Summary: ACGB gradient noticeably flatter; US Treasury curve gradient also flatter.

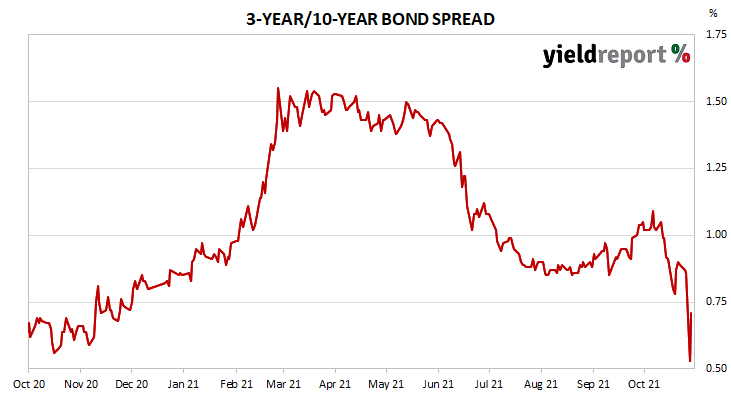

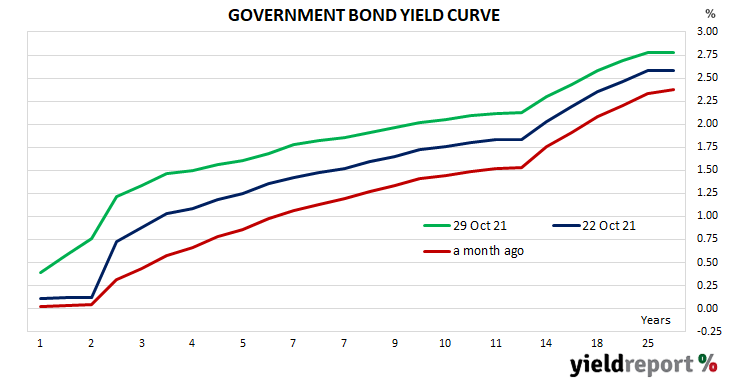

The gradient of the ACGB yield curve flattened a little The gradient of the ACGB yield curve flattened noticeably as yields at the front end increased markedly more than those at the long end. By the end of the week, the 3-year/10-year spread had tightened by 18bps to 71bps and the 3-year/20-year spread had shed 25bps to 123bps.

.

The gradient of the US Treasury curve also became flatter as yields rose at the short end while long-end yields declined. The 2-year/10-year spread tightened by 12bps to 106bps while the 2 year/30 year spread shed 18bps to 144bps. The San Francisco Fed’s favoured recession-predicting measure, the 3-month/10-year Treasury spread, finished 7bps tighter at 151bps.

To find out more about the yield curve and its usefulness, click here or here.

*December futures