Summary:

Term premiums remained elevated. In the US, investors also were motivated to buy longer-maturity Treasury debt at yield levels that offer the most compensation, relative to shorter-maturities, in more than a decade. This dynamic increased during the week, based on Fed officials suggesting a June cut. The term premium increased to 74 basis points, last seen in September 2014. Term premiums have been on the rise as US economic policy becomes harder to predict. A gauge of policy uncertainty neared a record this month after President Donald Trump announced sweeping tariffs and then backtracked on some. Proposals for tax cuts and a potential need to increase the US government debt limit also contributed to the move.

Meanwhile, higher Treasury yields are failing to support the value of the US dollar as they have historically. The relationship between the dollar and Treasury yields is the weakest in three years as investors question the dollar’s haven status. Options positioning shows show that traders expect more losses for the dollar. The moves last week were highly unusual and, in an interview, yesterday, Jenet Yellen stated that she believed the move in the USD last week was a sign of foreign asset selling. But there is a ton of narratives out in the markets about last week’s move.

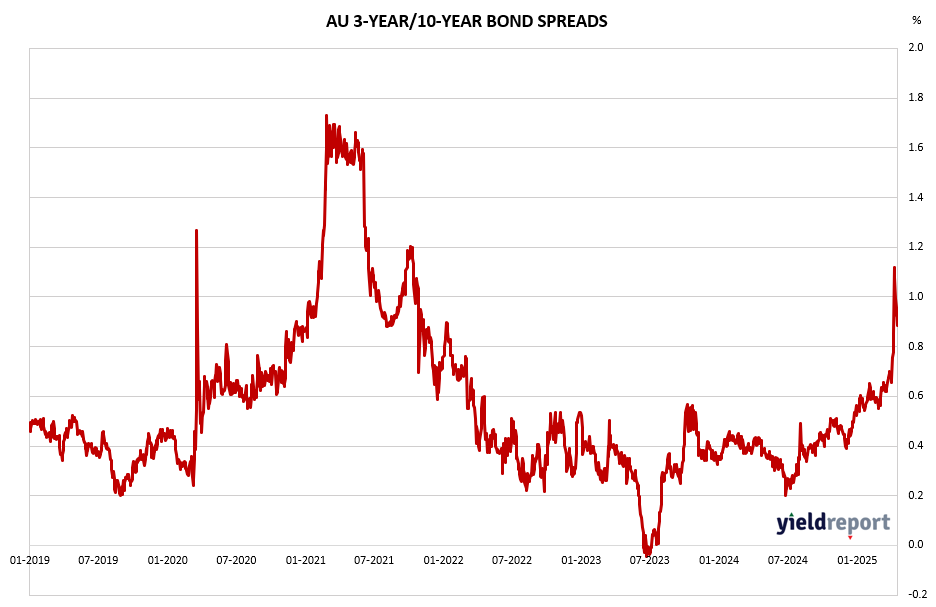

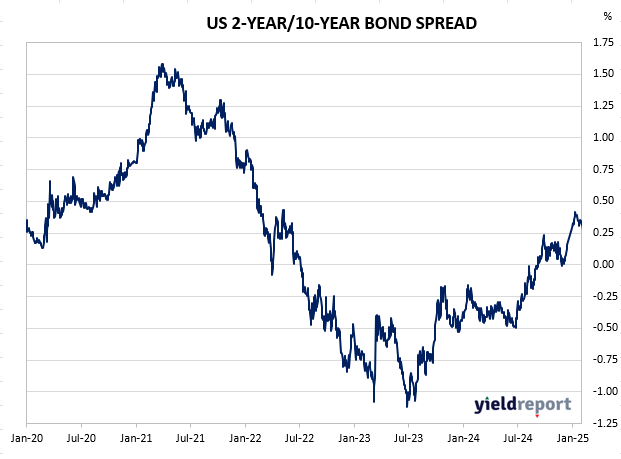

The Australian yield curve has been steepening aggressively for 2 weeks now, mirroring the US. What is happening in the back-end is more about US bond market dysfunction. The front end is making slightly more functional sense and reflective of where the RBA is expected to move on monetary policy. That is, cuts.

At the end of the week the Australian 2-year government bond had decreased by 7 bps to 3.19%. We’d say that is a relatively accurate reflection of the RBA’s thinking right now. They have noted that 1) they are in no rush, and 2) there is a madness of uncertainty currently – give us time to assess. In contrast, the money markets have been aggressive – they are at 5x 25 bps cuts now. Right now, that is not going to happen. But ‘Right Now’ has all the certainty of trying to look through mud.

|

Exhibit 1: Australian 10-yr minus 3-year Spread |

|

Exhibit 2 : US 10-yr minus US 2-yr Spread |

To find out more about the yield curve and its usefulness, click here or here.