Interest Rate & Market Commentary for Week Ending 13th June 2025

Weekly Overview

U.S. stock indexes fell on Friday amid heightened anxiety in the Middle East, sending the market to a negative week overall. After recording gains the previous two weeks, the S&P 500 and the NASDAQ posted fractional weekly declines while the Dow finished down more than 1%.

A monthly report on U.S. consumer prices showed that inflation remained somewhat muted, which eased concerns about the potentially inflationary impact from elevated tariffs. On a month-to-month basis, the Consumer Price Index rose 0.1% in May, less than most economists had expected. The annual inflation rate was 2.4%—in line with expectations and near a four-year low recorded in April. The US Nonfarm Payrolls for May showed a monthly increase of 139,000, surpassing the forecast of 126,000, though slightly down from the previous month’s 147,000. The unemployment rate remained steady at 4.2%, aligning with both previous and forecasted figures. An auction of U.S. 30-year Treasury bonds generated stronger-than-expected demand from investors, easing government debt worries that recently sent the 30-year bond’s yield above 5.00%. Thursday’s auction drew a yield of 4.84%, below the 4.91% closing yield recorded on Wednesday.

U.S. Treasury yields fall to a one-month low in the wake of Israel’s strike on Iran’s nuclear facilities. The 10-year Treasury yield falls to 4.314% before recovering to last trade at 4.325%, still down 3 basis points on the day, according to Tradeweb. The 30-year Treasury yield has also hit a one-month low, falling to 4.802%, helped by solid demand at Thursday’s auction. It last trades at 4.817%, down 2.5 basis points, according to Tradeweb.

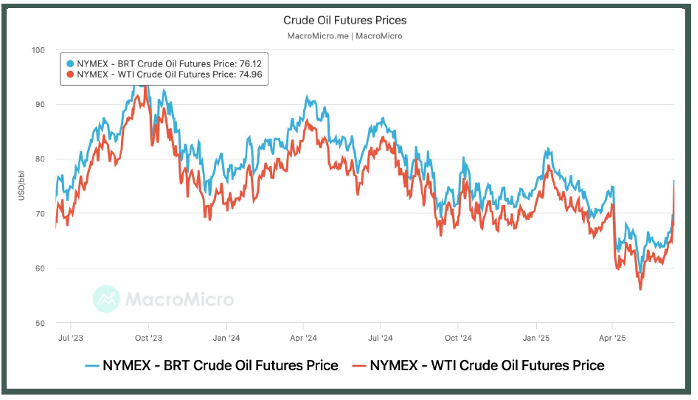

The price of U.S. crude oil surged more than 7% on Friday to the highest level in four months after Israeli military strikes on Iranian nuclear facilities raised the prospect of oil supply disruptions and renewed inflationary pressures for the broader economy. On Friday afternoon, oil was trading around $73 per barrel, up nearly 12% for the week.

The price of gold resumed its year-to-date climb, rising to new highs that eclipsed earlier records set in late April and early May. The precious metal was trading around $3,450 per ounce on Friday afternoon, up from about $3,320 at the end of the previous week and $2,600 at the end of last year.

Overview of the US Equities Market

The escalating conflict in the Middle East dragged stocks lower and sent oil prices surging on Friday, marking the latest geopolitical episode to rattle the markets this year. Stocks fell sharply after Israel launched a wide-ranging attack against Iran’s nuclear facilities and military leadership, and Tehran retaliated with drone strikes and missile barrages. The specter of a regional war and its potential disruption to global energy flows drove oil prices sharply higher. Iran is a major oil producer and strategically controls the northern side of the Strait of Hormuz, through which about a third of global seaborne oil flows. These developments make the Fed decisions that much more challenging because energy prices are just a different driver of inflation than what we’ve been focused on for the last six months.

The S&P 500 retreated 1.1%, while the Nasdaq Composite declined 1.3%. The Dow Jones Industrial Average lost 770 points, falling 1.8%. The CBOE Volatility Index—known as the VIX, or Wall Street’s fear gauge—jumped above 20, a sign of elevated investor anxiety. The index last skyrocketed in early April, after President Trump unveiled plans to impose tariffs on the rest of the world.

Brent crude rose over 7% to more than $74 a barrel. The U.S. oil gauge, West Texas Intermediate, advanced 7.3% to about $73 a barrel. Both logged their largest one-day percentage gains since the early days of the Russia-Ukraine war, according to Dow Jones Market Data. For the week, the S&P 500 and Nasdaq posted weekly declines of 0.4% and 0.6%, while the Dow shed 1.3%.

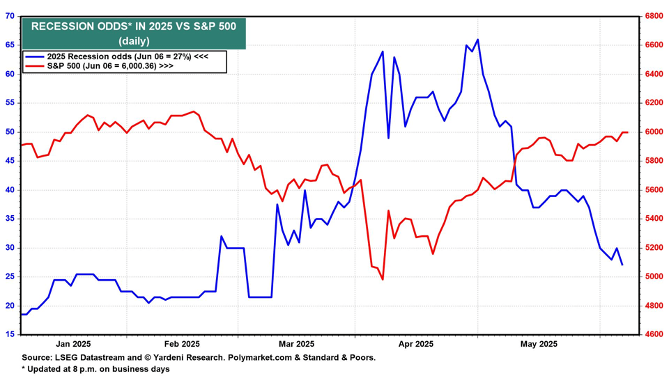

U.S. and Chinese officials discussed tariffs and other trade issues in a two-day session and reached a consensus on some of the key areas of dispute. Both sides said they’ll seek approval for the framework from the U.S. and Chinese presidents before implementing its terms. According to Polymarkets.com, the odds of a recession in 2025 rose from around 20% during January and February of this year to over 60% during March and April. On Friday, the odds were back down to 27%. Not surprisingly, the S&P 500 has been inversely correlated with the Polymarkets.com recession series.

Figure 1: US Recession Odds

Overview of the US Treasuries Market

The US Treasury bonds rallied last week, sending bond yields lower, as cool inflation reports from the Labour Department and another week of elevated jobless claims spurs hope of a Fed rate cut sooner rather than later—albeit not at the June meeting next week. The Treasury Department also notched solid auction results as it sells new bonds, a reassuring sign that, despite volatility this spring, demand for federal debt is holding up. On Friday, yields ticked higher despite a risk-off swing in other markets following Israel’s attack on Iran. The 10-year yield ends the week at 4.423%, up from 4.357% Thursday, and the 2-year yield finishes at 3.957%, compared with 3.904% on Thursday.

U.S. Treasury yields started Friday’s 13th session modestly higher, in relatively calm trading considering Israel’s attack on Iran. Israel’s attacks seem to have spared Iran’s oil infrastructure, a decision that could limit the conflict’s implications for the global economy, at least initially.Increasing attention to the possibility of a Fed rate cut amid some weaker data this week, although the market still deems a rate cut next week highly unlikely. The 10-year yield trades near 4.387%, versus 4.357%on Thursday, and the two-year yield is near 3.941%, up from 3.904% a day ago.

It’s widely expected that the U.S. Federal Reserve will keep interest rates unchanged again when it concludes a two-day meeting on Wednesday. However, rate cuts could still be coming; Friday’s prices in interest rate futures markets implied that most investors were expecting at least one to as many as three quarter-point rate cuts by year end.

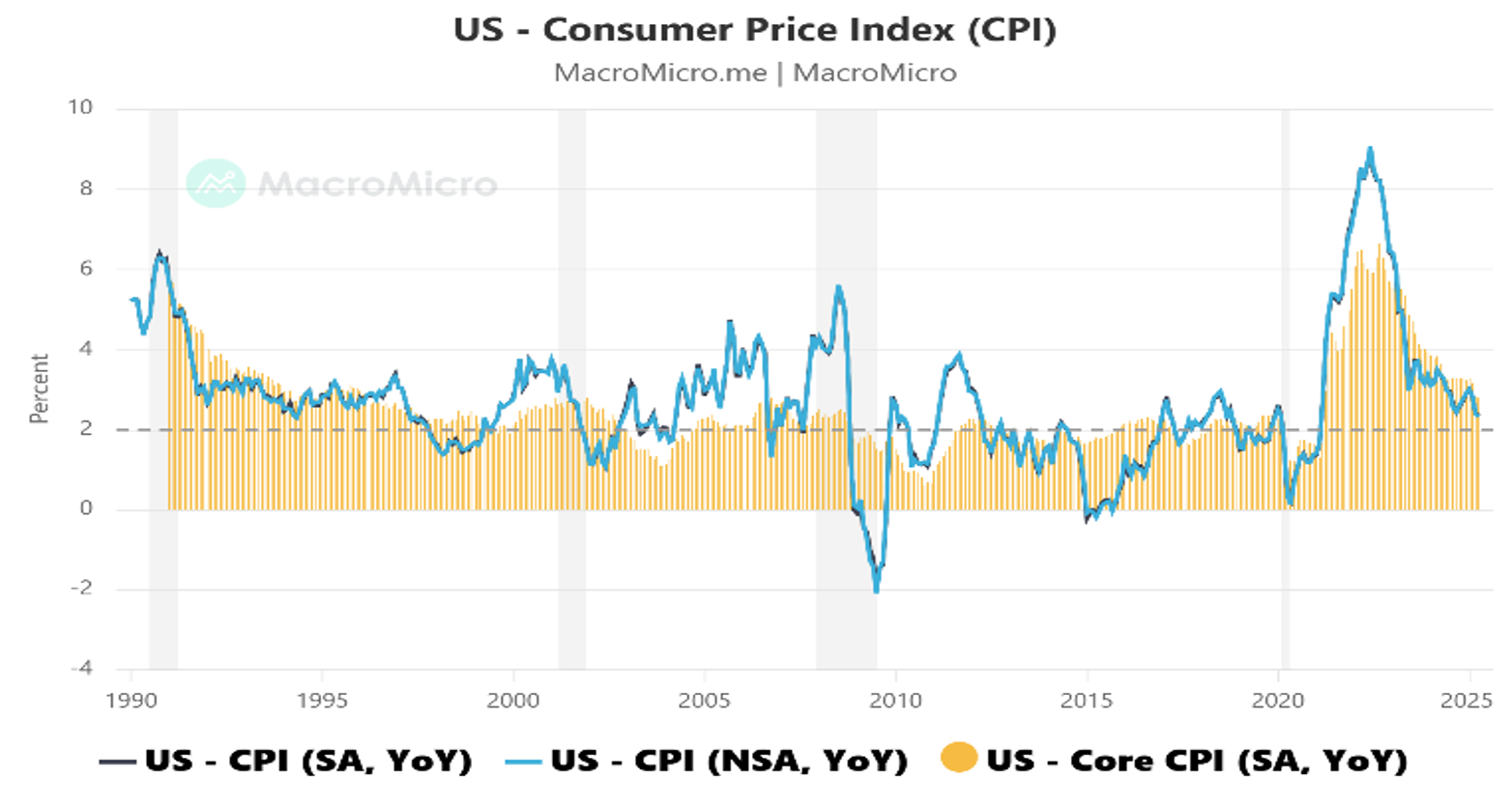

German 10-year Bunds have outperformed 10-year U.S. Treasurys by about 50 basis points since President Trump’s reciprocal tariff announcement early April. The US Consumer Price Index (CPI) for May revealed lower than anticipated inflation rates. The CPI (NSA, YoY) recorded a 2.35% increase, down from the forecasted 2.5% and slightly higher than the previous 2.31%. The CPI (SA, MoM) showed a 0.08% rise, below the expected 0.2% and previous 0.22%.

Core CPI figures also fell short of predictions. The Core CPI (NSA, YoY) rose by 2.79%, under the forecasted 2.9% and marginally above the prior 2.78%. Meanwhile, the Core CPI (SA, MoM) increased by 0.13%, missing the expected 0.3% and previous 0.24%.

-

- Figure 2: US CPI Picking Up on Tariffs Spillover

-

- Figure 3: US Core PPI (YoY)

Overview of the Australian Equities Market

Australia’s share market has lost much of the week’s gains, after Israel’s attack on Iran proved a brutal reality check for risk sentiment.

The S&P/ASX200 fell 17.7 points, or 0.21 per cent, to 8,547.4, as the broader All Ordinaries gave up 25.4 points, or 0.29 per cent, to 8,770.6. Wednesday’s dual-record intraday peak and best-ever close for the top 200 became a distant memory as Israeli air strikes on Iranian military targets and nuclear facilities prompted retaliatory drone attacks. Eight of 11 local sectors lost ground on Friday, while energy and utilities stocks surged after oil prices spiked to four-month highs in the wake of the attacks. The elevation of global risk came at an inopportune time for the ASX and its financial sector, both of which hit new highs this week and showed signs of being overbought in the short term.

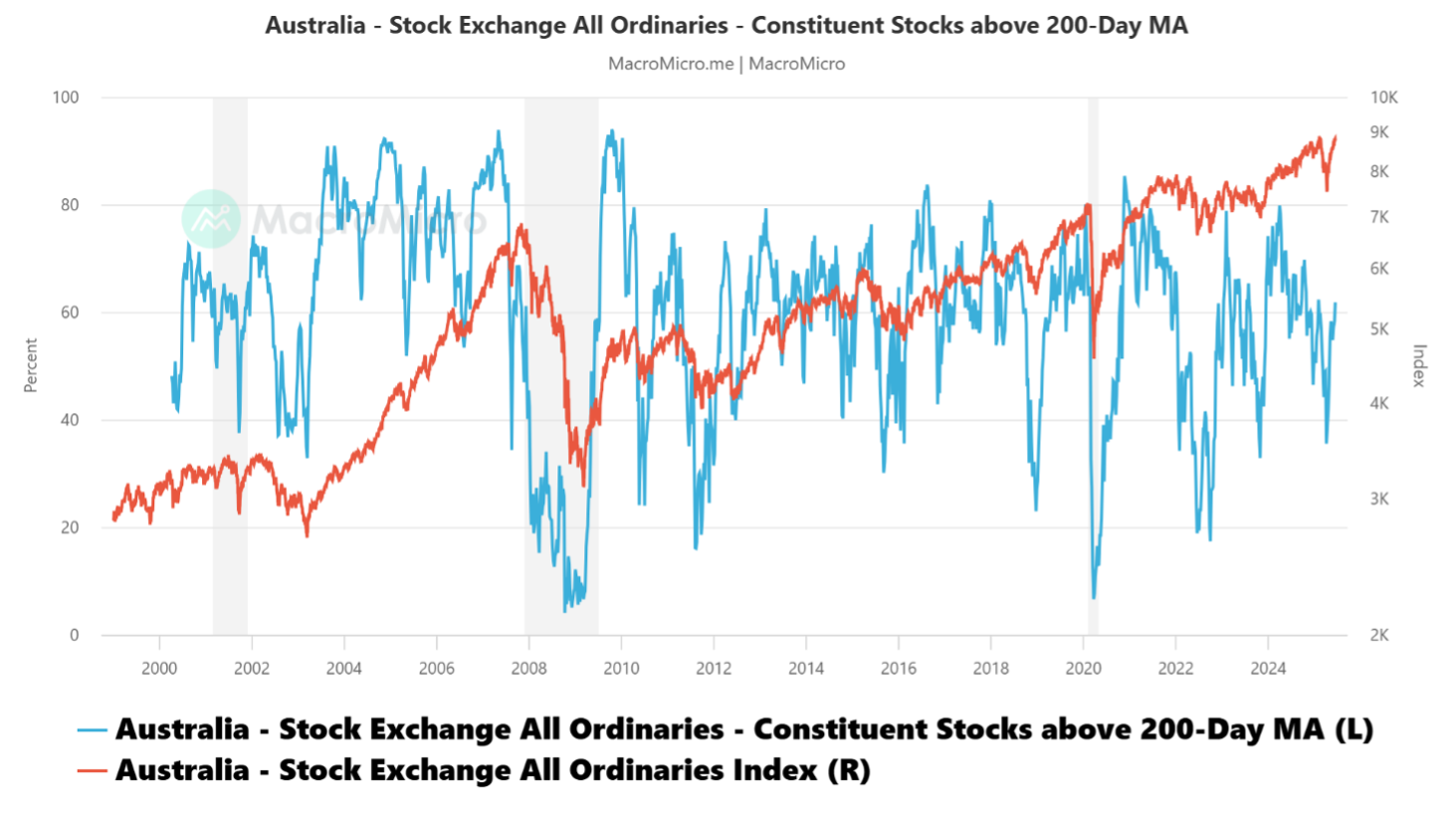

Figure 4 below shows the ASX All Ords index and market breadth (stocks above 200 day moving average of share price). After falling to below 40% during the Liberation Day sell-off, the market breadth in the broad index has now moved to above 60%, indicating improving participation in the rally be index stocks.

Figure 4: Australian Stocks – Improving Market Breadth

Energy stocks and utilities both surged more than four per cent, and the defensive consumer discretionary sector was the only other division in the green, up 0.25 per cent. The spike in crude prices was good news for Woodside investors, as the oil and gas giant rallied more than seven per cent to $25.21, the top 200’s best performer.

Financial stocks, which account for roughly half of the top-200’s value, fell 0.4 per cent as three of the big four banks, excepting a flat Westpac, ground lower.The sector was roughly flat for the week.Materials stocks fell 0.2 per cent, as rallying gold miners helped soften a sell-off in large-cap miners BHP (-2.6 per cent) and Rio Tinto (-1.1 per cent), tracking with an uplift in gold and continued weakness in iron ore prices.

Australia’s tech sector took the biggest hit on Friday, down 1.2 per cent as investors fled to safety.

Overview of the Australian Government Bond Market

Over the course of the week the Australian government’s bonds rallied across the curve. The Australian 1-year government bonds rallied 5bps to end the week 3.41%, the 2-year bonds rallied 8bps to end the week at 3.26% while the key 10-year bonds rallied 11bps to end the week at 4.16%. Australian government bond yield fell to the lowest point since March 2025 in the wake of Israel’s strike on Iran’s nuclear facilities. The 10-year US Treasury yield fell to 4.314% before recovering to last trade at 4.325%, still down 3 basis points on the day.

-

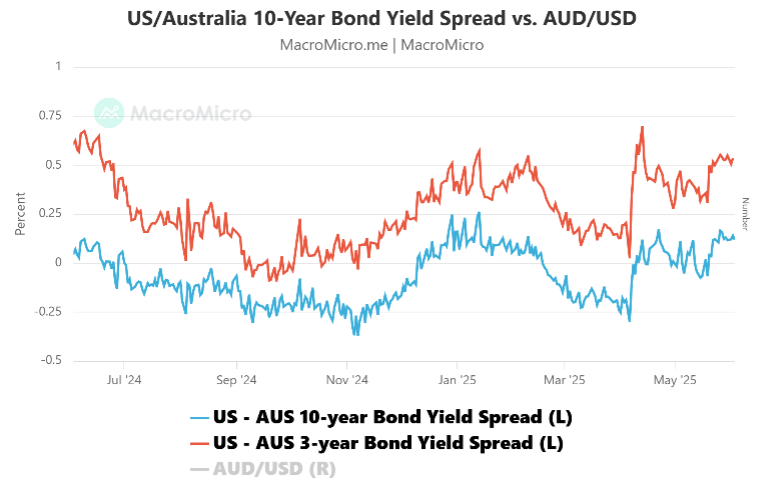

- Figure 5: US/Australia 10-year Bond Yield Spread

-

- Figure 6: Australia 10-year Bond Spread vs US

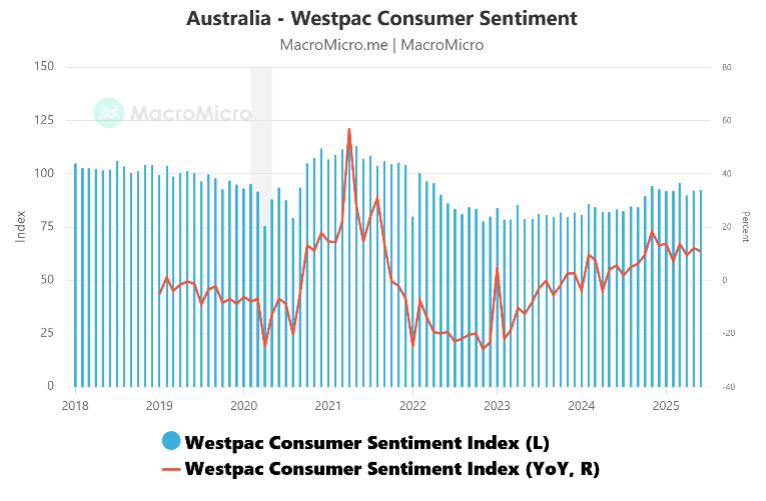

Domestically, the two key sentiment surveys were released. The Westpac-Melbourne Institute Consumer Sentiment Index rose 0.5% month-on-month to 92.6 in June—its fourth gain this year—supported by the May rate cut and signs of easing inflation.

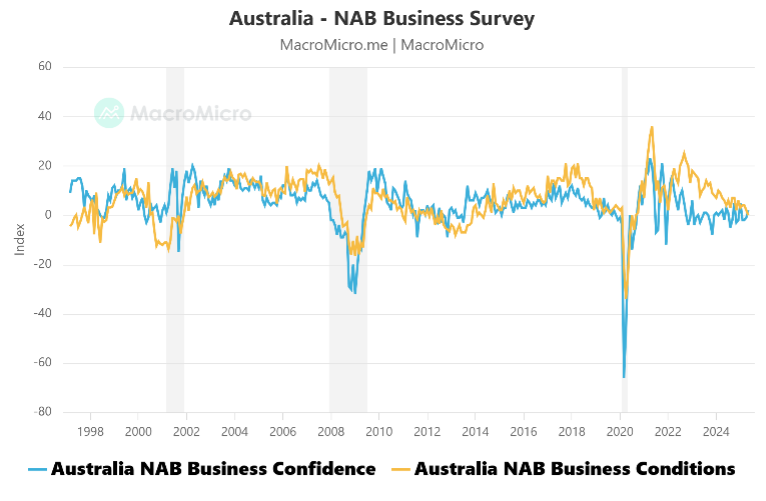

The NAB Monthly Business Survey for May showed that business conditions eased again in May to 0 index points. Conditions have fallen steadily over late 2024 and early 2025; in trend terms the series has eased from around average at +6 index points in September 2024 (to +2 index points currently). The decline in business conditions in recent quarters has narrowed the gap between business confidence and business conditions; it will be hard for confidence to lift sustainably if conditions deteriorate further. Business confidence improved again in May, though trend confidence remains below the long run average.

-

- Figure 7: WBC Consumer Sentiment – June

-

- Figure 8: Figure 2: NAB Monthly Business Survey

Chart of the Week- Crude Oil Futures

Israel launched Operation “Strength of a Lion”, targeting Iran’s nuclear facilities, ballistic missile sites, and military assets in a preemptive strike amid escalating tensions over Iran’s nuclear ambitions. Israeli Prime Minister Netanyahu stated that the attack aimed to permanently neutralize Iran’s nuclear threat. Iran responded by declaring a state of emergency, with explosions reported in Tehran. Reuters warns that the situation could spill over into neighboring oil-producing nations. Market reactions were swift—oil prices surged over 10%, gold surpassed $3,450, and safe-haven currencies like the Swiss franc and Japanese yen rallied, while US equity futures declined.

Figure : Crude Oil Futures

Market Summary Table

| Name | Week Close | Week Change | Week High | Week Low |

|---|---|---|---|---|

| Cash Rate% | 4.1 | |||

| 3m BBSW % | 3.725 | -0.005 | 3.735 | 3.7048 |

| Aust 3y Bond %* | 3.293 | -0.196 | 3.409 | 3.337 |

| Aust 10y Bond %* | 4.157 | -0.296 | 4.283 | 4.24 |

| Aust 30y Bond %* | 4.865 | -0.294 | 4.96 | 4.941 |

| US 2y Bond % | 3.935 | -0.0096 | 4.012 | 3.906 |

| US 10y Bond % | 4.379 | -0.126 | 4.484 | 4.357 |

| US 30y Bond % | 4.8603 | -0.153 | 4.954 | 4.843 |

| iTraxx | 67 | 0 | 71 | 67 |

| $1AUD/US¢ | 64.76 | -0.11 | 65.27 | 64.87 |

To read more about Yield Report Weekly Full Content Click here