Summary: Corporate bond spreads 3bps tighter; swap spreads narrower; iTraxx up.

Corporate spreads finished the week 3bps tighter on average as corporate bond yields slightly outpaced the rises of their Commonwealth Government counterparts. The majority of spreads’ week-on-week changes at the individual level were within a range of -6bps to zero and the exceptions were limited to a couple of short-dated lines.

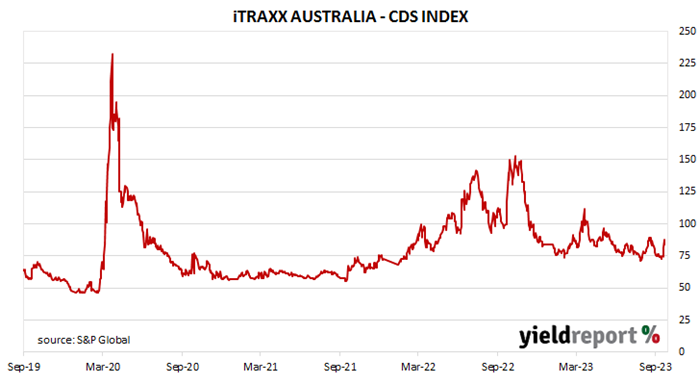

One of the two other main measures of corporate risk, swap-to-bond spreads, narrowed noticeably. The other main measure, credit default swap premiums, increased on average. The Australian credit default swap index, the iTraxx Australia Series 39, finished 10.00 points higher at 84.00 points.

AUSTRALIAN CORPORATE BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Apr-24 | 2.75 | 35,900 | 4.13 | 0.08 | 0.07 | 4.15 | 4.08 |

| 21-Nov-24 | 0.25 | 41,300 | 4.18 | 0.16 | 0.14 | 4.19 | 4.07 |

| 21-Apr-25 | 3.25 | 41,500 | 4.12 | 0.19 | 0.14 | 4.14 | 3.98 |

| 21-Nov-25 | 0.25 | 39,200 | 4.05 | 0.20 | 0.13 | 4.06 | 3.91 |

| 21-Apr-26 | 4.25 | 39,600 | 4.03 | 0.20 | 0.13 | 4.04 | 3.89 |

| 21-Sep-26 | 0.50 | 37,800 | 4.03 | 0.20 | 0.14 | 4.04 | 3.89 |

| 21-Apr-27 | 4.75 | 36,700 | 4.03 | 0.20 | 0.14 | 4.04 | 3.89 |

| 21-Nov-27 | 2.75 | 31,400 | 4.04 | 0.20 | 0.13 | 4.05 | 3.89 |

| 21-May-28 | 2.25 | 30,900 | 4.05 | 0.21 | 0.12 | 4.05 | 3.90 |

| 21-Nov-28 | 2.75 | 34,800 | 4.07 | 0.21 | 0.11 | 4.07 | 3.92 |

| 21-Apr-29 | 3.25 | 36,600 | 4.10 | 0.21 | 0.10 | 4.10 | 3.94 |

| 21-Nov-29 | 2.75 | 34,700 | 4.13 | 0.21 | 0.10 | 4.13 | 3.98 |

| 21-May-30 | 2.50 | 37,100 | 4.18 | 0.22 | 0.10 | 4.18 | 4.02 |

| 21-Dec-30 | 1.00 | 38,700 | 4.22 | 0.23 | 0.10 | 4.22 | 4.06 |

| 21-Jun-31 | 1.50 | 38,100 | 4.25 | 0.23 | 0.10 | 4.25 | 4.09 |

| 21-Nov-31 | 1.00 | 21,000 | 4.28 | 0.23 | 0.10 | 4.28 | 4.11 |

| 21-May-32 | 1.25 | 39,300 | 4.30 | 0.23 | 0.10 | 4.30 | 4.13 |

| 21-Nov-32 | 1.75 | 29,000 | 4.32 | 0.23 | 0.10 | 4.32 | 4.15 |

| 21-Apr-33 | 4.50 | 25,100 | 4.32 | 0.23 | 0.10 | 4.32 | 4.15 |

| 21-Nov-33 | 3.00 | 22,500 | 4.34 | 0.24 | 0.11 | 4.34 | 4.17 |

| 21-May-34 | 3.75 | 18,800 | 4.35 | 0.23 | 0.10 | 4.35 | 4.18 |

| 21-Dec-34 | 3.50 | 17,000 | 4.37 | 0.23 | 0.10 | 4.37 | 4.20 |

| 21-Jun-35 | 2.75 | 13,050 | 4.40 | 0.24 | 0.10 | 4.40 | 4.23 |

| 21-Apr-37 | 3.75 | 12,300 | 4.48 | 0.23 | 0.09 | 4.48 | 4.31 |

| 21-Jun-39 | 3.25 | 10,300 | 4.56 | 0.21 | 0.09 | 4.56 | 4.40 |

| 21-May-41 | 2.75 | 14,300 | 4.63 | 0.21 | 0.08 | 4.63 | 4.47 |

| 21-Mar-47 | 3.00 | 14,200 | 4.70 | 0.20 | 0.11 | 4.70 | 4.54 |

| 21-Jun-51 | 1.75 | 19,600 | 4.71 | 0.21 | 0.11 | 4.71 | 4.56 |