Summary: 10-year bond yields down in Australia; ACGB 10-year spread to US Treasury yield falls from -3bps to -15bps; 10-year bond yields down in US, most major European markets; $3.7 billion of bonds, notes issued by AOFM.

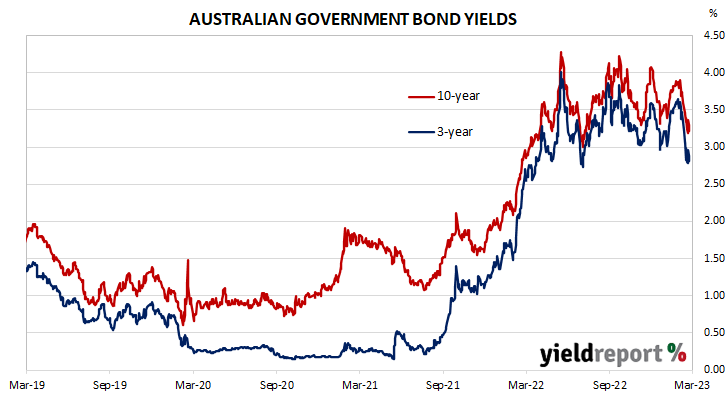

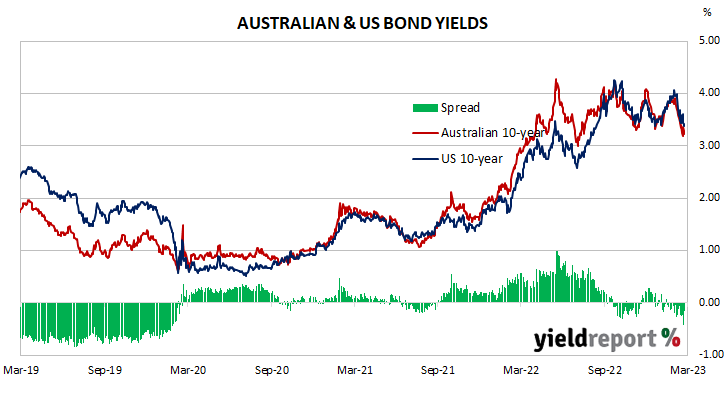

Locally, long-term ACGB yields started the week with a large fall and, with the exception of a mid-week bounce, this set the tone for much of the week. By the end of it, 3-year and 10-year ACGB yields had both lost 18bps to 2.81% and 3.32% respectively while the 20-year yield finished 16bps lower at 3.69%. The spread between US and Australian 10-year Treasury bond yields “tightened” from -3bps to -15bps.

Over in the US, 10-year bond yields started with a couple of days of solid or substantial rises. The increase was almost totally reversed midweek and yields continued to fall over the remainder of the week.

The FOMC’s two-day meeting ended on Wednesday and another 25bps increase to its target range for the federal funds rate was announced.

S&P Global Market Intelligence’s latest flash reading of its composite index was released at the end of the week, with the index rising from February’s final reading of 50.1 to 53.3. The manufacturing index increased from 47.4 to 51.0 and the services index added 3.2 points to 53.8. S&P Global’s Chris Williamson said, “March has so far witnessed an encouraging resurgence of economic growth…”

The Atlanta Fed’s Nowcast model was also updated. The March quarter GDP growth estimate remained at 3.2% annualised, or a 0.8% expansion over the quarter.

By this point, the US 2-year Treasury bond yield had lost 4bps to 3.78%, the 10-year yield had shed 6bps to 3.37% while the 30-year yield finished 2bps higher at 3.65%.

In major euro-zone markets, 10-year bond yields followed a similar path to their US counterpart except yields rose moderately midweek.

On Tuesday night (AEDT), Germany’s ZEW March survey indicated its Economic Sentiment index had dropped back from February’s reading of 28.1 to 13.0. ZEW’s current conditions index declined modestly, from -45.1 to -46.5. “The assessment of the earnings development of banks has deteriorated considerably, although it still remains slightly positive,” said ZEW President Achim Wambach. He also noted the insurance industry was significantly affected.

The results of March’s consumer sentiment survey were released on Thursday night (AEDT) and they indicated euro-zone sentiment had slipped a touch after improving for the previous five consecutive months.

The Bank of England raised its Bank Rate by 25bps to 4.25% on the same day.

S&P Global Market Intelligence released its March flash PMI figures for the euro-zone some hours before the US figures on Friday. The preliminary reading of the composite index was 54.1, up from February’s final reading of 52.0.

S&P Global’s Chris Williamson said, “The eurozone economy is showing fresh signs of life as we enter spring, with business activity growing at its fastest rate for ten months in March.”

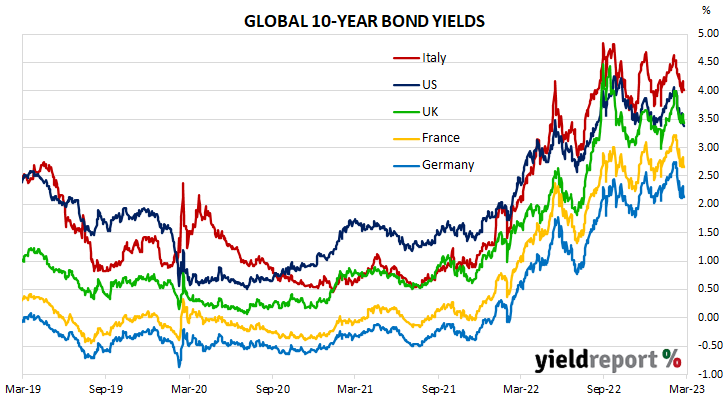

By this point, the German 10-year bond yield had added 1bp to 2.12% while the French 10-year OAT yield had lost 4bps to 2.65%. The Italian 10-year BTP yield decreased by 4bps over the week to 4.01% while the British 10-year gilt yield finished 1bp higher at 3.44%.

The AOFM held two bond tenders during the week. $700 million of November 2033s and $500 million of April 2026s were priced at respective yields of 3.35% and 2.86%. There were also three Treasury note tenders which raised a total of $2.5 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2022/2023 financial year-to-date (not taking into account buy-backs or short-term Treasury note tenders) is $57.65 billion. There are currently $835.55 billion of Treasury bonds and $38.586 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 April 2023 when $34.20 billion worth of bonds are due. There are also $28.5 billion of short-term Treasury notes currently outstanding after $5.5 billion matured on Friday.

AUSTRALIAN GOVERNMENT BONDS

| MATURITY | COUPON (%) | ISSUE SIZE ($M) | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|

| 21-Apr-23 | 5.50 | 34,200 | 3.40 | -0.07 | -0.12 | 3.47 | 3.40 |

| 21-Apr-24 | 2.75 | 35,900 | 3.09 | -0.16 | -0.64 | 3.24 | 3.04 |

| 21-Nov-24 | 0.25 | 41,300 | 2.96 | -0.16 | -0.65 | 3.12 | 2.92 |

| 21-Apr-25 | 3.25 | 41,500 | 2.86 | -0.17 | -0.70 | 3.03 | 2.83 |

| 21-Nov-25 | 0.25 | 38,700 | 2.82 | -0.17 | -0.73 | 2.99 | 2.79 |

| 21-Apr-26 | 4.25 | 39,100 | 2.85 | -0.17 | -0.72 | 3.02 | 2.82 |

| 21-Sep-26 | 0.50 | 37,800 | 2.87 | -0.18 | -0.73 | 3.04 | 2.83 |

| 21-Apr-27 | 4.75 | 36,700 | 2.90 | -0.17 | -0.71 | 3.07 | 2.87 |

| 21-Nov-27 | 2.75 | 31,400 | 2.93 | -0.17 | -0.69 | 3.10 | 2.90 |

| 21-May-28 | 2.25 | 30,200 | 2.96 | -0.17 | -0.68 | 3.13 | 2.93 |

| 21-Nov-28 | 2.75 | 34,100 | 3.00 | -0.16 | -0.66 | 3.16 | 2.96 |

| 21-Apr-29 | 3.25 | 35,000 | 3.02 | -0.18 | -0.66 | 3.20 | 2.99 |

| 21-Nov-29 | 2.75 | 34,700 | 3.06 | -0.18 | -0.66 | 3.24 | 3.03 |

| 21-May-30 | 2.50 | 37,100 | 3.10 | -0.18 | -0.64 | 3.28 | 3.07 |

| 21-Dec-30 | 1.00 | 38,700 | 3.14 | -0.18 | -0.63 | 3.32 | 3.11 |

| 21-Jun-31 | 1.50 | 38,100 | 3.17 | -0.17 | -0.62 | 3.34 | 3.14 |

| 21-Nov-31 | 1.00 | 21,000 | 3.19 | -0.18 | -0.62 | 3.37 | 3.16 |

| 21-May-32 | 1.25 | 39,300 | 3.20 | -0.18 | -0.61 | 3.38 | 3.17 |

| 21-Nov-32 | 1.75 | 29,000 | 3.21 | -0.18 | -0.61 | 3.39 | 3.19 |

| 21-Apr-33 | 4.50 | 23,600 | 3.22 | -0.18 | -0.61 | 3.39 | 3.19 |

| 21-Nov-33 | 3.00 | 21,100 | 3.24 | -0.18 | -0.61 | 3.42 | 3.22 |

| 21-May-34 | 3.75 | 16,600 | 3.27 | -0.18 | -0.61 | 3.44 | 3.24 |

| 21-Jun-35 | 2.75 | 10,050 | 3.35 | -0.19 | -0.61 | 3.54 | 3.34 |

| 21-Apr-37 | 3.75 | 12,300 | 3.47 | -0.18 | -0.57 | 3.65 | 3.46 |

| 21-Jun-39 | 3.25 | 10,300 | 3.60 | -0.17 | -0.52 | 3.77 | 3.59 |

| 21-May-41 | 2.75 | 13,800 | 3.69 | -0.16 | -0.47 | 3.85 | 3.66 |

| 21-Mar-47 | 3.00 | 14,200 | 3.77 | -0.13 | -0.42 | 3.84 | 3.72 |

| 21-Jun-51 | 1.75 | 19,000 | 3.78 | -0.10 | -0.37 | 3.88 | 3.70 |