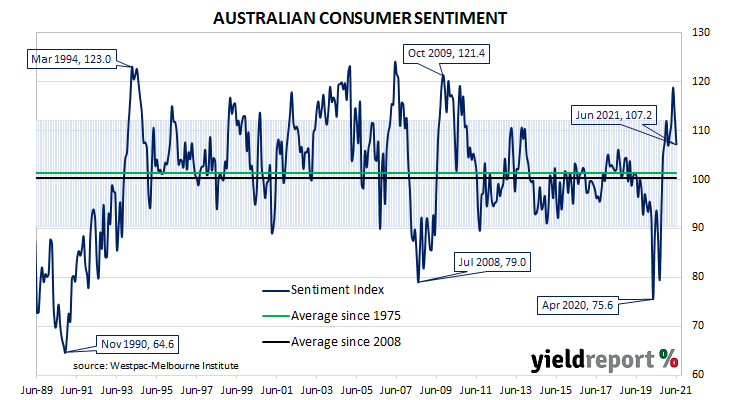

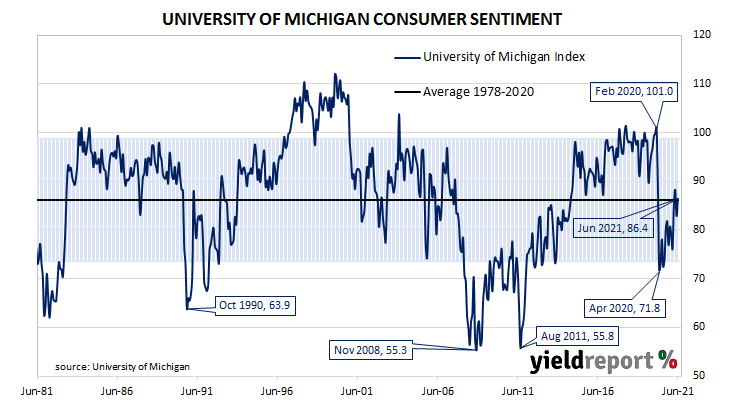

Summary: US consumer confidence improves in June; University of Michigan index above consensus figure; views of present conditions, future conditions both improve; driven by middle, upper income households, future economic prospects; stronger growth, lower unemployment rates generally expected; higher inflation rates “a top concern”.

US consumer confidence started 2020 at an elevated level. However, surveys had begun to reflect a growing uneasiness with the global spread of COVID-19 and its reach into the US by March of that year. After a plunge in the following month, household confidence recovered in a haphazard fashion, holding at below-average levels. While recent surveys suggested optimism may be about to rise, they have also tended to produce readings close to the long-term average.

The latest survey conducted by the University of Michigan indicates the average confidence level of US households improved in June. The University’s preliminary reading of its Index of Consumer Sentiment registered 86.4, above the generally expected figure of 83.8 and higher than May’s final figure of 82.9. Consumers’ views of current conditions and expectations regarding future conditions both improved in comparison to those held at the time of the May survey.

“The early June gain was mainly among middle and upper income households and for future economic prospects rather than current conditions,” said the University’s Surveys of Consumers chief economist, Richard Curtin.

Longer-term US Treasury bond yields moved a touch higher on the day. By the end of it, 10-year and 30-year Treasury yields had each crept up 1bp to 1.45% and 2.14% respectively. The 2-year yield finished unchanged at 0.15%.

Curtin noted respondents generally expected stronger growth, “with an all-time record number of consumers anticipating a net decline in unemployment.” However, higher inflation rates “remained a top concern of consumers, although the expected rate of inflation declined in early June.”

More-confident households are generally inclined to spend more and save less; some increase in household spending could be expected to follow. As private consumption expenditures account for a majority of GDP in advanced economies, a higher rate of household spending growth would flow through to higher GDP growth if other GDP components did not compensate.