Summary: Leading index growth rate unchanged in October; in negative territory for two consecutive months but index holds up “quite well”; non-lockdown states operating above trend, global backdrop much more supportive; reading implies annual GDP growth of 2.25% during December/March quarters; Westpac maintains growth forecasts.

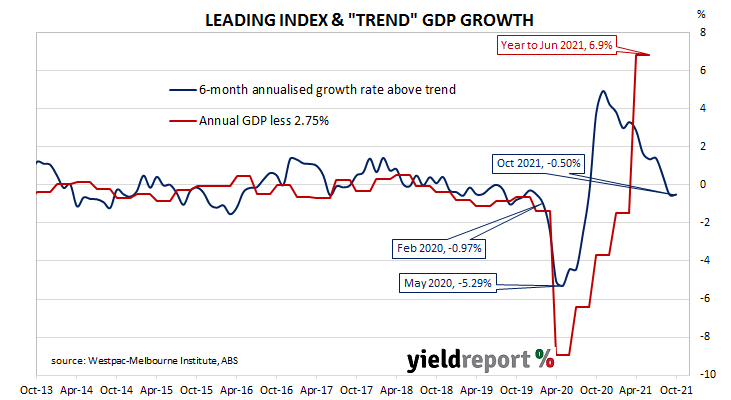

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic growth in the short-term. After reaching a peak in early 2018, the index trended lower through 2018 and 2019 before plunging to recessionary levels in the second quarter of 2020. Subsequent readings were markedly higher but more-recent readings have steadily declined.

The latest reading of the six month annualised growth rate of the indicator registered -0.50%, unchanged from September’s reading.

“The Index growth rate has now been in negative territory for two consecutive months. Given that our two major cities were locked down for most of the September quarter and into October the Index has held up quite well,” said Westpac Chief Economist Bill Evans.

Index figures represent rates relative to “trend” GDP growth, which is generally thought to be around 2.75% per annum. The index is said to lead GDP by up to nine months, so theoretically the current reading represents an annual GDP growth rate of around 2.25% in the first or second quarters of 2022.

Domestic Treasury bond yields generally moved lower on the day, although ultra-long yield did rise noticeably. By the close of business, the 2-year ACGB yield had lost 3bps to 1.17%, the 10-year yield had slipped 1bp to 1.85% while the 20-year yield finished 5bps higher at 2.41%.

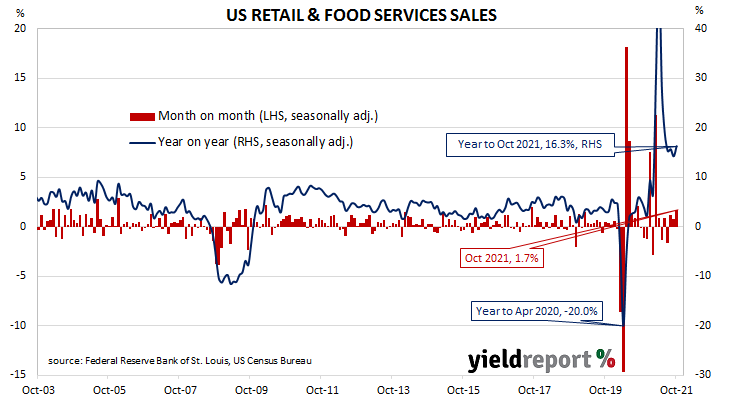

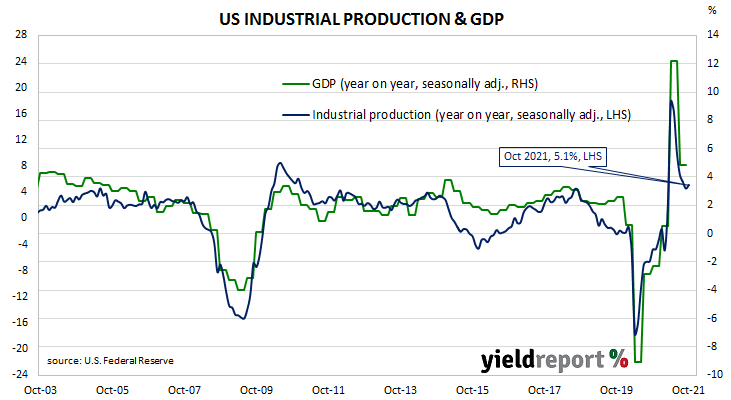

“One key consideration has been that, despite these lockdowns, the rest of the country has been operating above trend,” said Evans. He also pointed to other positive factors on the Index, such as higher US industrial production, noting the “global backdrop has also been much more supportive” than it was in 2020.

Westpac maintained its GDP growth forecasts for the September and December quarters at -4.0% and +1.6% respectively. Westpac still expects a 7.4% growth rate over calendar 2022.