10 October 2016

Unemployment in the US remained steady at 5.0% in September as the number of people in the US in employment increased and the participation rate rose. 156,000 new jobs were created but the participation rate rose from 62.8% to 62.9% leaving the unemployment rate steady at 5.0%.

Although the numbers were slightly less than expected, the probability of a December rate rise implied by Federal funds futures rose from 55% to 60%, the 2 year bond yield fell back 2bps to 0.83% and the 10 year bond yield edged down 1bps 1.72%.

UBS economist Samuel Coffin pointed to what he saw as symptoms of reduced slack in the number of people available for new jobs. “Over the past twelve months, low-wage industry employment has risen 2.0% and high-wage industry employment 1.9%. That steady-ish job quality suggests that the strength in job openings is not because of skills shortage but is instead because of broader labor (sic) market tightness.” ANZ Research focussed on a rise in hourly rates of pay and said, “Average earnings rose to 2.6% y/y, indicating wage pressures are gradually moving higher… The trend growth in the labour market is slowing, but that’s because available slack is less and the expansion is mature…The market viewed the figures as strong enough to keep prospects of a December Fed rate hike on track.”

10 October 2016

The fixed interest desk at Bell Potter started the week with a recommendation for holders of Suncorp CPS 3 (ASX code: SUNPE) to switch to Bendigo & Adelaide Bank CPS 2 (ASX code: BENPE). Call dates for each are in 2020; Suncorp’s is in June while Bendigo’s is in November 2020. However, one has a yield at the top of those on offer and the other has a yield which is towards the bottom of the range. Suncorp is the larger institution and its senior debt is rated “A” by S&P Global while Bendigo’s senior debt rating is “A-“.

At the close of trading on 10 October, below is a chart which shows how they and other non-major bank hybrids looked. It is not hard to see why it caught Bell’s interest. *To call date. Assumes BBSW unchanged. Includes franking credits, capital gain/loss.

*To call date. Assumes BBSW unchanged. Includes franking credits, capital gain/loss.

10 October 2016

Australia’s Treasurer, Scott Morrison, has reportedly told the Australian Financial Review that he opposes further interest rate cuts on the basis that they have exhausted their effectiveness. He was speaking whilst in Washington to address central bank governors, finance ministers and investors.

The statement is unusual in that the Reserve Bank of Australia is set up to be independent of government. It makes its own decisions, free from political interference. The comments might be seen as trying to influence the RBA although the RBA has in the past noted that the effectiveness of cutting rates was diminishing as rates were cut.

The Treasurer also signalled that the government would need to do more with fiscal policy and reforms to boost productivity and to incomes.

07 October 2016

In mid-September YieldReport wrote of the AOFM’s plans to issue a Commonwealth security with a 30 year tenor. The AOFM has now announced it intends to issue a new March 2047 bond via syndication, subject to market conditions, in the week beginning 10 October 2016.

Issuing long term bonds has become the fashionable thing for sovereigns to do in recent times. Italy has just issued its inaugural 50 year bond and Ireland has joined Mexico to be among the few countries to have issued “centennials” (100 year bonds). In this context, 30 years looks downright conservative.

There’s no shortage of investors willing to buy long-duration bonds either. €18.5 billion (AUD$27 billion) of orders were placed for €5 billion (AUD$7.4 billion) of Italian 50 year bonds. Even Ireland, only a few years after being branded an economic basket case, managed to sell its 100 year bonds at a lower yield than a US 30 year Treasury bond earlier this year, so a AAA-rated country such as Australia should have little trouble attracting investors.

Related articles

New Aussie 30 year bond is nearly here

Australian 30 year bond back on radar

06 October 2016

There are some economists and commentators who talk of never-ending cycles of bond purchases by central banks. They struggle to see central bankers admitting defeat and abandoning their quantitative easing programmes. At the back of their minds, however, they and everyone else know that bond purchases by European, Japanese and US central banks must eventually come to an end. Someone is going to have to pick up the tab.

So when a report comes out suggesting the European Central Bank is preparing for just that, an end to bond purchases, albeit in a gradual, tapered manner, it naturally causes quite a bit of angst. All it took was report of officials discussing the manner in which the ECB asset purchase programme will end. As it is, it is scheduled to end in March 2017. However, the programme will operate beyond the scheduled finish date “if necessary, and in any case until the Governing Council sees a sustained adjustment in the path of inflation consistent with its inflation aim.”

The report in question is unsubstantiated and was denied by the ECB which stated the European Governing Council “has not discussed these topics…”. However, the denial did not stop yields on German 10 year bunds, UK gilts and US Treasurys all moving up by 3-4bps on the day. Australian 10 year bond yields took the lead from offshore and rose a similar amount. The next ECB policy meeting is scheduled for 20 October 2016.

06 October 2016

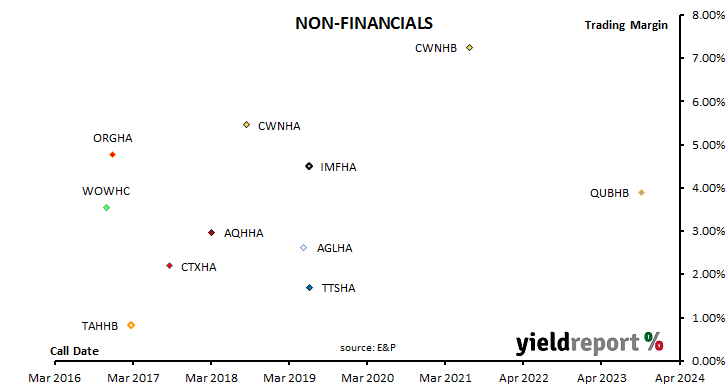

Qube Holdings Notes (ASX code: QUBHA) began trading on a deferred delivery basis on the ASX this week. The first trade was at $101.30. The notes finished the day at $101.57, a small premium to their $100 face value. They have a maturity date of 5 October 2023 and an issue margin of 3.90% above BBSW (an initial yield around 6.50%). Normal trading is expected to begin on 10 October.

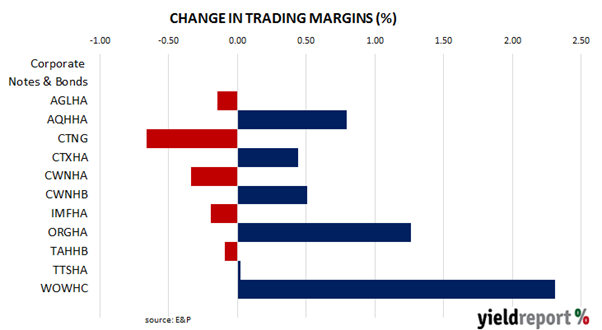

Since the issue was announced at the end of August, margins on ASX listed notes have risen with the median trading margin moving from 2.01% on the day of the announcement to 2.19% on the day before trading commenced. The diagram below shows how non-bank corporate notes have fared over that period and readers will see it has been a bit of a mixed bag.

Qube’s new issue initially sought to raise $200 million but demand was strong and the issue was upsized to $305 million. The first interest payment date is set for 5 January 2017 with the first payment amount an estimated $1.4203. The chart below shows how trading margins stood at the end of the first day’s trading.

06 October 2016

Italy has, arguably, Europe’s most at-risk banking system, yet this week the country has pulled off something of a coup. It has managed to issue 50 year government bonds. Never mind that in the past 50 years the country has changed prime ministers more than 30 times,

Italy is offering investors the privilege of receiving 2.80% per annum for the next 50 years.

The bond sale netted bids of over €18bn for a final bond issue size of €5bn. The yield is the same as 30 year bonds the country issued earlier in 2016. The successful issue has been largely put down to the fact that investors are desperate to buy bonds paying a ‘reasonable’ yield. Keep in mind reasonable is a very flexible term and many investors such as insurance companies and life offices are mandated to buy government bonds almost regardless of the yield.

Added to this is the fact that the European Central Bank has been buying so many bonds as part of its quantitative easing programme that investors are having difficulty of finding bonds to buy. With over $US10 trillion worth of bonds around the world trading at negative yields, the 2.80% on offer is seen as good value, by some.

Italy is also in a state of flux, again, and Prime Minister Matteo Renzi has called a referendum in December seeking a mandate for economic reform which may well backfire and see him resign if it fails. As bond prices around the world rise from their record lows in July and August it would seem a brave person or fund to load up on 50 year Italian debt.

04 October 2016

Total job advertisements fell in September (in seasonally–adjusted terms) after rising in August, according to ANZ’s monthly jobs ads survey. The month-on-month figure fell by 0.4%, and the year to September figure moved back to 3.6%, or where it was in June 2014.

Domestic bond markets largely ignored the results and took their trading leads from offshore news. The 3 year bond yield increased by 4bps to 1.53% while the 10 year bond yield moved up 3bps to 2.02% on the day. The AUD was down about half a US cent on the day, which is an indication the forex market thinks future interest rates are likely to be lower.

Labour force figures for September have not yet been released and so how the job ads to total employment ratio has fared in September is not known. The chart below shows the inverse relationship between the job ads to total employment ratio and the unemployment rate. As the ratio rises (more adds per potential employee) the unemployment rate falls. However, the rate of ads per potential employee is still far from pre-GFC levels.

04 October 2016

No one really expected the RBA to change the official cash rates at its October meeting and when the announcement of no change was made at 2.30pm, barely a ripple was registered in financial markets. Prior to the meeting, the probability of a cut to 1.25% implied by October cash contracts was 4% because economists and other observers all have their eyes on November’s meeting.

There are only four distinct months of the year where the RBA is thought to considering changing rates, barring emergencies. Each of these months follow the release of CPI figures, which are released on a quarterly basis as well as the quarterly Statement on Monetary Policy. June quarter CPI figures are released in July, September quarter CPI figures are released in October and so on. For a central bank which has essentially two priorities, one being employment and the other being price stability, consumer inflation figures are very important. So, it is no surprise the RBA would wait until the latest inflation data is out before moving one way or another. Therefore rate decisions, more often than not, are made in February, May, August and November.

Westpac’s Bill Evans noted the move to a neutral bias in the Governor’s statement and how the implied reference to the next CPI report present in July statement is not present in this one. “…the decision to de-link the next inflation report from next month’s policy decision must be partly influenced by developments in the housing market.” NAB’s David de Garis disagreed regarding the link to the next inflation report. “The next big local data point that could yet make the upcoming November meeting a “live” meeting is the September quarter CPI, being released on 26 October. NAB’s model forecast is for steady underlying inflation of 0.5% q/q that would see the RBA continue to hold rates steady through the New Year.” ANZ, as with Westpac, noted the reference to housing. “The Bank is clearly mindful of the resurgence in house price strength, noting yesterday that “some markets have strengthened recently”. The looming swell in supply is also on the Bank’s radar, and yesterday’s smaller-than-expected fall in building approvals (after a 12% m/m rise in July) would have been noted.

After the August cut from 1.75% to 1.50%, there were quite a few economists, strategist and others who expected another cut to 1.25% and beyond. On the day after the August decision, November cash contracts implied a 46% probability of another cut. Now, with only a month to go, the odds have been cut back to 1 in 5. 3 year and 10 year bond yields both rose 5bps to 1.57% and 2.08% respectively on the day.

03 October 2016

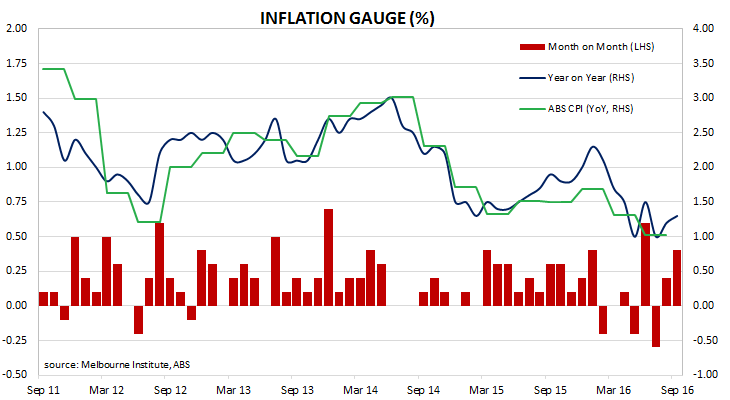

Central banks around the world are fretting. Not because inflation is out of control and affecting investment decisions and eroding people’s savings as it did during the 1970s and 1980s. Rather the central banks are fretting because they want more of it. Bizarre as this may sound, central bankers think a modest amount of inflation is a good thing. Indebted governments also like inflation as it erodes the value of government debt. This is the opposite for savers who see inflation diminishing their real (after inflation) returns. As one person’s liability is another person’s asset, inflation shifts value from one party to another.

One private measure of inflation, the Melbourne Institute Inflation Gauge, is recorded monthly and the latest reading for September indicates consumer prices rose by 0.4% for the month and 1.3% year on year. Readers will see from the chart below how the Inflation Gauge is an excellent proxy for official CPI figures produced by the Australian Bureau of Statistics. Consumer inflation over the last five years has been edging down quite consistently and this latest figure, while not low on a monthly basis, is far away from marking the end of this trend. Economists and the RBA will require a few more months of figures above 0.2% before they gain confidence inflation has risen back to the RBA’s 2% to 3% target band.