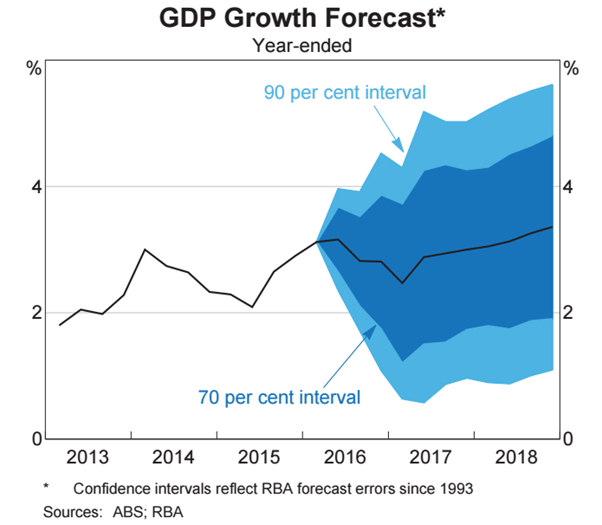

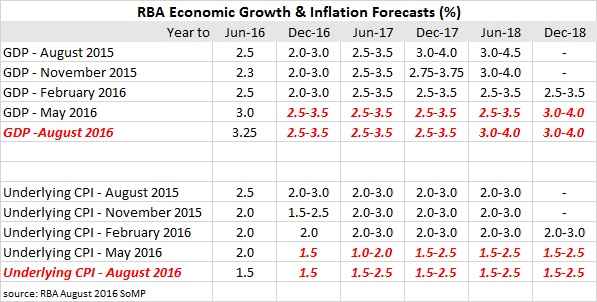

Today’s release of the RBA’s Statement on Monetary Policy (SoMP) had very little effect on markets and, according to Westpac, it “did not alter market perceptions around RBA policy.” Most forecasts from May’s SoMP remained intact, with the exceptions of underlying inflation for the year to June 2017, which was increased by 0.5% to 1.5%-2.5% and GDP for the year to June 2018 was bumped up by 0.5% to 3.0%-4.0%.

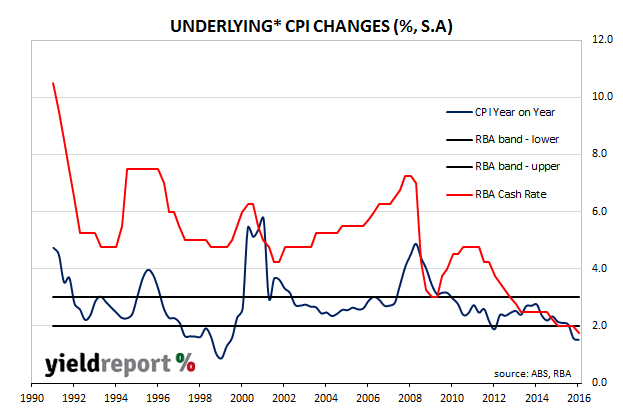

June quarter inflation was pretty much as the RBA had expected and while a weakening currency is pushing the price of imports (“tradables”) higher, consumer inflation is not expected as low wages growth and competition in retail markets keep a lid on price increases. “The large exchange rate depreciation since early 2013 is likely to continue boosting the prices of tradable items as increases in import prices are gradually passed through to the prices paid by consumers. However, domestic factors, such as heightened competitive pressure in retail markets and low wage growth, have put downward pressure on retail inflation over recent years and are expected to persist for some time.”

The RBA seems to be sending more time on the underemployment issue, something it referred to in its interest rate announcement earlier in the week. “…to the extent that gains in employment continue to be mostly in part-time employment and among workers who would like more hours, there could be more spare capacity in the labour market than implied by the forecast for the unemployment rate.”

AMP Capital’s Shane Oliver described the tone of the statement as “dovish”; that is, the statement implies an inclination for the RBA to cut rates further. He also noted the RBA’s expectation of inflation remaining below 2%, their view of growth rates below limits, a diminished housing bubble risk and mixed employment indicators which “implies [the] RBA retains an easing bias”. ANZ and Westpac shared his sentiments. ANZ Research said, “We view this, in combination with the RBA worrying about more risks to the outlook, as a strong easing bias.” Westpac’s chief economist Bill Evans said, “Our current forecast is that having responded to the ‘inflation scare’ in May with two rate cuts, the Bank will be inclined to now seek a period of stability on the policy front. However the sentiment in this statement indicates that the Bank is more open to further near term stimulus than we thought would have been the case.”