10 June 2016

The central bank strategy of implementing negative interest rates in order to coerce banks to lend money and stimulate the economy has arguably not worked. Global aggregate demand has remained weak and borrowers have been reluctant to borrow and invest.

Levying a charge on banks depositing excess funds with the central bank, that is, using a negative interest rate, has meant the profitability of banks has also come under considerable stress. As rates move lower and lower, bank profits are reduced. Banks are reluctant to pass on negative interest rates to customers so profit margins are being squeezed. The policy being followed is arguably making the banking sector weaker still.

To combat this, Reuters has reported that one bank, Commerzbank of Germany, has been investigating buying storage vaults to hold excess bank notes. Rather than placing cash with the ECB it may be cheaper for the bank to hold the billions of euros of physical cash in its own storage vaults. While the bank has so far refused to comment on the story it does highlight how ineffective a NIRP (Negative Interest Rate Policy) can be if people prefer to deal in cash.

Central banks are desperately hoping their tactics work and economies start to pick up more sharply than they have been. However, the limits of central bank policies may be approaching and this is a problem for all of us.

10 June 2016

Leading local bond fund manager, Vimal Gor from BT Investment Management, has used his latest monthly report to warn of his new base case that the $AUD will fall to 40 US cents. His original call was for the $AUD to fall to 50 US cents but he now believes this is too optimistic. Vimal predicts the Australian cash rate will fall to 1.00% and, as a consequence, the exchange rate will fall.

This are not the thoughts of someone that has just realised things are worse than predicted. Vimal has held a longstanding and public view that the central bank will be forced to cut rates in Australia as growth falters and price deflation is imported from China, Europe and Japan. His bond fund has consistently been amongst the best performing in the country as interest rates have continued to fall.

In essence the view he holds is that central banks around the world, principally European and Japanese central banks, are losing the fight against low growth. Cutting interest rates to historically low levels (Japanese 10 year bonds are trading at around -0.12%, German 10 year bonds are trading at a record low 0.04%, Swiss bonds out to around 22 years are trading at negative rates) to boost growth and demand has not had the effect that was hoped for. Consumers who are worried about the future are not spending.

In Australia, we have a large reliance on foreign capital to fund our lifestyle and budget deficits, hence the further we cut rates, the less attractive we are as an investment destination. Once foreign investors realise this, foreign capital will flee, seeking a safer investment destination. The early warning signs of this are the steepening yield curve between 10 years and 20 years. Despite yield curves flattening over the globe, our curve at the long end is steepening suggesting investors are demanding more premium for the risk they are taking.

With a flagging economy and a deteriorating federal budget position, unless there is some sort of growth miracle the day of reckoning will come. And when it does the $AUD will face a precipitous collapse that will force our hand to restructure our economy, pay back debt and curb spending.

Vimal Gor’s full report can be viewed here.

09 June 2016

It is not just the banks which feel forced to issue new securities to deal with the fallout of the GFC and the new financial regulations which are being implemented as a result. QBE Insurance Group has mandated banks for another USD 30 year (non-callable for 10 years) Tier 2 subordinated transaction.

QBE typically issues 30 year notes with interest resets and call options, having last issued USD and sterling denominated notes of this structure in May. Those transaction were to refinance the repurchase of USD$600 million of 2041 subordinated callable notes which had been issued by QBE capital Funding and £291 million subordinated callable 2041s were exchanged for Tier 2 instruments.

It seems the theme behind these transactions is the new notes are all deemed to be Tier 2 capital. While details of the latest transaction are not yet available, the fact the new notes will be Tier 2 implies they have a non-viability trigger for conversion into ordinary shares clause and an interest deferment clause in the same manner as the USD and sterling notes recently issued.

08 June 2016

ANZ has announced the pricing on its USD$1 billion issue of ANZ Capital Securities which was first flagged at the end of May. Indicative pricing of the fixed-rate securities was at 725bp but by the time the issue was officially launched it was reported to have tightened to 700bps. The final pricing settled at 675bps and is a result of the massive demand generating around USD$18 billion worth of orders. The hybrids will be issued through ANZ’s London branch.

The offshore issue will potentially change the face of hybrid securities market in Australia. The ATO has given a ruling that will allow banks to issue hybrids offshore without attaching franking credits to distributions. This has increased the ability of local banks to issue large amounts of hybrids into institutional markets overseas in a short time frame may end up limiting the volume of hybrids available to local retail investors. This, in turn, may drive the trading margins of local hybrids lower.

A number of local hybrid specialists including Bell Potter, Evans and Partners, Elstree Funds Management agree with Shaw and Partners saying the implication of this latest issue is “there is clearly an alternative source of demand offshore, if required, for Australian major bank AT1 issuance.” Domestic hybrid issues remain a lower cash cost for the banks because of the value of franking credits to domestic investors but “yield hungry” offshore investors will be attracted to high unfranked yield of these sorts of securities.

YieldReport will maintain a close watch on hybrid margins but already it would seem that local demand is picking up.

08 June 2016

Rio Tinto is back in the bond trading business. Having bought back $1.5 billion dollar of bonds in April, the global mining giant has announced it will offer to repurchase up to USD$3 billion of bonds with maturities in between 2018 and 2022. Rio says the offer is the result of having a “strong liquidity position”, which is perhaps another way for Rio to say it is currently holds excessive amounts of cash and/or cash equivalents. What this implies is Rio will not be issuing new debt with lower coupons to replace the debt. It also implies Rio’s treasury department sees these bonds as offering a higher return than the return offered by it cash holdings.

However, unlike an investor which buys bonds as an investment, as a bond issuer Rio is already effectively “short”. It will be probably repurchasing these bonds at prices higher than the prices at which they were sold. According to prices on the Berlin Borse, all these bonds, with one exception, are trading at more than face value. There will some losses, which was also the case with the bonds Rio repurchased in April.

The offer comprises two components; the “Any and All” offer for two series of May 2018 bonds and a “Maximum tender” offer for various bonds with maturities in 2020, 2021 and 2022. The Any and All component will be repurchased at (2018) Treasurys + 50bps while the Maximum Tender bonds will be repurchased at a spread of between 65bps and 140bps to the relevant Treasury security yield. The face value of two series of bonds in the Any and All component amount to about USD$2.85 billion and any funds left over will be available to buy bonds in the Maximum Tender component.

Related Articles

Fortescue in another “reverse” tap

Fortescue’s canny bond sales

Fortescue mines bond yields

Fortescue to buy bonds back at a discount

Fortescue bonds under issue price

07 June 2016

The RBA left the cash rate unchanged at its June meeting in a widely-expected decision. What did change, however, is what is referred to as the RBA’s “bias”; that is words, sentences and phrases which economists and observers which can imply the direction of the banks next move.

Westpac said they expected to see words from the after-meeting statement such as “scope”, “time being”, “assess” and “further easing” to indicate an easing bias. Instead it got what it considered to be a neutral statement. Commonwealth Bank reached the same conclusion. “A lack of any overt easing bias was surprising and the language conveyed a reluctance to move…Nothing now seems likely before August, after the election on July 2 and the Q2 CPI print in late July.” ANZ was just as surprised as Commonwealth Bank. “The lack of an explicit easing bias makes an August rate cut a much closer call than we had previously thought.” Even so, ANZ still expect another rate cut down to 1.50% given the RBA’s own inflation forecasts. NAB seemed less surprised than the other banks but arrived a pretty much the same conclusion. “The Statement suggests the RBA’s May easing is currently seen as sufficient to return inflation to target and achieve sustainable growth. That said, inflation remains important and a low Q2 CPI print (due out 27 July) could still trigger a cut further down the line.”

Cash markets responded to the RBA statement by reducing the probability of a July rate cut from 26% to 14%, while an August cut went from 64% to 48%.

07 June 2016

Switzerland has announced an issue of long bonds which mature in June 2029, at the lowest coupon on record. In fact the coupon will be zero per cent, yes 0.00%. Investors will be placing their money with the Swiss National bank for 13 years for no return.

Swiss bonds with maturities out to 22 years are already trading in the secondary market at negative yields but this is the first time the country has issued bonds with a zero coupon. The fall in yields has been driven by an unprecedented combination of investor demand, negative cash rates and the ECB buying billions of euro worth of European bonds every month. While Switzerland is not actually part of the European Union, investors fleeing the euro have poured money into the Swiss franc and subsequently into Swiss bonds.

With interest rates negative, banks are charged up to 75bps per year to park their money at the central bank. This leaves investors who own zero coupon bonds better off than if they had parked their money at the Swiss National Bank. It’s a strange world.

06 June 2016

Tascorp has announced it will be issuing a new February 2028 bond. It has mandated several investment banks to raise a maximum of $200 million via a syndication process for the 11.5 year bonds and pricing for the deal is expected shortly.

The issue of bonds with tenors in excess of 10 years may be part of a recent trend among semi-government issuers. In April Tascorp issued $55 million worth of a new bond series with a 30 year maturity and then followed up with a $45 million tap in May. It is likely that this is part of a deliberate strategy to lengthen the state’s maturity profile with the average tenor of all semis rising. So far in 2016 the average has been 11.5 years, in 2015 it was 8.4 years and in 2014 it was 7.4 years.

Related Articles

Apple Isle’s 30 year bond play

06 June 2016

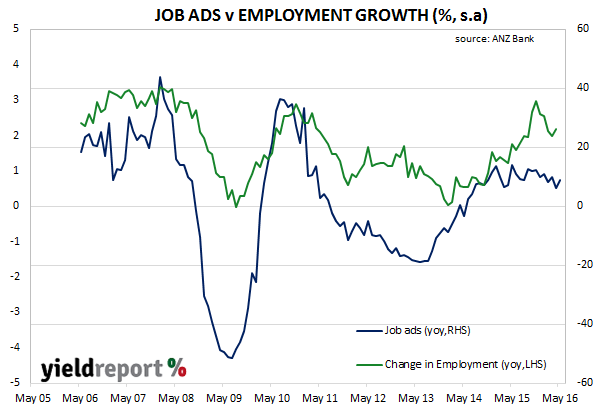

ANZ’s most recent monthly job ads survey was released this week and it showed total ads rose by 2.4% (seasonally adjusted) in May and up 9.1% over the year. The comparable April figures were -0.6% and +6.4% (after revisions) respectively. Internet ads were up 2.9% for the month (+9.9% for the year) while newspaper ads fell 12.6% (-31.1% for the year). Advertising through newspapers now represents 1.3% of all job advertisements and is now essentially irrelevant from a sampling point of view.

ANZ described the results as “encouraging”, with the economy’s transition to non-mining activity occurring. “The rise in job ads is consistent with the strength in business conditions, which point (sic) to ongoing solid growth in the economy.” ANZ’s former senior economist Justin Fabo said the numbers indicated second quarter jobs growth will be slower “but still relatively solid.” AMP Capital’s Shane Oliver said the data implies the employment market is “still strong after appearing to slow a bit.”

06 June 2016

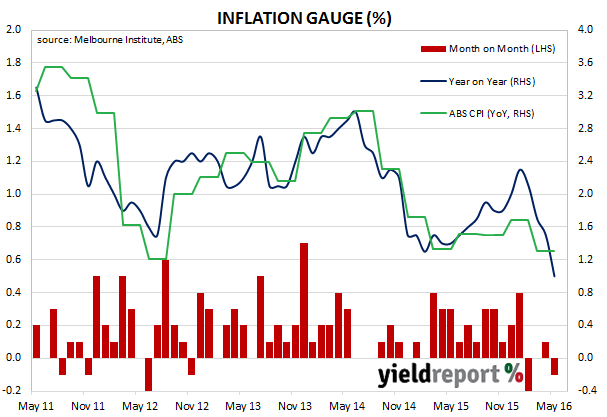

Readers may wonder why there is so much discussion about raising the rate of inflation back to the RBA’s target band of 2% to 3%. Readers may even wonder why the RBA has a target band in the first place. Whereas consumers generally don’t like inflation, except in their own salaries and wages, the RBA and central banks in general want a modest amount of inflation for various policy reasons.

The latest Inflation Gauge reading for May shows consumer prices fell 0.2%. Fruit, vegetables, holiday travel and accommodation fell. These items were offset by prices rises from fuel, insurance and financial services. 12 month inflation (blue line below) fell for a fourth month in a row, from 1.5% to 1.0%. The trimmed mean measure of the Inflation Gauge fell by 0.2 per cent in May (+0.2% in April).

The Melbourne Institute’s Inflation Gauge has a high correlation to the official ABS CPI data; a quick look at the chart illustrates this relationship. The advantage it has over the official data is it is released monthly and therefore it gives financial markets a good clue as to where CPI figures are heading. Markets can then speculate on the likelihood of the RBA raising or lowering rates as they know a rate cut is more likely when inflation is falling and a rate rise is more likely when inflation is rising.

According to the Melbourne Institute’s Dr. Sam Tsiaplias, however inflation is measured, it is lower than the RBA’s target. “Looking at either the headline or trimmed mean measures, annual inflation appears to have fallen to about 1%. Inflation excluding volatile items has also fallen to 1.5%…Whichever measure happens to be preferred, it is fairly clear that there is a sizeable gap between target and actual inflation.”