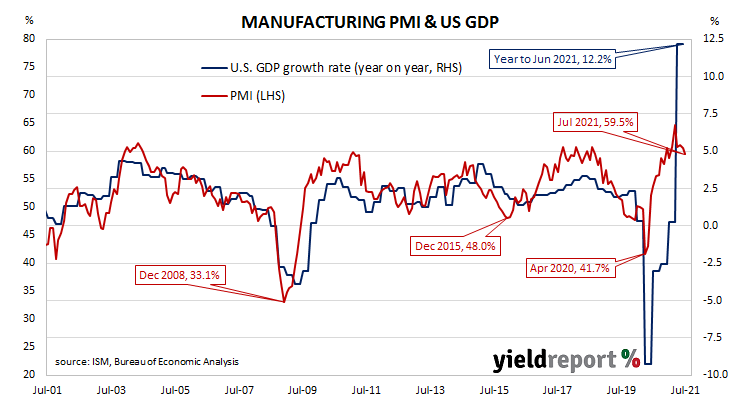

Summary: ISM PMI falls from 60.6% to 59.5% in July, slightly below consensus expectation; companies, suppliers struggle to meet increasing demand levels; US Treasury market reaction suggests concern over ‘peak growth’, more slowdown ahead; various factors imposing limits on manufacturing sector; latest reading implies 4.7% 12-month GDP growth rate in December.

The ISM’s purchasing managers’ index (PMI) reached a cyclical peak in September 2017. It then started a downtrend which ended in March 2020 with a contraction in US manufacturing which lasted until June 2020. Subsequent month’s readings implied growth had resumed before becoming stronger through the early months of 2021.

According to the latest Institute of Supply Management (ISM) survey, its Purchasing Managers Index recorded a reading of 59.5% in July. The result was slightly below the generally expected figure of 60.8% and slightly lower than June’s reading of 60.6%. The average reading since 1948 is 52.9% and any reading above 50% implies an expansion in the US manufacturing sector relative to the previous month.

The ISM’s Timothy Fiore said, “Business Survey Committee panellists reported that their companies and suppliers continue to struggle to meet increasing demand levels.”

Longer-term US Treasury bond yields fell on the day. By the close of business, the 10-year Treasury bond yield had shed 4bps to 1.19% and the 30-year yield had lost 3bps to 1.86%. The 2-year yield unchanged at 0.18%.

NAB currency strategist Rodrigo Catril said, “From a historic perspective a 59.5 manufacturing ISM reading is still a very robust activity reading. Nevertheless, reaction to the data release by the US Treasury market suggests the market is concerned over ‘peak growth’ and the potential for more slowdown ahead.”

Fiore pointed to various factors imposing limits on the US manufacturing sector, such as “near-record long raw-material lead times”, shortages of critical basic materials, transport difficulties, absenteeism and employee shortages. At the same time, he noted, “Optimistic panel sentiment remained strong, with 13 positive comments for every cautious comment.”

Purchasing managers’ indices (PMIs) are economic indicators derived from monthly surveys of executives in private-sector companies. They are diffusion indices, which means a reading of 50% represents no change from the previous period, while a reading under 50% implies respondents reported a deterioration on average. According to the ISM, a reading “above 42.8%, over a period of time, generally indicates an expansion of the overall economy.”