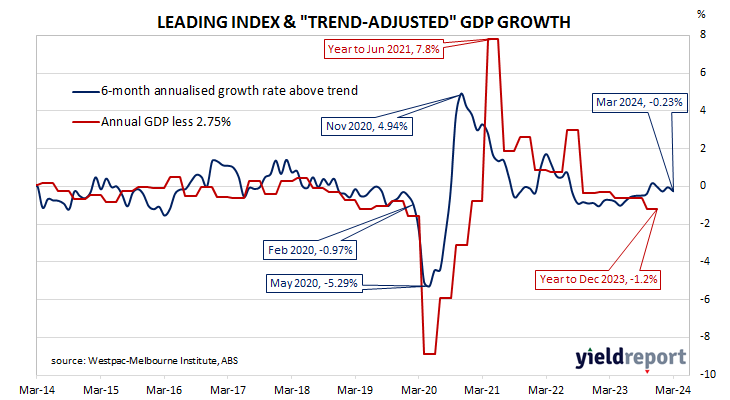

Summary: Leading index growth rate down in March; update points to Australia’s sub-trend growth continuing throughout 2024; reading implies annual GDP growth of around 2.5%; ACGB yields rise; rate-cut expectations soften; persistently soft results suggest growth will remain weak over remainder of year.

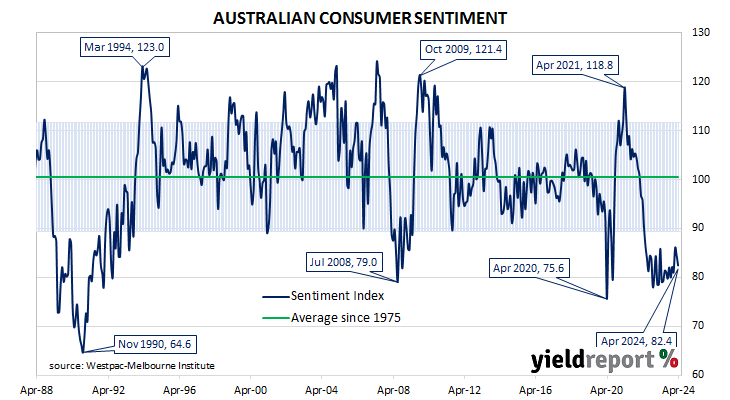

Westpac and the Melbourne Institute describe their Leading Index as a composite measure which attempts to estimate the likely pace of Australian economic growth in the short-term. After reaching a peak in early 2018, the index trended lower through 2018 and 2019 before plunging to recessionary levels in the second quarter of 2020. Subsequent readings spiked towards the end of 2020 but then trended lower through 2021 and 2022 before flattening out in 2023.

March’s reading has now been released and the six month annualised growth rate of the indicator registered -0.23%, down from February’s revised figure of -0.03%.

“The latest Leading Index update points to Australia’s sub-trend growth performance continuing throughout 2024,” said Westpac senior economist Matthew Hassan. “Despite some improvement over the last six months, and a brief one month lift into positive late last year, the Index growth rate has been stuck firmly below zero in early 2024.”

Index figures represent rates relative to “trend” GDP growth, which is generally thought to be around 2.75% per annum in Australia. The index is said to lead GDP by “three to nine months into the future” but the highest correlation between the index and actual GDP figures occurs with a three-month lead. The current reading is thus indicative of an annual GDP growth rate of around 2.5% in the next quarter.

Domestic Treasury bond yields rose nearly uniformly along the curve on the day, largely in line with movements of US Treasury yields on Tuesday night. By the close of business, 3-year and 10-year ACGB yields had both gained 6bps to 3.93% and 4.40% respectively while the 20-year yield finished 4bps higher at 4.68%.

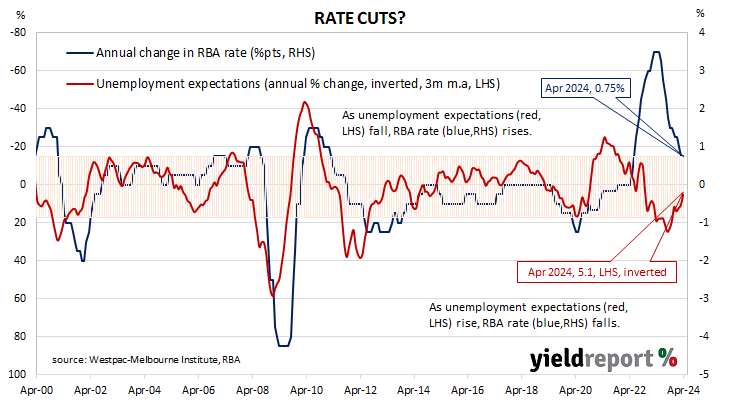

In the cash futures market, expectations regarding rate cuts in the next twelve months softened. At the end of the day, contracts implied the cash rate would remain close to the current rate for the next few months and average 4.305% through May and 4.29% in June. However, August contracts implied a 4.25% average cash rate, November contracts implied 4.195%, while May 2025 contracts implied 4.045%, 28bps less than the current rate.

“While not overly concerning…the persistently soft results suggest growth will remain weak over the remainder of the year,” Hassan added.