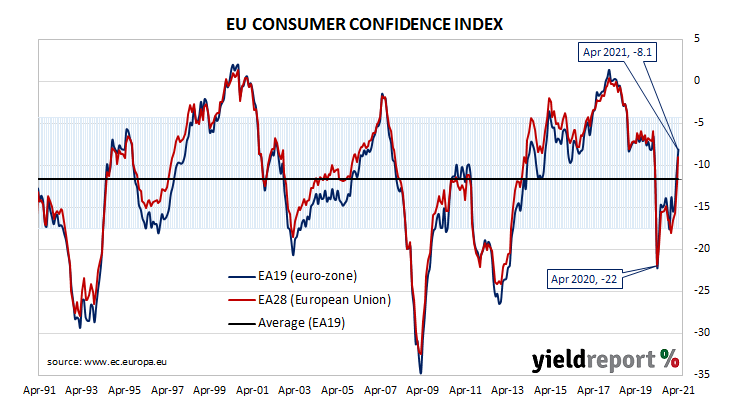

Summary: Euro-zone households more optimistic in April; back to pre-pandemic value; index above consensus expectation, long-term average; major euro-zone bond yields up a touch.

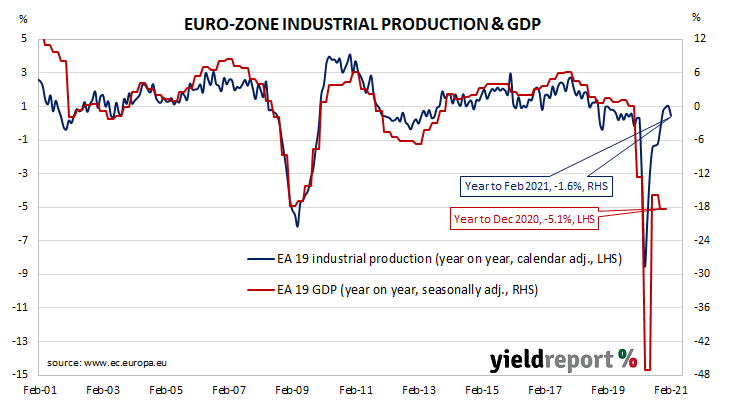

EU consumer confidence plunged during the GFC and again in 2011/12 during the European debt crisis. After bouncing back through 2013 and 2014, it fell back significantly in late 2018 but only to a level that corresponds to significant optimism among households. Following the plunge which took place in April 2020, a recovery began a month later, with household confidence returning to above-average levels in March.

The April survey conducted by the European Commission indicated its Consumer Confidence index increased to -8.1, a reading comparable with pre-pandemic values at the end of 2019. The reading was above -11.5 which had been generally expected and higher than March’s figure of -10.8. The average reading since the beginning of 1985 is -11.7.

Sovereign bond yields crept up in major European bond markets on the day. By the end of it, German and French 10-year bond yields had each ticked up 1bp to -0.25% and -0.01% respectively.