27 July 2016

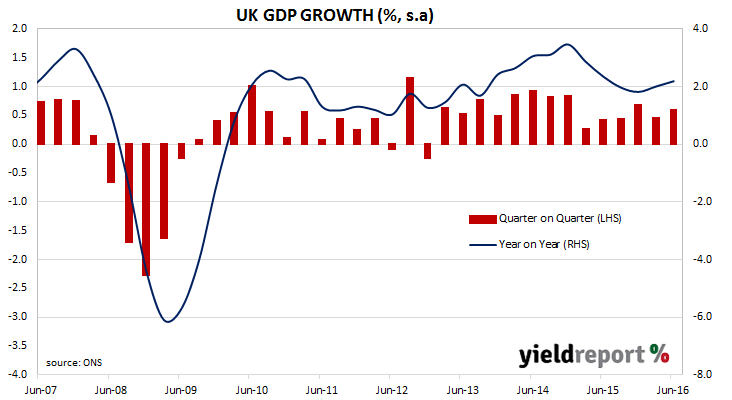

Unlike much of continental Europe, the UK seems to be doing quite well. “Advance” GDP figures were released this week indicating GDP grew at 0.6% over the June quarter, better than the 0.4% expected and higher than the 0.4% recorded in the March quarter. On a yearly basis, GDP expanded by 2.2%, up on the March quarter comparable number of 2.1%. The figures are preliminary and are likely to be amended as more data becomes available and of course the figures don’t include the fallout from the “Brexit” vote on 23 June.

ANZ responded to the latest GDP figures by saying, “…the economy was humming along nicely into Brexit.” There it would seem to end, though. ANZ suggested data released since the UK’s June 23 EU vote pointed to a drop in business confidence, less business investment and staff hiring. St George Bank economist Janu Chan expected to affect these to flow into Q3 figures. “The downward impact of the Brexit vote on economic activity will likely take a greater hit in the September quarter however, the data suggests stronger momentum just prior to the Brexit vote than previously thought.”

26 July 2016

Bank of America Merrill Lynch may not be a household name in Australia but in financial markets they are extremely well-known. At one stage it was the largest financial services company in the world and while it is not a frequent issuer in Australian debt markets in its own right, from time to time it has been known to issue bonds. The last transaction by their Australian branch was in October 2015 and prior to that, the parent company sold five year bonds in a dual tranche transaction in 2013.

This week BoAML have returned the domestic bond markets with another dual tranche five year deal. In May 2013, BoA issued $900 million worth of five year bonds split 50/50 between fixed and floating. Pricing back then was 142bps above Swap/3m BBSW. This latest transaction is weighted in favour of the floating rate note component ($550 million) rather than the fixed component ($250 million) and the pricing is more expensive in relative terms as the margin to Swap/BBSW has been set at 155bps.

BoA may not be overly-concerned by the wider spreads it will be paying on these bonds. The term structure of rates around the world has fallen since 2013. In absolute terms the yield to maturity on the fixed component is considerably lower and BBSW is now below 2% whereas in 2013 it was closer to 3%. In terms of interest expense this latest transaction will look better in their profit and loss statement. Ultimately, this is where BoA’s management and shareholders will focus.

25 July 2016

Following last week’s successful launch of Australia’s first $300 million green semi government bond issue, the Victorian government is said to be looking at launching an issue of social impact bonds.

NSW pioneered the concept of social impact bonds in Australia with its launch in 2014 of a $7 million programme aimed at reducing the number of children in foster care. The programme is considered to be very successful in both achieving its desired outcome and generating returns to investors.

The Victorian initiative will be the state’s first in the social bond space and is said to be targeted towards programmes that assist young Victorians to escape alcohol and drug addiction.

The green bond initiative was fully subscribed in 24 hours and it is hoped that the social bond initiative will go the same way. A successful programme would see a partnership between investors and government agencies providing benefits for each party.

22 July 2016

Until recently, issues of bonds and notes by unrated Australian corporates have been typically few and far between. However, so far in 2016, companies such as Peet Group, Capitol Health, Healthscope and IMF Bentham have all issued bonds and notes of various sorts. While these companies have different very different businesses, the things they have in common are they are all unrated by credit rating agencies, they are all listed on the ASX and their bonds and notes typically have coupons which fall in the range of 7.50% to 9.00%.

TFS Corporation, an ASX-listed company which owns and manages sandalwood plantations, is one of these companies, having first issued USD notes in 2012 and again in 2015. The company has announced it will be issuing USD$250 million senior secured notes which mature in August 2023, with a non-call period of three years and a coupon of 8.75%.

The proceeds will be used to repay USD$200 million of its existing USD notes and to add USD$50 million to the company’s coffers. TFS pointed out the new debt would carry interest at 225bps less than the debt it is replacing as well while extending the company’s debt maturity profile.

The notes are being sold in the US to institutional buyers as a Rule 144A transaction and thus will not be available to retail investors. However, readers interested in this segment of the market can find information on notes and bonds issued by the companies mentioned above, as well as others issued by Crown, AMP and Suncorp in the ASX-Listed Notes page.

Related articles

New bonds to pay around 7.50%

Inaugural bond issue for Capitol Health

21 July 2016

Recently, Bell Potter’s fixed income desk recommended holders of Westpac CPS (ASX code: WBCPC) switch into NAB Notes (ASX code: NABPC). Not because there is anything particularly wrong with the Westpac hybrids but simply due to the yield differential and the potential gain to be had. NAB’s hybrids have a March 2019 call date while Westpac’s have a March 2018 call date, so one would expect the NABs to have a slightly higher trading margin on this basis alone. However, the team at Bell Potter think the difference is too large and one worth exploiting.

(As at the close of business 21 July, 2016)

20 July 2016

Normally new issues of semi-government bonds is fairly sedate with around four a month on average. This week we have had three and one of them is the first of its kind in this segment of the Australian bond market. Victoria has become the first state to issue a green bond. Treasury Corporation Victoria (TCV) issued $300 million worth of 1.75% July 2021 bonds which have been certified as green bonds.

Green bonds, otherwise known as climate bonds, have been around for a few years now but until this week they had only been issued by corporate borrowers such as ANZ, NAB and Stockland. Bonds are defined as green if they fund projects which have positive environmental and/or climate benefits. TCV, as central financing authority for the Victorian Government and other state enterprises, will on-lend the funds to various Victoria agencies for use in energy efficiency, renewable energy, public transport and water treatment projects.

Green bonds are typically priced in the same fashion as standard bonds. In this case TCV’s bonds were issued at ACGB + 19.75bps, which is comparable to the spread on bonds such as NSWTC April 2021s. Investors were a mix of insurance companies, fund manager and other investors.

Related articles

Westpac joins NAB, ANZ as “green” bond issuer

ANZ green bond

Stockland €300m green bond

19 July 2016

Back in the 1970s and 1980s, discussions regarding inflation tended to focus on slaying the “inflation dragon”. Inflation had been high since the “oil shock” in the early 1970s and western economies had performed poorly in terms of growth and unemployment when compared to the previous decade. Studies conducted in later decades would indicate countries with high inflation tend to have lower economic growth rates compared to countries with low inflation.

Despite this knowledge, the US Fed has in recent years spent trillions of dollars buying bonds from the private sector in exchange for central bank cash in an attempt to raise US inflation back to its target range. However, inflation has remained stubbornly low and more like a frilled-neck lizard than a dragon. CPI figures released by the US Labor Department for June indicate consumer prices rose 0.2% for the month, 1.1% for the year and less than the 0.3% expected by financial markets. Core prices, the measure of prices which strips out food and energy prices changes, also rose 0.2% for the month but over the last 12 months the rise was a more substantial 2.3% (seasonally adjusted).

Rising medical care and housing costs were partially offset by falling prices of used vehicles. AMP Capital’s Shane Oliver said the figures suggested the “deflation threat [was] receding.” The numbers had little effect on US bond markets and on the day, the 2 year bond yield was down 1bp at 0.67% while the 10 year yield finished 2bps higher at 1.55%.

19 July 2016

Economists found little surprising in the minutes of the RBA’s July meeting. As CBA put it, “The RBA Minutes caused no reaction in a market that had already rallied.” However, a number of economists at the major banks picked up on the attention the RBA is beginning to pay to the nature of employment in Australia. The minutes refer to the underemployment rate and how it had not fallen as much as the unemployment rate. Those who are employed but wish to work more and are available to work more hours are described as being underemployed. It is another measure of spare capacity in the economy.

While noting the RBA’s new (public) interest in this issue, most economists chose to focus on one particular section of the minutes. “The Board noted that further information on inflationary pressures, the labour market and housing market activity would be available over the following month and that the staff would provide an update of their forecasts ahead of the August Statement on Monetary Policy. This information would allow the Board to refine its assessment of the outlook for growth and inflation and to make any adjustment to the stance of policy that may be appropriate.” It is this reference to “further information…over the following month” which has got economists thinking this section of the minutes adds weight to their suspicions regarding the importance of June quarter CPI which is published late this month.

Bill Evans, Westpac chief economist said, “The minutes clearly leave the door open for another rate cut in August. This will depend upon the June quarter inflation report and of course it is not clear what would be the upper bound for this report to ensure a follow up rate cut.” CBA Team economics held a similar view. “[The] RBA minutes confirm it’s all about inflation and the activity data is less relevant from a policy perspective…. So if inflation is low enough in next week’s CPI data the best guess is still a rate cut in August.” Reactions from other banks were quite similar.

Financial markets took little immediate notice of the release, although the local currency was a little weaker, which implies the foreign exchange market thinks the chance of lower future interest rates is higher than before. The yield on Australian 3 year bonds finished the day at 1.45%, down 6bps while 10 year bonds closed at 1.935%, down 7bps. The probability of an August rate cut implied by cash contracts rose from 58% to 64%.

18 July 2016

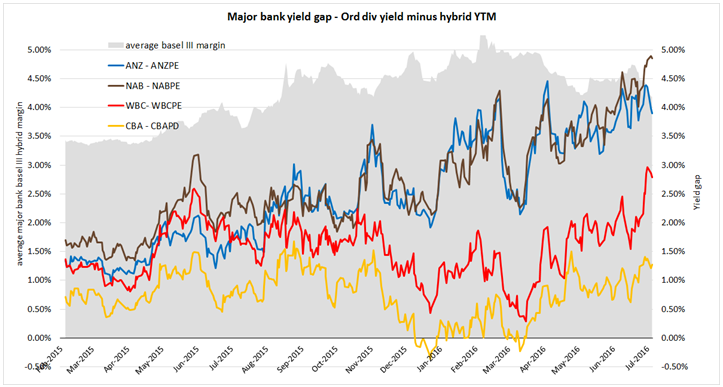

New hybrids issued by three of the major Australian banks have been snapped up by investors at attractive yields. Initial yields for CBAPE’s, NABPD’s and WBCPG’s (Westpac) were the bank bill rate plus 5.10%, 4.95% and 4.90% respectively. Issue volumes were all significantly increased due to demand and all three issues are trading well above their $100 issue price, effectively pushing the yields lower post-issue.

As often happens, new hybrid issues spark increased investor interest in the sector as investors revisit existing hybrid issues and search for value. With global bonds hitting record lows, the yields on hybrids have been seen as attractive. Investors have been pushing down trading margins in general but have they gone too far?

One analyst who thinks they might have in the short term is Michael Saba, Head of Income Products at Evans and Partners. He recently looked at the relationship between trading margins of bank hybrid securities and the dividend yields on banks’ ordinary shares. The chart below shows that relationship over the past year.

There are similar characteristics between investing for bank dividends and investing in hybrids but significant differences in risks as the two securities are in a different part of the company’s capital structure. Hybrids carry less risk than pure equity and the question investors should always be asking is “Am I being compensated enough for the risk I am taking?”

The chart below shows that the gap between dividend yields and trading margins on hybrids has been widening and what Mr Saba found was that is that hybrid securities of most banks appear to be expensive relative to the ordinary shares. This suggests that hybrid yields are too low or that dividend yields are too high. “Either the stock price must rise or ordinary dividends be cut to reduce the share price yield, or hybrid prices fall to increase the hybrid yield to in turn reduce the yield gap.” Whilst he acknowledged the variance over time of the relationship and says the yield gap itself is not a reliable indicator of hybrid prices or yields it is an interesting observation and reflects on the risk choices that investors appear comfortable making.

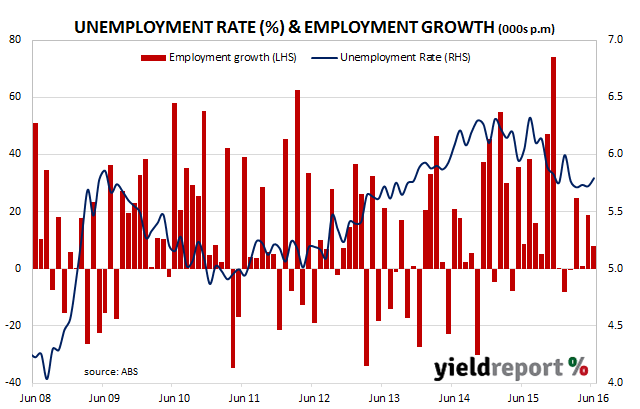

14 July 2016

Australia’s employment market continued to expand for the fourth month in a row. The ABS released June employment estimates which indicated the total number of people employed in Australia in either full-time or part-time work increased by 7900 during the month. Even so, the unemployment rate increased from 5.7% to 5.8% as more people looked for work. The participation rate rose from 64.8% to 64.9%. Unlike May’s numbers, full time employment was the driver behind the rise in numbers employed as full-time employment increased by 38,400 while part-time employment fell by 30,600.

The local currency rose 0.30 US cents on the news and then proceeded to move higher for the rest of the day/morning. 3 year and 10 year bonds initially spiked before falling back to end the day 2-3 bps higher at 1.545% and 2.00% respectively.

ANZ said “the labour market remains in ok shape, although the pace of jobs growth has eased and unemployment has ticked higher.” The bank cautioned that employment advertising surveys suggest employment growth is likely to ease further, despite positive business surveys.

The bank still expects the RBA to reduce the official rate in August. Westpac was more positive. Senior economist Andrew Hanlan said, “Our assessment is that the labour market will regain momentum over the second half of this year, consistent with positive fundamentals…. Our jobs index has strengthened over recent months, as private business surveys report actual business conditions are at elevated levels, pointing to the prospect for solid employment gains near-term”

There is still more than a little doubt as to the veracity of the data presented. Commonwealth Bank in its review of the figures said, “We remain sceptical of the quality of the jobs data following revisions to the survey back in 2014.” Other observers commented on the apparent contradiction of a fall in total hours worked in conjunction with a rise in full-time employment at the expense of part time employment. Such a combination is counter-intuitive at first glance although it could be down to part-time employees working fewer hours or it may be the result of sampling errors.