29 September 2016

Yields are inversely related to prices and, whether you are dealing with bonds or shares, this is the inescapable rule which is drummed into all young advisers and traders. It’s mathematically set in stone; if the denominator (the lower part) of the fraction goes up, the fraction as a whole goes down.

So when you are advised the yield of something has gone up at the same time as the price, the natural inclination is to believe something is amiss. Yet, this is what has just happened with Alumina bonds. Alumina lost its investment-grade rating this week and slid from BBB- to BB, an event usually associated with investors losing out as the company is notionally more risky than previously.

However, bond issues often have clauses buried deep in the prospectus or PDS that state if a company loses its investment grade rating then the company will increase the coupon payable on its bonds.

This is what happened to Alumina. The credit rating downgrade triggered a step-up clause on the November 2019 notes so the coupon payable was increased by 5.50% to 7.25%.

Trading information in Alumina bonds is somewhat opaque as the bonds are not traded on an exchange, rather they are traded directly between principals: over-the-counter is the market term. According to one market maker for Alumina bonds, the yield to maturity increased from 4.48% to 5.68%. It is what one would expect when a company suffered a credit downgrade but what was unusual was how the market maker bid and offer prices also increased.

The explanation is not all that complicated. The coupon increased and once this was taken into account, even with a higher yield, the increase in interest payable to the holder meant the bonds were more valuable. Not that holders would want another downgrade; the terms of the bonds don’t allow for another step–up and, even if they did, another step up may not be enough to fully offset the additional risk.

In the 1970s there was advertisement for a type of Castrol oil and the slogan was “oils ain’t oils”. It is worthwhile for investors to remember this slogan because in the bond market “bonds ain’t always bonds”. Some bonds come with clauses which may be good, or bad, for investors and being informed of them prior to investment is a must.

29 September 2016

[Update 3 Oct 2016] Qantas has added to its debt issue with a further $175m October 2026 bonds at Swap + 280bps. The final price for the 7 year bonds was Swap + 265bps. The company has said the funds will be used to refinance short term debt.

[Original story] Qantas flagged its intention to raise capital in mid-September when it carried out a series of investor briefings. Investor briefings are usually a prelude to some sort of capital raising although the gap between the briefings and any such transaction can be anywhere from a week to many months. In this case Qantas has moved quickly and the company has now announced it will go ahead with the issue of a new series of bonds which have a fixed rate of interest and a maturity date in 7 years.

Qantas last issued bonds in December 2014 when it sold $400 million 7.75% May 2022s at Swap + 400bps. The company was rated BB+/Ba1 at the time which is deemed to be sub-investment grade. Qantas’ current credit rating has improved and is now is BBB-/Baa3, the lowest rung of the investment grade scale after a strong operating performance in the past 15-18 months.

Not only has Qantas’ business performance improved but corporate spreads over bonds have contracted since its last bond issue. The latest debt pricing is indicated to be around Swap + 270bps, or around 4.70% total yield thus lowering the company’s debt funding margin by a substantial amount. Managers to the issue are ANZ, Deutsche Bank and HSBC.

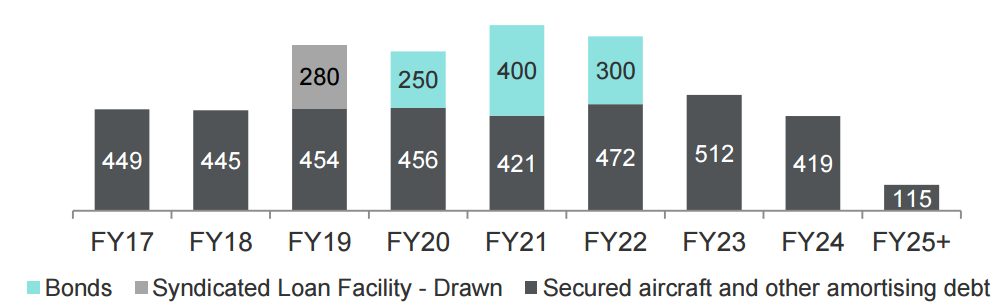

Debt Maturity Profile as at 30 June 2016 ($m)

28 September 2016

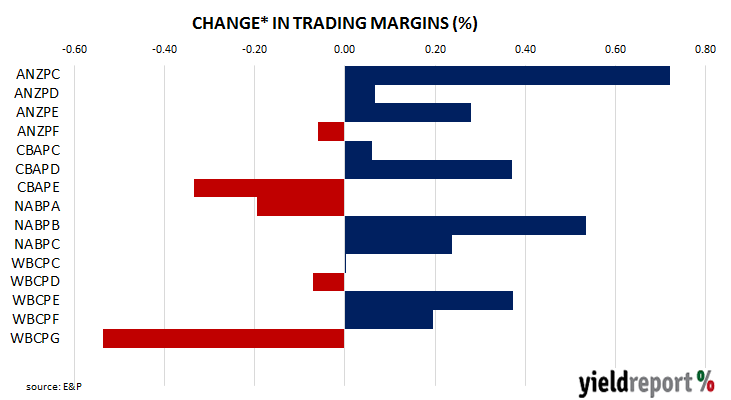

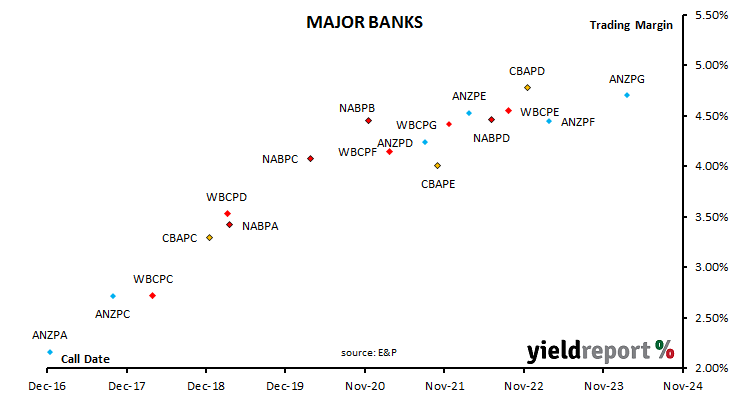

ANZ’s latest hybrid issue began trading on the ASX today. ANZ Capital Notes 4 (ASX code: ANZPG) began trading on a deferred delivery basis with the first trade at $100.63. They have a first call date of 20 March 2024 and an issue margin of 4.70% above BBSW. The hybrids closed the day at $100.85, a modest gain from the $100 issue price. Normal trading is expected to begin on 5 October.

ANZ’s new issue was announced in mid-August when government bonds yields were close to record lows. Since then benchmark yields have risen only a few basis points but along the way rises and falls have been substantial. When ANZ’s new issue was announced the median trading margin of hybrids was 395bps (15 August 2016). ANZ’s margin was set at 370bps about a week later and since then trading margins of hybrids have risen with the median trading margin now around 410bps (27 September). Readers will see from the diagram below how comparable major bank hybrids have fared since the announcement of the issue.

*16 August to 26 September

The ANZ issue raised approximately $1.6 billion, of which $900 million was used to repay CP2 holders (ASX code: ANZPA). The first distribution payment date is set for 20 December 2016 and a distribution amount of $1.0383 franked is expected. For the technically-minded, the issue date volume-weighted average ANZ share price, the price used to determine the maximum conversion ratios and the satisfaction of mandatory exchange conditions (in the event of the hybrids being converted to shares) has been announced as $26.80.

The chart below shows how trading margins stood before the beginning of trading today.

26 September 2016

Does Rio Tinto know something the rest of us, with the possible exception of Twiggy Forrest from Fortescue, are not aware of?

Rio have launched another buyback and up to USD$3 billion (AUD$3.95 billion) of Rio bonds will be redeemed early or bought back, according to the company’s latest offer.

The buyback comprises two parts; one is the early redemption of 2017 and 2018 bonds and the other is the “Cash Tender Offer” for a range of bonds issued by Rio Tinto Finance (USA) plc with maturities between 2019 and 2022. The redemption date has been set for 26 October 2016 but the overall offer closes 24 October 2016 (New York time), unless extended. A 3% bonus will be paid as an added incentive for bond holders who successfully tender their bond holdings prior to 7 October 2016.

This is Rio’s third buy back for 2016. The previous two buybacks were completed in May and July and were worth USD$1.5 billion and USD$1.7 billion respectively. Perhaps it is a little early to be calling a trend but it seems as if the “nips are getting bigger”, or so the popular Australian song goes. It is tempting to think Rio knows something about corporate bonds yields the rest of us don’t know. However, given the company’s poor record in buying assets over the last decade perhaps a more cynical view would be to ask if they are ringing the bell for a rise in bond yields?

26 September 2016

CSL’s penchant for three tranche bond deals has continued with its latest offering in the US. In a deal not widely publicised, CSL sold USD$550 million (AUD$720 million) of bonds into the US private placement market in three tranches comprising USD$150 million 10 year bonds, USD$200 million 12 year bonds and $USD200 million 15 year bonds.

Just under one year ago, CSL issued bonds under a three tranches deal; two tranches were denominated in Swiss francs and had tenors of 8 years and 10 years while the one denominated in USD had a 10 year tenor and was priced at Treasurys + 145bps. The only directly comparable tranche of the two sales is the 10 year USD tranche and in this latest deal it was priced at Treasurys + 125bps. It is another example of the narrowing in corporate spreads seen in global markets in the last year as investors go down the risk curve in a search for yield.

26 September 2016

The constituent companies for the iTraxx Series 26 have been announced. YieldReport readers will recall that the iTraxx credit default index is reviewed every March and September with a new series replacing the old. The Series 26 Australian iTraxx index has no changes and has begun trading.

The iTraxx ‘roll’

The iTraxx credit default swap indices were developed in order to bring more liquidity and transparency to the credit default swap market. The indices are tradable instruments in their own right, with pre-determined fixed rates and the prices set by market demand.

The constituents of the indices are changed every six months on 20 March and 20 September in a process known as ‘rolling’ the index. The roll occurs to ensure that the current series tracks the most liquid instruments in the relevant market.

Official pricing is collected by Markit on a daily basis by polling the trading desks at banks that are licensed market makers. The most liquid indices also have a weekly Tradable Fixing calculated in a similar fashion to the Libor fixings process. The tradable fixing is often used as a reference price for calculating payments of other structured credit instruments. At present trading in iTraxx CDS contracts predominantly occurs in the over-the-counter market.

For a fuller explanation of the iTraxx index read What is iTraxx?

| iTraxx Australia Series 26 |

| AMP GROUP HOLDINGS LIMITED |

| BHP BILLITON LIMITED |

| RIO TINTO LIMITED |

| AUSTRALIA AND NEW ZEALAND BANKING GROUP LIMITED |

| COMMONWEALTH BANK OF AUSTRALIA |

| WESTPAC BANKING CORPORATION |

| NATIONAL AUSTRALIA BANK LIMITED |

| QANTAS AIRWAYS LIMITED |

| QBE INSURANCE GROUP LIMITED |

| WOODSIDE PETROLEUM LTD. |

| MACQUARIE BANK LIMITED |

| TELSTRA CORPORATION LIMITED |

| WESFARMERS LIMITED |

| SCENTRE MANAGEMENT LIMITED (as resp. entity of Scentre Group Trust 1) |

| GPT RE LTD (as resp. entity of the General Property Trust) |

| CSR LIMITED |

| JEMENA LIMITED |

| SPARK NEW ZEALAND LIMITED |

| WOOLWORTHS LTD |

| CROWN RESORTS LIMITED |

| LENDLEASE CORPORATION LIMITED |

| AMCOR LTD |

| SINGTEL OPTUS PTY LIMITED |

| TABCORP HOLDINGS LIMITED |

| CHORUS LIMITED |

22 September 2016

Members Equity are reported to be heading back to the local debt market, only a month after issuing $100 million November 2017 bonds. However, this time it is to sell some of its mortgages via its SMHL RMBS programme to Australian investors.

The last time it had such a transaction was in July 2015 when it issued $1.5 billion worth of RMBS split among six tranches. The largest Class A1 tranche at that time was worth $1.38 billion and it was priced at 1m BBSW + 95bps.

CBA, Macquarie, NAB and Westpac have been given the nod to drum up some interest in the last week of September. Given how spreads have come in over the last twelve months it will be interesting to see how the pricing comes in for this latest offering.

21 September 2016

Back in July Australian financial markets were on hold as they waited for June quarter CPI figures and the FOMC July meeting. Now it is September and a similar period of waiting has just ended, this time for the BoJ policy decision and for the results of the FOMC September meeting. The BoJ meeting was important; the Japanese economy is one of the largest in the world. Once the BoJ meeting was out of the way, with not much in the way of policy change there, focus quickly turned to the FOMC.

Prior to the FOMC meeting the odds of a rise, based on 30-Day Fed Fund futures prices, were a relatively slim 18%, so not much weight was placed on a change occurring. Markets were more interested in the statement released after the meeting which would give a clues as to the likelihood of a December increase, given November is all but ruled out because of the presidential election.

The predictable result was of no increase. US yields fell after the meeting with 10 year yields 4bps lower at 1.65%, 30 year yields 6bps lower at 2.38% while the USD fell against the euro and the yen. Economists got to work analysing the accompanying statement and their varied views are indicative of the lack of clarity the FOMC is providing to markets but US cash markets place a near 60% chance of a December rate rise.

Westpac’s Elliot Clarke pointed out how November was a non-starter and the focus was on December. ”While the politics of November are likely to prove too difficult, a December rate hike is clearly in view. Two more will follow in 2017, but thereafter further action will prove extremely difficult.” ANZ Research agreed and said, ”One hike this year continues to be implied and the tone of the commentary regarding the economic outlook was slightly more upbeat.” NAB’s David DeGaris pointed to the wriggle room the FOMC had given itself. “Fed Chair Yellen at her press conference rate acknowledged the case was stronger for an increase in the target rate at this meeting but that it was reasonable to wait to see more progress towards its objective…She would not be specific on dates, but it seems she is setting the market up for the likelihood of a December hike, subject to a still growing economy, stable markets and overseas developments.”

21 September 2016

MyState has announced it has priced another Tier 2 subordinated note which will be issued shortly. The new notes have terms much along the same lines as the ones it issued in August of last year. As with the 2015 issue, these notes are callable in five years (September 2021) and they have a final maturity date in ten years (September 2026). They also have the standard non-viability clause required to qualify for Basel 3 capital. A triggering of this clause leads to conversion of the notes into ordinary shares, which are listed on the ASX under the code MYS.

This latest transaction is priced at BBSW + 425bps, which seems quite high until it is compared with the pricing of their notes issued just over twelve months ago. That transaction was priced at BBSW + 500bps and this latest offering from MyState indicates how demand for high-yielding assets in a low yield world has dragged spreads down. At current BBSW rates, interest on the new notes will be about 6% per annum.

MyState confirmed it had held negotiations with La Trobe Financial, as well as with “a number of parties” and it is likely the proceeds of this latest bond issue will be used to finance any such acquisition. Senior debt issued by MyState is rated BBB by S&P Global Ratings.

21 September 2016

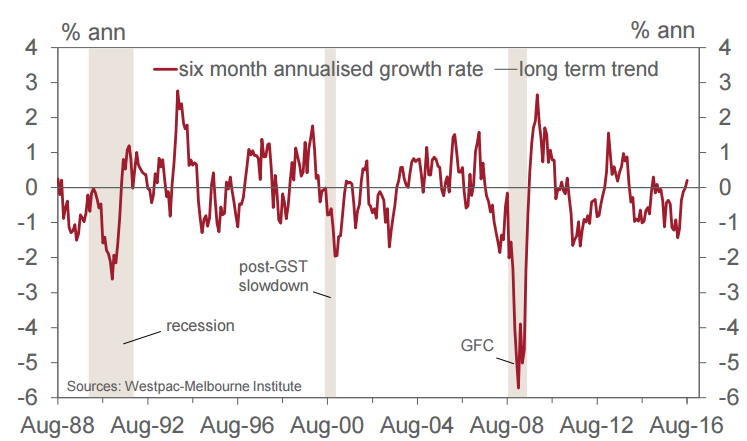

While NAB chief economist Alan Oster thinks the economy will weaken in 2017/2018, the latest Westpac-Melbourne Institute Leading Index suggests otherwise. August’s reading was released today showing a return to above–trend growth. The Leading Index figure moved from –0.01% in July to +0.20% in August and they are the first set of positive numbers in over a year.

The report, as with most economic news in recent days, has been overshadowed by a focus on September meetings of the Bank of Japan and the FOMC. However, the Leading Index provides a measurement of Australia’s likely rate of economic growth for the next three to nine months, relative to trend, and it is one of several important private sector estimates which provide markets with clues as to economic conditions in the short term.

The latest figures continue a pattern of rising numbers which has been present through all of 2016 and, according to Westpac’s chief economist Bill Evans, the figures suggests Australian GDP “is likely to continuing growing around its long run trend rate of about 3% a year.” The trend rate of economic growth in Australia has been traditionally estimated to be 3% per annum but in recent years some economists have suggested it may have moved closer to 2.75%.