Summary:

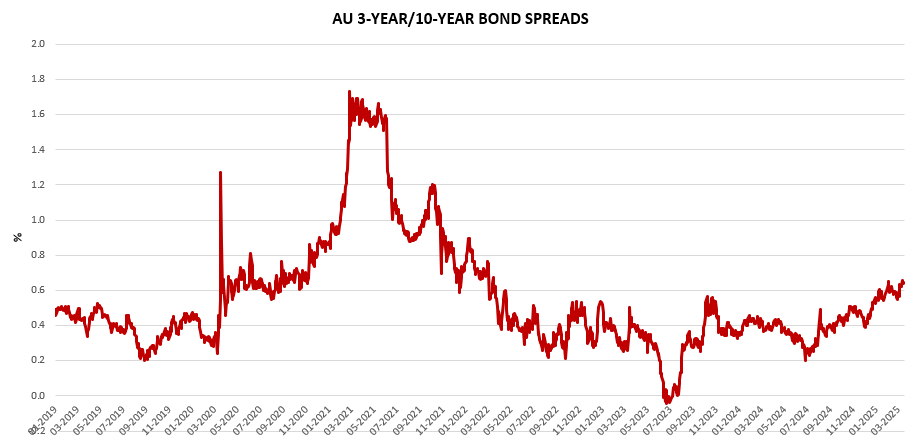

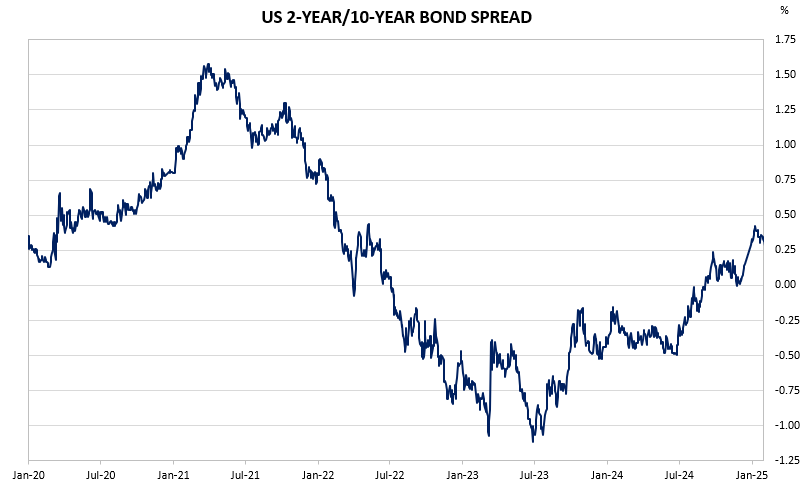

The Australian yield curve has been steepening aggressively for 2 weeks now, mirroring the US. What is happening in the back-end is more about US bond market dysfunction. The front end is making slightly more functional sense and reflective of where the RBA is expected to move on monetary policy. That is, cuts.

At the end of the week the Australian 2-year government bond had increased by 20 bps to 3.4%. We’d say that is a relatively accurate reflection of the RBA’s thinking right now. They have noted that 1) they are in no rush, and 2) there is a madness of uncertainty currently – give us time to assess. In contrast, the money markets have been aggressive – they are at 5x 25 bps cuts now. Right now, that is not going to happen. But ‘Right Now’ has all the certainty of trying to look through mud.

|

Exhibit 1: Australian 10-yr minus 3-year Spread |

|

Exhibit 2 : US 10-yr minus US 2-yr Spread |

To find out more about the yield curve and its usefulness, click here or here.