JCB find the YieldReport to be an invaluable summary of all debt market activity. Whilst we are focussed on the highest grade bonds it is important to see what is..Angus Coote, Executive Director, JCB Active Bond Fund

Australian Corporate Fundamentals Well Insulated at First Glance

Global recession fears spooked financial markets last week with many questions left unanswered regarding the impact to company balance sheets. Positively, however, Australia was left relatively unscathed from a credit fundamental perspective with the Trump administration opting to impose the minimum 10% tariff on AU imports. For context, the US accounts for ~4% of Australia’s total exports, suggesting the first order impacts should be relatively manageable.

While the medium-term outlook remains clouded, particularly should larger trading partners (such as China and Japan) slow in terms of economic growth, international revenue (ex. New Zealand) from Australian issuers in the AusBond non-financial corporate universe appears moderate at approximately ~16% on our estimates. That said, international issuers make up around 22% of the non-financial corporate AusBond Credit index which has put greater upward pressure on the credit spread of the index.

Spreads have tightened across the market since the peak reflecting the change/delay in the tariff policy implemented by the Trump administration, however, still remain broadly wider than year-to-date peaks.

The potential flow on impact of a domestic recession arising from the potential deterioration in economic conditions from key trading partners cannot be discounted, but we expect credit ratings to remain robust all else equal should Australian corporate credit remain in its bubble.

Source- Bond Advisor

Meanwhile, in the US corporate bond market, lowly rated high yield companies have failed to sell any debt in the US high-yield bond market since Trump unleashed market turmoil and raised fears of a US recession with the wave of tariffs he announced earlier this month. Wall Street banks face potential losses on billions of dollars of short-term loans they had committed to in the expectation that junk-bond investors would ultimately take on the debt. But banks can be wrong-footed if the interest rate they have agreed to provide differs sharply from market levels, as can be the case in times of stress. The market sell-off comes as the private equity industry – and the banks that have long profited from their deals – struggles with a drop-off in dealmaking and fading hopes of a revival amid a looming threat of a recession.

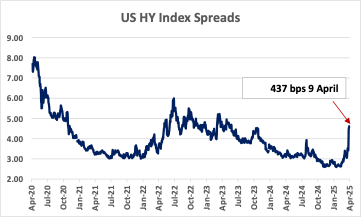

High yield credit spreads have eased slightly, now at 410 bps. Last week they shot to the highest level in nearly two years last week, hitting 4.61bps before retreating slightly after Trump agreed to pause some tariffs. Goldman Sachs last week raised its forecast for defaults by high-yield and leveraged loan borrowers this year to 5% and 8% respectively, up from 3% and 3.5%.

Bill Eigen, a bond portfolio manager at J.P. Morgan Asset Management who’s been hoarding cash for the past three years, has finally started deploying at least some of those funds as the credit market shows signs of cracks.

Over the past few weeks, Eigen, who manages the $10 billion JPMorgan Strategic Income Opportunities Fund, has bought assets including high-yield debt, convertible bonds, as well as exchange-traded and closed-end funds for corporate debt. While he declined to specify what he purchased or how much he’s buying, Eigen said he’s seeing opportunities that haven’t existed in years.

In high-yield debt, for example, Eigen said last week that he was seeing yields pushing toward 9% or higher, and spreads around five percentage points above Treasuries. That yield level is more than a percentage point above the average over the past year. Eigen said he had avoided more risky parts of the credit market over the past few years, because the bonds were priced to perfection. Now, as the Trump administration seeks to revamp the US’s trade relationships and fuels more questions around Corporate America’s outlook, the credit market is likely to see more pain, he said. When that happens, he plans to buy more, he said.