Summary: Corporate bond spreads 6bps wider on average; swap spreads narrower; iTraxx up 1 point.

Corporate spreads finished the week about 6bps wider on average as corporate bond yields generally lagged the falls of their Commonwealth counterparts. The majority of spreads’ week-on-week changes at the individual level were within a range of -3bps to +7bps; Fonterra November 2027s (spread: 146bps, -6bps) and Lendlease October 2027s (spread: 261bps, -6bps) were the most notable exceptions.

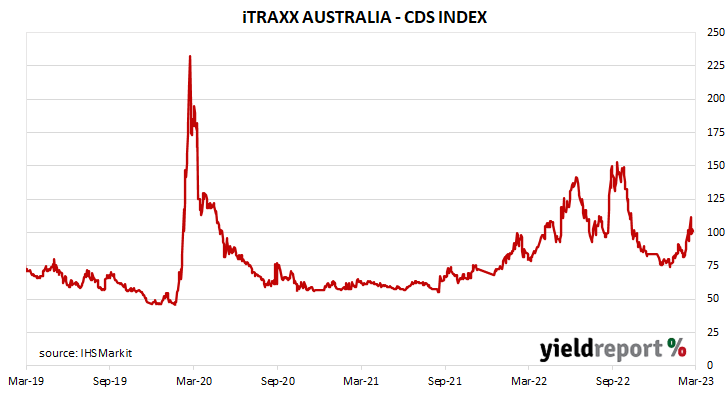

One of the two other main measures of corporate risk, swap-to-bond spreads, narrowed. Another measure of corporate risk, credit default swap premiums, increased a touch. The Australian credit default swap index, the iTraxx Australia Series 37, finished 1.00 point higher at 101.00 points.

AUSTRALIAN CORPORATE BONDS

| ISSUER | MATURITY | COUPON (%) | RATING | CLOSING YIELD | Δ WEEK | Δ MONTH | WEEK HIGH | WEEK LOW |

|---|---|---|---|---|---|---|---|---|

| ANZ | 16-Aug-23 | 5.00 | AA- | 4.05 | -0.03 | -0.07 | 4.08 | 3.99 |

| QANTAS | 10-Oct-23 | 4.40 | 4.64 | -0.03 | -0.14 | 4.68 | 4.54 | |

| AUSTPOST | 13-Nov-23 | 5.50 | A+ | 3.99 | -0.07 | -0.37 | 4.05 | 3.92 |

| WESTPAC | 21-Nov-23 | 5.25 | AA- | 4.00 | -0.05 | -0.28 | 4.06 | 3.92 |

| FONTERRA | 26-Feb-24 | 5.50 | A- | 4.01 | -0.09 | -0.57 | 4.10 | 3.92 |

| NAB | 11-Mar-24 | 5.00 | AA- | 4.05 | -0.15 | -0.45 | 4.19 | 4.02 |

| RABO NL AU | 11-Apr-24 | 5.50 | A+ | 4.18 | -0.08 | -0.47 | 4.25 | 4.10 |

| CBA | 27-May-24 | 4.75 | 4.01 | -0.12 | -0.57 | 4.12 | 3.95 | |

| AUSNET | 21-Jun-24 | 4.00 | BBB+ | 4.39 | -0.10 | -0.60 | 4.49 | 4.32 |

| MACQUARIE | 7-Aug-24 | 1.75 | A+ | 4.27 | -0.10 | -0.49 | 4.37 | 4.21 |

| WFC | 27-Aug-24 | 4.75 | 4.56 | -0.24 | -0.55 | 4.80 | 4.56 | |

| UNISYD | 28-Aug-25 | 3.75 | 3.92 | -0.20 | -0.61 | 4.12 | 3.91 | |

| APPLE | 10-Jun-26 | 3.60 | 3.89 | -0.14 | -0.55 | 4.04 | 3.88 | |

| CBA | 11-Jun-26 | 4.20 | 4.17 | -0.18 | -0.59 | 4.35 | 4.17 | |

| ANZ | 22-Jul-26 | 4.00 | 4.17 | -0.16 | -0.57 | 4.34 | 4.17 | |

| QANTAS | 12-Oct-26 | 4.75 | 5.01 | -0.20 | -0.43 | 5.21 | 5.00 | |

| AUSPAC AIRPORT | 4-Nov-26 | 3.75 | BBB+ | 4.48 | -0.18 | -0.58 | 4.66 | 4.47 |

| AUSTPOST | 1-Dec-26 | 4.00 | A+ | 4.09 | -0.20 | -0.59 | 4.29 | 4.08 |

| WSO FINANCE | 31-Mar-27 | 4.50 | 4.42 | -0.22 | -0.64 | 4.64 | 4.42 | |

| TELSTRA | 19-Apr-27 | 4.00 | A | 4.16 | -0.21 | -0.73 | 4.37 | 4.16 |

| ASCIANO | 12-May-27 | 5.40 | BBB- | 5.78 | -0.11 | -0.36 | 5.94 | 5.73 |

| FONTERRA | 2-Nov-27 | 4.00 | A- | 4.39 | -0.22 | -0.58 | 4.62 | 4.39 |

| MACQUARIE | 15-Dec-27 | 4.15 | BBB+ | 5.42 | -0.08 | -0.25 | 5.61 | 5.39 |

| AUSNET | 21-Aug-28 | 4.20 | A- | 5.03 | -0.17 | -0.41 | 5.21 | 5.03 |

| AUSNET | 31-Jul-29 | 2.60 | A- | 5.24 | -0.17 | -0.48 | 5.41 | 5.24 |