Summary:

Global and Domestic Bond Market Trends

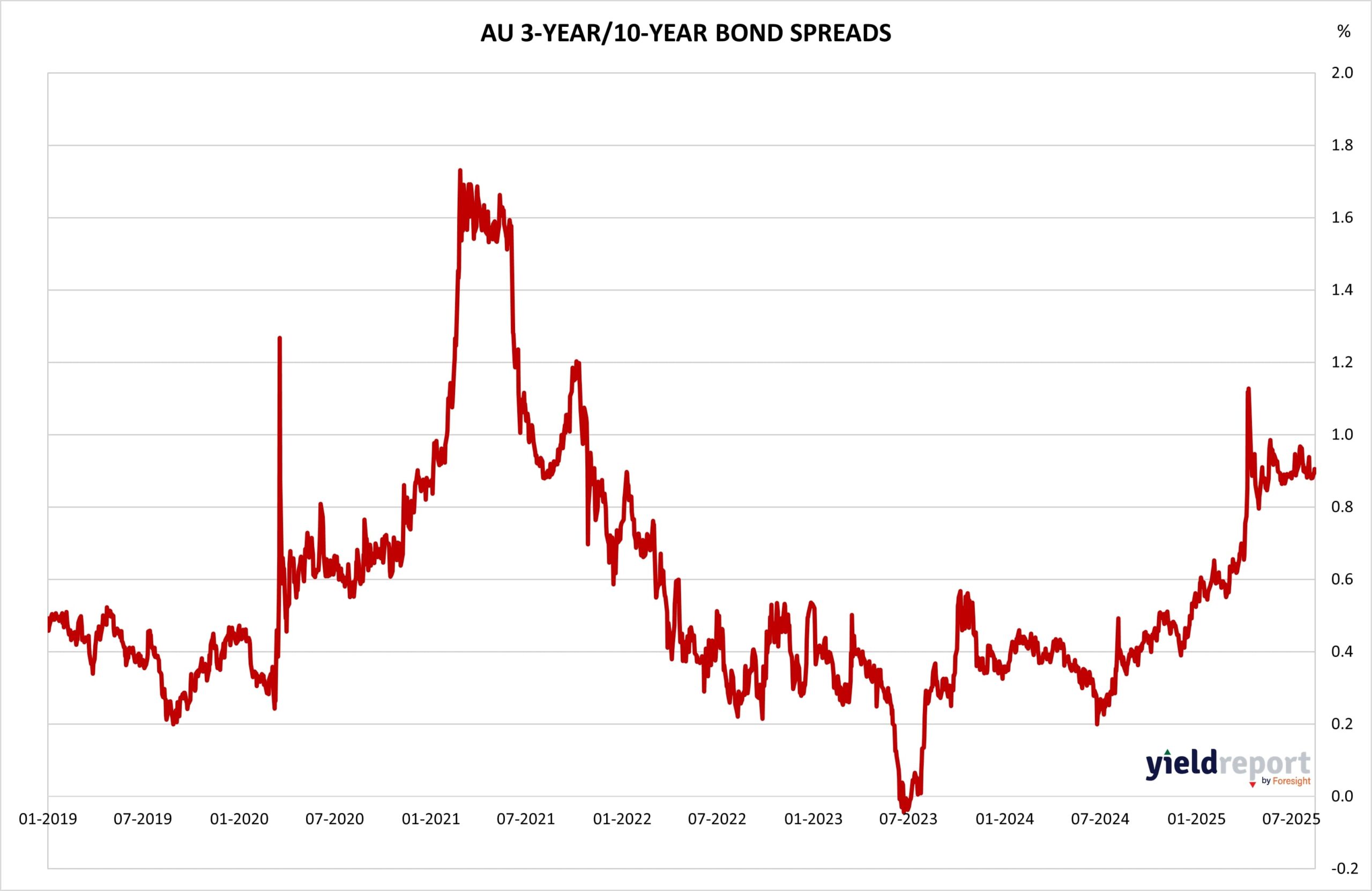

Australian Yield Curve

The AU 3s10s spread has rebounded sharply since mid-2023, reaching ~1.0% by July 2025. Key takeaways:

- Steepening trend suggests growing confidence in medium-term growth

- RBA’s cautious stance has kept short-end yields relatively anchored

- Long-end movement reflects global rate normalisation and domestic fiscal stability

Figure 1: Australia 3 and 10-year Bond Yield Spread

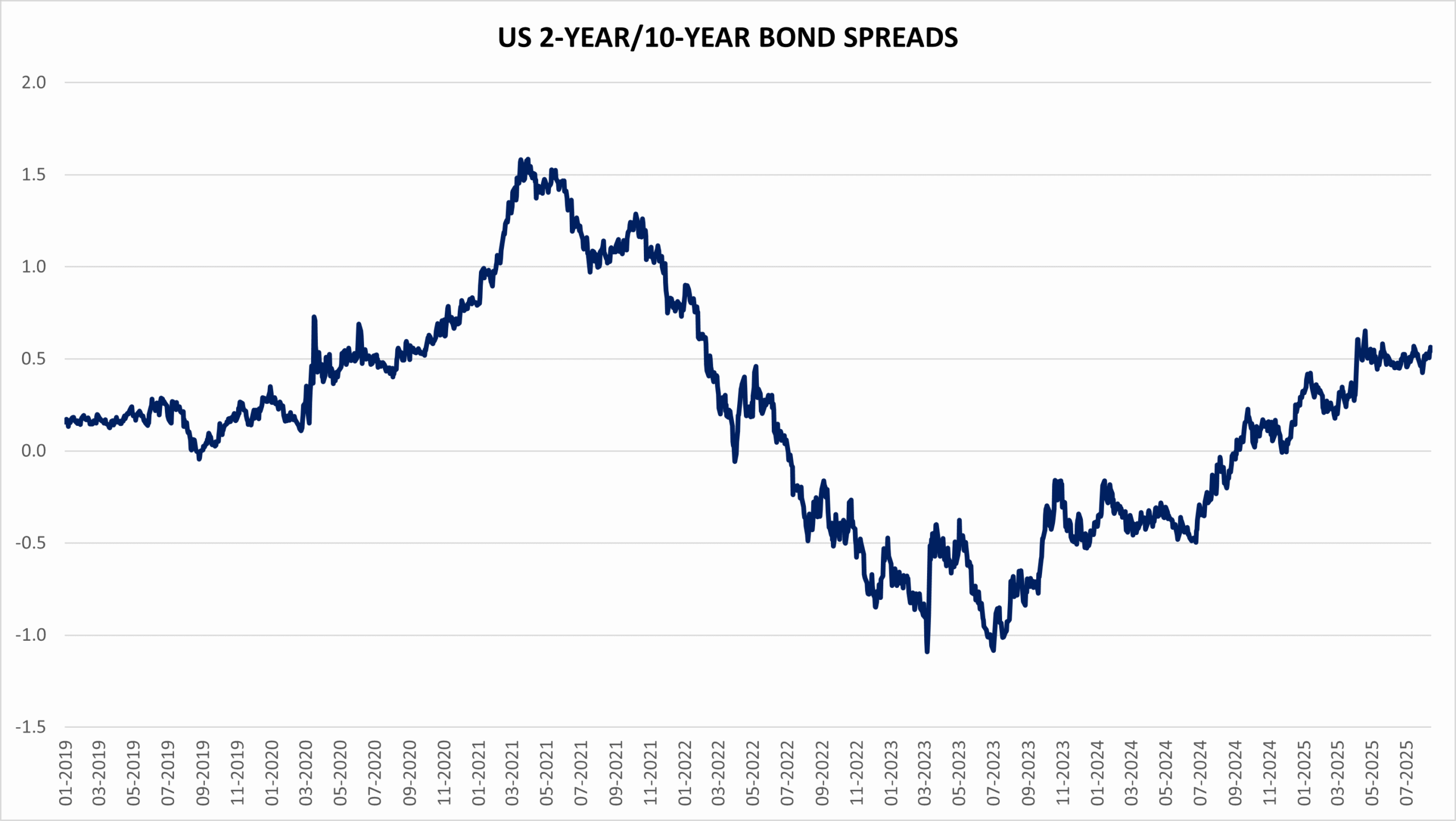

US Yield Curve

The US 2s10s spread narrowed to –0.35%, continuing its gradual climb from deeper inversion levels seen in 2022–2023. This shift reflects:

- Easing recession fears, supported by softer inflation data

- Dovish Fed tone, hinting at a potential policy plateau

- Investor repositioning, with increased demand for longer-dated securities

Figure 2: US 2 and 10-year Bond Spread

To learn more about yield curves and their predictive power, visit this article or this one.