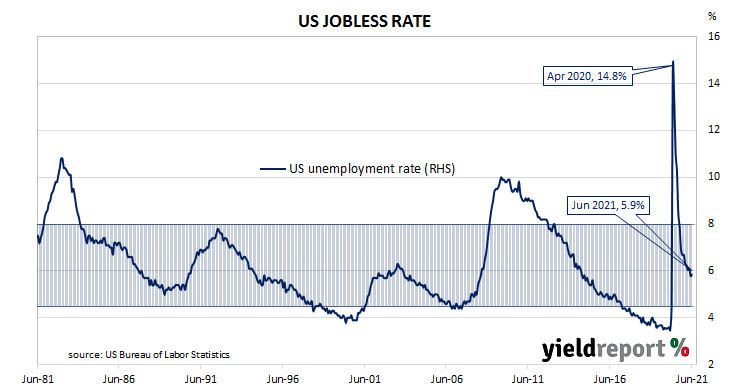

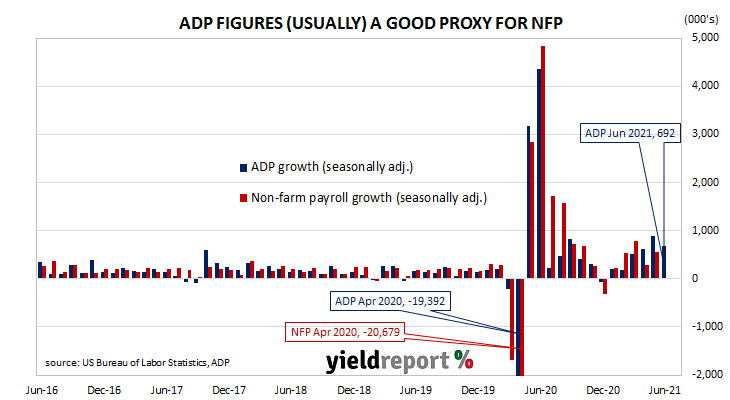

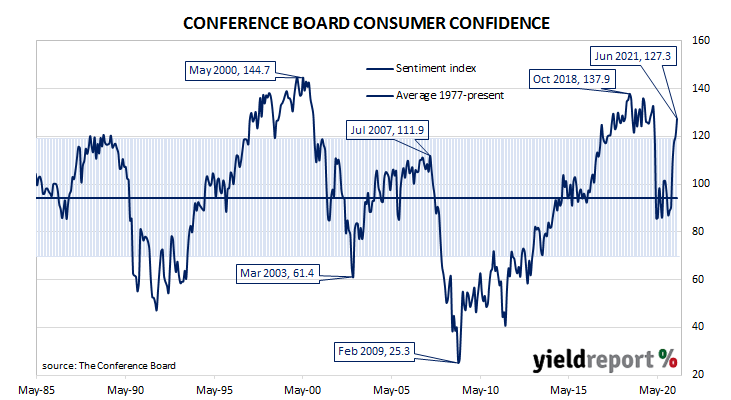

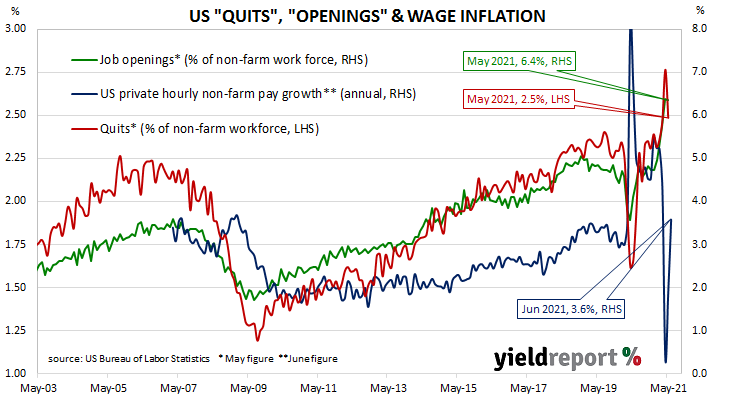

Summary: US quit rate falls back in May after hitting new high in April; quit rate “still elevated”; job openings up, separations down; “job matching” issues still evident.

The number of US employees who quit their jobs as a percentage of total employment increased slowly but steadily after the GFC. It peaked in March 2019 and then tracked sideways until virus containment measures were introduced in March 2020. The quit rate plummeted as alternative employment opportunities rapidly dried up but then recovered back to its pre-pandemic rate in the third quarter of 2020.

Figures released as part of the most recent JOLTS report show the quit rate fell back in May after it hit a new series high in April. 2.5% of the non-farm workforce left their jobs voluntarily, down from April’s 2.8% after it was revised up from 2.7%. There were 388,000 fewer quits but 533,000 more people employed in the non-farm sector in May.

ANZ economist Daniel Been described the 2.5% quit rate as “still elevated” and said people “with jobs are continuing to take advantage of the strong labour demand conditions to improve their position.”

Long-term US Treasury bond yields decreased moderately on the day. By the close of business, the 10-year Treasury yield had shed 3bps to 1.32% and the 30-year yield had lost 4bps to 1.94%. The 2-year yield finished unchanged at 0.22%.

The fall was led by 181,000 fewer quits in the “Professional and business services” sector while the “Accommodation and food services” sector experienced the greatest increase. Overall, the total number of quits for the month fell from April’s revised figure of 3.992 million to 3.604 million.

Total vacancies at the end of May increased by 16,000, or 0.2%, from April’s revised figure of 9.193 million to 9.209 million, driven by a 109,000 rise in the “Other services” sector, an 89,000 increase in the “Accommodation and food services” sector and 81,000 more openings in the “Healthcare/social services” sector. 100,000 fewer openings in the “Professional and business services” sector and 80,000 fewer openings in the “Arts, entertainment and recreation” sector provided the two largest offsets. Overall, 7 out of 18 sectors experienced more job openings than in the previous month.

Total separations decreased by 485,000, or 8.4%, from April’s revised figure of 5.803 million to 5.318 million. The fall was led by the “Professional and business services” sector, where there were 192,000 fewer separations than in April. Separations decreased in 13 out of 18 sectors.