elsewhere. By the close of business, the 3-year ACGB yield had added 3bps to 1.29% while the 10-year yield had slipped 1bp to 1.88% and the 20-year yield had lost 2bps to 2.40%.

In dollar terms, total loan approvals excluding refinancing increased by 6.3% over the month, considerably more than the 0.4% rise which had been generally expected and in contrast with October’s -2.5%. On a year-on-year basis, total approvals excluding refinancing increased by 33.2%, marginally faster than the previous month’s comparable figure of 32.2%.

“Overall housing finance approvals excluding refinancing are near record highs and are an incredible 64.4% above their pre-pandemic February 2020 levels. The composition of loans has tilted slightly towards a greater investor share, though the investor share overall at 32% is still below the historical average of 36%,” said NAB senior economist Tapas Strickland.

ANZ senior economist Adelaide Timbrell said ANZ expects rate rises “to eventually trigger a material fall in lending”, noting fixed mortgage rates “are already rising”.

The total value of owner-occupier loan commitments excluding refinancing increased by 7.6%, in contrast to October’s -4.1%. On an annual basis, owner-occupier loan commitments were 17.2% higher than in November 2020, whereas October’s annual growth figure was 15.1%.

The total value of investor commitments excluding refinancing arrangements increased by 3.8%. The rise follows a 1.1% increase in October and it is the thirteenth month of consecutive gains since the last monthly decline in October 2020. On an annual basis, the value of loan commitments in the month was 86.9% higher than in November 2020, down from 89.6% in October.