Summary: ACGB gradient flatter; US Treasury curve gradient also flatter.

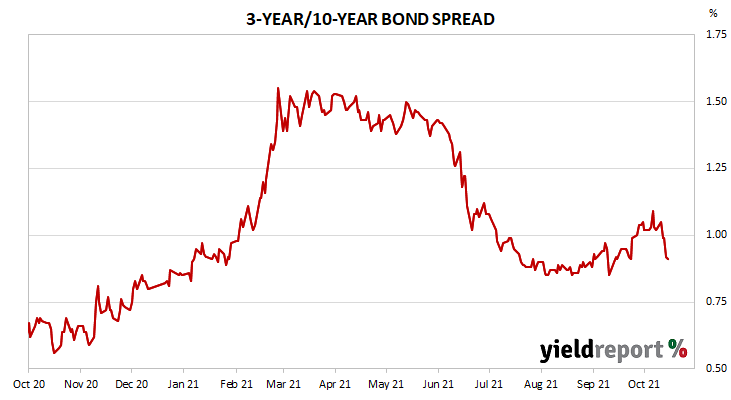

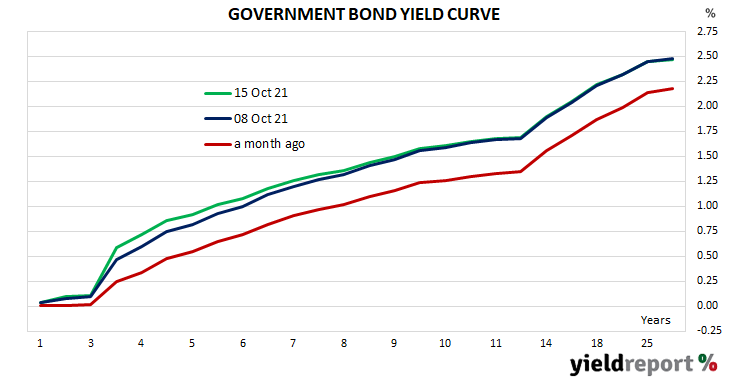

The gradient of the ACGB yield curve flattened as yields increased at the short end. By the end of the week, 3-year/10-year and 3-year/20-year spreads had both shed 11bps to 91bps and 152bps respectively.

.

The gradient of the US Treasury curve also became flatter. The 2-year/10-year spread tightened by 12bps to 118bps while the 2 year/30 year spread lost 21bps to 165bps. The San Francisco Fed’s favoured recession-predicting measure, the 3-month/10-year Treasury spread, finished 4bps narrower at 153bps.

To find out more about the yield curve and its usefulness, click here or here.

*December futures