Summary: Australian gradient steeper; US Treasury curve also steeper.

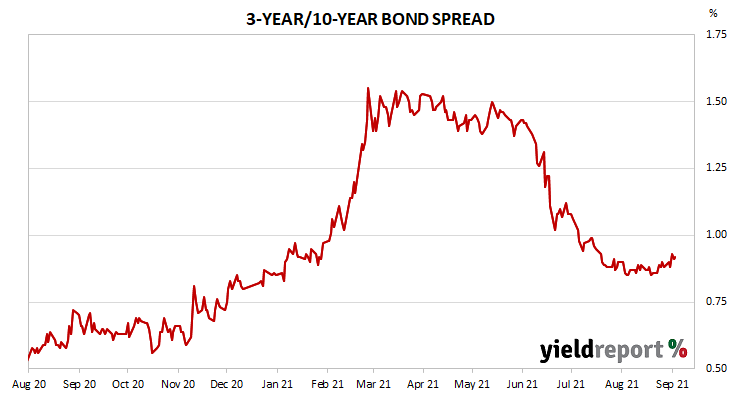

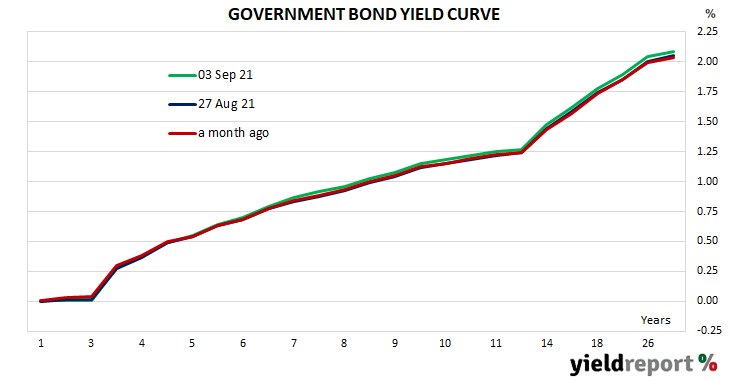

The gradient of the ACGB yield curve steepened a touch as yields rose at the long end. By the end of the week, the 3-year/10-year spread had widened by 4bps to 92bps and the 3-year/20-year spread had increased by 3bps to 154bps.

The gradient of the US Treasury curve also became steeper as yields at the long end increased. The 2-year/10-year spread gained 4bps to 112bps and the 2 year/30 year spread added 6bps to 174bps. The San Francisco Fed’s favoured recession-predicting measure, the 3-month/10-year Treasury spread, finished 2bps wider at 128bps.

To find out more about the yield curve and its usefulness, click here or here.