18 August 2016

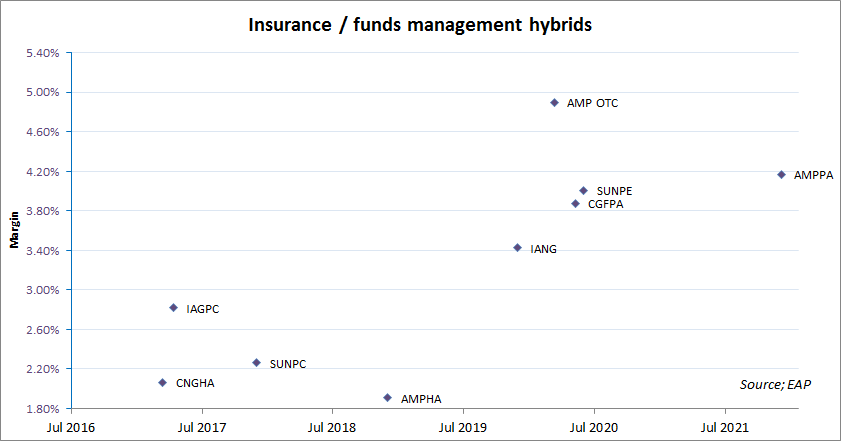

Some charts require very few words. This chart was produced by Evans & Partner on 18 August, 2016.

In a note to clients this week, E&P head of fixed income Michael Saba said, “On a scatter diagram with similar insurance/funds companies, the AMP securities offer mixed value. AMPHA looks tight compared to CNGHA, whereas AMPPA is about right relative to SUNPE. The OTC AMP Capital Notes (similar to bank Capital notes) are explicitly rated BBB by S&P and look to be excellent value relative to the listed AMP securities.”

16 August 2016

Coming so shortly after the RBA’s August Statement on Monetary Policy (SoMP) economists and other market pundits did not expect any revelations to flow from the minutes of the RBA’s August meeting. At best it was hoped some indication as to the closeness of the decision to lower the cash rate to 1.50% would be given.

Reactions in financial markets were muted but mixed. Yields on Australian 3 year and 10 year bonds both finished the day one basis point lower at 1.36% and 1.89% respectively. The local currency dropped on the release before climbing for the rest of the day which is generally a “higher future interest rates” reaction. Probabilities of official rate changes implied by cash prices were virtually unchanged.

AMP Capital’s Shane Oliver said there was “nothing new” in the minutes which had not already covered in the August SoMP. He still expects another rate cut in November. Westpac economist Matthew Hasson partially agreed but he does not think another rate cut is in the offing. “Having cut rates in August, the RBA is clearly in ‘watch and see’ mode…The Board is almost certain to keep rates on hold in September. However we continue to view the Reserve Bank as carrying an easing bias – implicit in its inflation forecasts and in our view in much of its rhetoric….Accordingly we expect that the Bank will keep rates on hold over the remainder of 2016 despite an apparent easing bias.”

16 August 2016

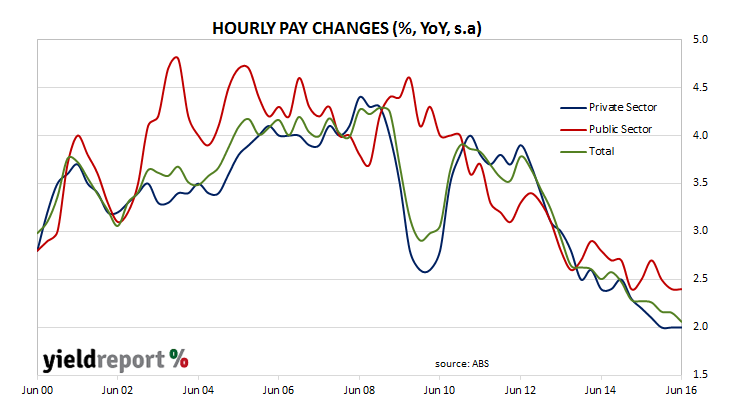

Wages growth in Australia has been slowing in trend terms since 2009 and the latest figures from the ABS suggest the trend still continues. June quarter wages growth was 0.5% (seasonally adjusted) for the quarter and in line with market expectations. Seasonally adjusted year-on-year growth was 2.1% which is down from March’s comparable figure of 2.2%

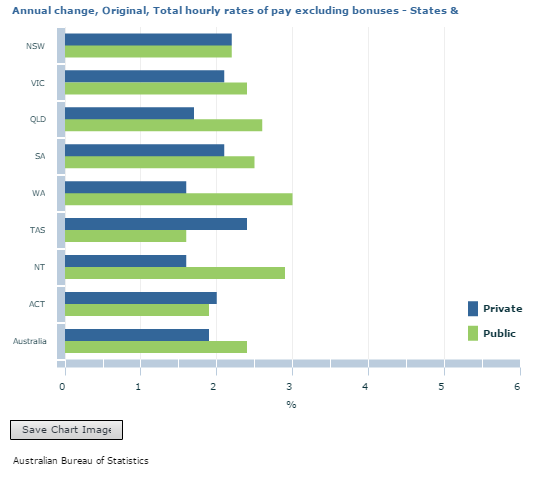

Private sector wages grew at the lowest rate since the data series began in September 1998 for the third quarter in a row. Seasonally adjusted private sector wages growth for the year to June 2016 has stabilised at 2.0% while the public sector figure of fell from 2.5% to 2.4%.

Western Australia is the standout state for two reasons. In the private sector, the state had the lowest annual increase in wages of any Australian state at 1.6%. However, in the public sector, the 3.0% recorded was the highest rate in the country.

RBC strategist Michael Turner expects wage inflation to continue falling. “Firstly, the rate of labour force underutilisation remains high, which will continue to dampen any wage pressure. Secondly, headline inflation has fallen further, which creates a low starting point for a lot of wage claims and will also weigh on inflation expectations.”

15 August 2016

Holders of various type of ANZ securities, including ordinary shares, ASX-listed notes and hybrids are currently being offered new ANZ Capital Notes 4 (ASX code: ANZPG). In the case of ANZ CPS2 (ASX code: ANZPA) holders, they have the additional offer a “roll-over” facility into the new capital notes. That is, they will be able to exchange their existing ANZPA holdings for new securities.

While a substantial number are expected to exchange their holdings for the new securities, what will happen to ANZPA holders who choose not to do so? In an announcement accompanying the details of the new ANZPG, ANZ said it will issue a “resale” notice which, under the issue terms of the ANZPA, will result in a compulsorily sale to a third party on 15 December, 2016 nominated by ANZ. CPS2 holders will then receive $100 cash plus accrued dividend, which is the equivalent of what holders would receive if CPS2 were redeemed.

Resale is subject to two conditions, the first being APRA approval and the second is ANZ must find a willing third party. APRA approval is thought to be likely as selling securities already on issue to a third party would leave ANZ’s balance sheet largely unchanged. Finding a third party has not been a problem in the past and the last example occurred when Commonwealth Bank took this route for its PERLS V (ASX code: CBAPA) in 2014.

If resale were not to occur for whatever reason, mandatory conversion would then triggered as long as certain conditions were met. The price of ANZ shares would need to fall by around 60% from current levels for the conditions not to be met. So one could be quite confident, although not certain, mandatory conversion would go ahead in the absence of a resale arrangement. Mandatory conversion would result in CPS2 holders receiving $101.01 worth of ANZ ordinary shares plus accrued dividend per CPS2. Holders would then need to sell these ANZ shares in order to be in the same position they would have been in if redemption had taken place.

10 August 2016

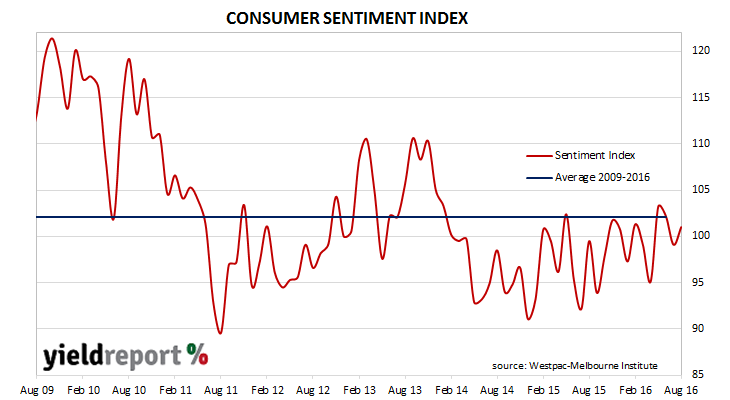

The latest Westpac Melbourne Institute consumer sentiment survey shows a rise to 101.0 from July’s reading of 99.1. Any reading above 100 indicates the number of consumers who are optimistic is more than the number of consumers who are pessimistic. The rise was expected as the survey period included the covered the RBA’s 0.25% cut in the cash rate, an event which typically leads to more consumer optimism.

Westpac’s chief economist Bill Evans said the reaction to this latest cut in the official rate was more muted than May’s reaction. “Firstly, there was a larger surprise element to the May decision with, arguably, significantly less intense media speculation than we saw in August. Secondly the standard variable mortgage rate offered by most banks was reduced by the full 0.25%, whereas in August the four major banks only reduced variable rates by 0.10%-0.14%.”

Westpac is currently expecting the RBA to keep to just two rate cuts for the 2016 year although “it is clear from the Bank’s [quarterly] recent Statement on Monetary Policy that it holds an easing bias.” Australian 10 year bond futures finished the day at 98.12, implying a yield of 1.88% and down 7bps from the previous day’s 1.95%.

10 August 2016

In the first week of August the Bank of England (BoE) reduced its official rate, known as the Bank Rate, to 0.25%, in a move widely expected after the UK’s EU “Brexit” vote. Along with the rate cut, the BoE extended some quantitative easing programmes where it would buy additional gilts (UK government bonds) and expand the programmes to include an additional £10 billion of corporate debt. Quantitative easing is the polite way of saying money printing.

The programme has already hit a snag. In the first reverse auction after the announcement, the BoE’s offer to buy £1.17bn of long-dated gilts was not rushed by sellers and there was a £52 million shortfall. The amount was not great in relative terms but the low uptake was unexpected. Yields on 20 year and 30 year gilts fell to 1.22% and 1.36% respectively on the day and then continued to fall for the next two days.

The reasons for the shortfall appear to be in two camps. The first is that investors anticipate higher prices from the BoE at future auctions, the second is that some holders of government debt are reluctant to sell. The latter might be pension funds and other investors that are mandated to hold government debt. It is quite possible they are fearful of selling their bonds lest they have to buy them back at even lower yields. The moral hazard of buying debt and fearing losses diminishes the more central banks keep buying bonds under their quantitative easing programmes.

This is another example of where textbook or academic theory meets resistance from real world scenarios.

10 August 2016

UK institutional asset manager Hermes Investment Management is currently recommending BHP hybrid bonds to investors as a substantially-higher yielding investment compared to the company’s vanilla bonds. The asset manager said investors can get a 300bps pick up by switching from BHP’s ordinary bonds to the company’s hybrids and it thinks the greater level of risk is worth the switch.

Hermes refers to BHP’s strong credit rating, reputation and the mining giant’s history of paying ordinary dividends. This latter point is important as the hybrids’ interest payments may be deferred at any time solely at the discretion of BHP. Hermes thinks is coupon deferral on the hybrids is unlikely as BHP has consistently paid dividends for decades.

The hybrids were issued last year amongst enormous investor interest. There were five tranches in all; two series are denominated in euros, two are denominated in USD and one is denominated in pounds sterling and coupons ranged from 4.75% to 6.75%.

09 August 2016

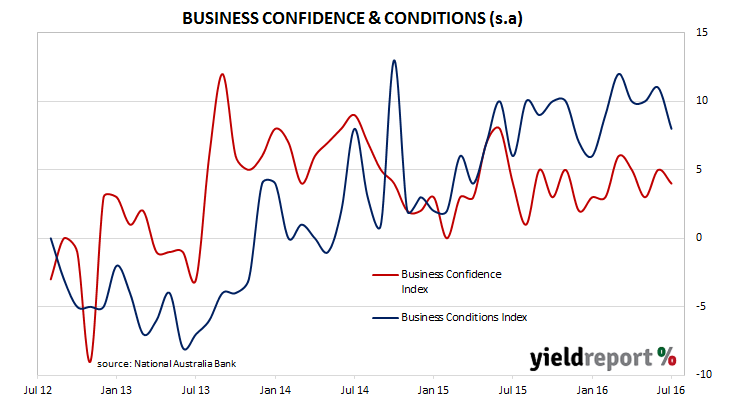

Australian businesses are still confident despite external shocks such as the UK’s vote to leave the EU and the uncertainty in the aftermath of the Australian Federal election. In NAB’s latest monthly business survey, the Business Conditions Index moved 3 points lower from a revised June figure of 11 (previously 12) to 8 while the Business Confidence Index fell 1 point to 4 from a revised June figure of 5.

According to NAB the confidence stems for elevated business conditions which are still well above the long term average. It indicates what NAB described as a “steady” recovery in non-mining activity but with “sharp deteriorations” in the transport and wholesale segments. Alan Oster, NAB’s chief economist said, “Business confidence continues to show resilience despite the number of external factors…Business conditions remain quite elevated despite easing back in the month of July.” However, some sectors of the economy are of concern. “Signs of a broadening recovery in recent months have again become more obscure following sharp deteriorations in transport and wholesale.”

These concerns have led Mr Oster and NAB to revise their outlook for official interest rates over the next 12-18 months as GDP growth dampens. Short-term positives for the Australian economy are expected to give way to weaker offshore demand and less construction spending. “While the survey points to a reasonably upbeat outlook for the near to medium-term, longer term risks are becoming increasingly apparent, particularly going into 2018 as resource exports start to level off and dwelling construction turns negative.” His view has led him to join ANZ’s head of Australian research Felicity Emmett in speculating about the “non-conventional monetary policy measures” the RBA may take in the face of continued low growth and low inflation.

Bond and currency markets reacted to the new figures in a manner which suggest lower interest rates are more likely, but the movements were not large. The AUD immediately fell from 76.5 US cents to 76.4 US cents before recovering. Implied yields on 3 year bonds and 10 year bonds both fell 2bps to 1.40% and 1.95% respectively.

08 August 2016

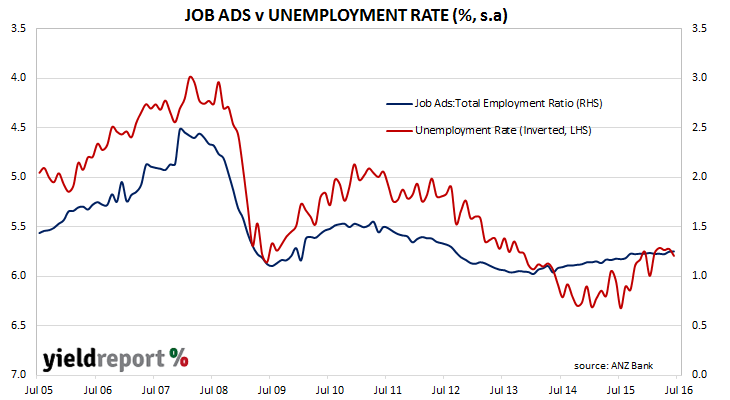

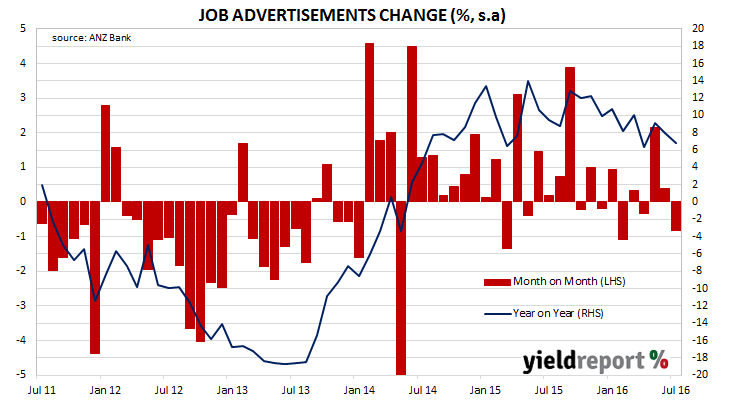

Total job advertisements fell back in July after two months of rises, according to ANZ’s monthly jobs ads survey. The month-on-month figure fell by 0.8%, although the year to July figure remains positive at 6.9%. After revisions to past data, June’s comparable figures were 0.4% and 8.0% respectively.

The survey’s results produce what economists call a “leading indicator”, or a statistic which gives a strong hint as to the direction and strength of parts of the economy. In the case of ANZ’s job ads survey, it provides a preview of conditions in the employment market, especially with regards to employer demand for labour. More advertisements generally means more hirings, a stronger economy ahead and thus lower unemployment rates.

ANZ’s Head of Australian Economics, Felicity Emmett, thinks Australia’s labour market had slowed as a result of employers’ hesitation after the Federal election and during the period surrounding the UK’s EU vote. However, she thinks their reluctance to recruit is likely to be temporary. “This impact appears to have been short-lived, with job ads picking up over the course of July, and little sustained effect from the increase in uncertainty on business and consumer confidence…With surveyed business conditions remaining upbeat and the RBA cutting rates in August, we look for a gradual improvement in hiring intentions over the remainder of the year.”

05 August 2016

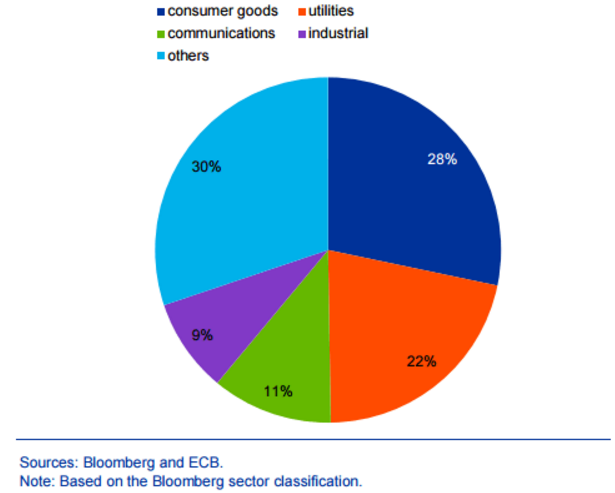

The European Central Bank has released a monthly update that contains details of its corporate bond or quantitative easing programme. The ECB has so far bought €10.4 billion of corporate debt. This number includes over 458 bonds by 175 separate issuers. Nearly all of the bond purchases (93%) has occurred in the secondary market with only 7% purchase in primary issues.

20% of all the bonds purchased have been bought at a negative yield and it would appear that a major game for the investment banks and traders is to buy bonds in the hope that the ECB will buy the bonds off them. Hardly stimulatory for the economy.

The report also included a breakdown of the bonds purchased by industry segment with the largest company sector being consumer goods.