07 April 2016

The law of unintended consequences has reared its head yet again. The Bank of Japan (BoJ) has a set target of purchasing $80 trillion yen (AUD$1 trillion) worth of Japanese Government Bonds (JGBs) per year. In buying JGBs from investors in the secondary market, the central bank hopes two things will happen. First, investors will have more cash and thus are more likely to spend it on goods and services in the Japanese economy. Second, the BoJ’s purchases keep the price of JGBs high and thus the yield low, thereby providing an incentive for investors to spend part of their cash holdings rather than save/invest it. The hoped-for result is a moderate level of inflation which is what central banks generally like.

However, such a plan becomes unstuck when holders of JGB’s don’t play ball and sell. Apparently, this has been happening and trading in some JGBs has been observed as haphazard. As the BoJ ends up owning an ever-increasing percentage of the total JGBs on issuer, there are fewer and fewer other holders in a position to sell them.

An IMF working paper by Serkan Arslanalp and Dennis Botman addressed this issue. “There is a minimum level of demand for JGBs from banks, pension funds, and insurance companies due to collateral needs, asset allocation targets, and asset-liability management (ALM) requirements…This raises the question how long the current unprecedented pace of JGB purchases, equivalent to about 1 percent of GDP every month, or near 10 percent of the market on an annual basis, can continue before the BoJ runs into speed limits.”

In response to this upcoming roadblock for BoJ monetary policy, Jefferies Group strategist Sean Darby proposed the BoJ consolidate some of its existing holdings into perpetual zero coupon bonds. He thinks the BoJ will indicate its intention to do so after a meeting later this month and says its decision to implement a negative official interest rate in January was part of its plan to push yields at the longer end of the curve lower in preparation for the issue of such bonds. They would cost nothing to service, never have to be repaid and the Japanese Government could continue to issue JGBs to finance spending increases or tax cuts, which the BoJ could then buy as part of its bond purchase programme.

06 April 2016

Several banks mandated by Suncorp-Metway are close to finalising a new 5 year benchmark issue on its behalf. Suncorp has $750 million of April 2016 FRNs due to mature in a week’s time so it is not a stretch to anticipate a $750 million raising. The last foray of Suncorp Group’s banking division into debt capital markets was in mid -October when it issued $750 million worth of fixed and floating bonds with October 2020 maturities. That deal was priced at Swap/BBSW + 125bps and while the new issue is reported to be in the BBSW + 140bps region, it will be interesting to see how Suncorp’s latest debt issue fares.in regards to its final pricing. The ECB expanded its bond purchasing programme to corporate bonds in mid-March and credit spreads for investment grade issuers have tended to contract since then but Suncorp may end up paying more all the same.

06 April 2016

The RBA left the cash rate at 2.00% at its April 2016 board meeting earlier today. This makes it the tenth meeting in a row where the official cash rate has not changed. Economists were not expecting any change and cash markets had implied a 6% chance of an April cut. However, cash markets have factored in much greater chances of rate reductions in May or June and while banks such as Westpac think the RBA will not cut rates this year or next, they are not totally discounting the possibility. “We have consistently argued that any move from here, at these low rate levels, is only likely to occur at the February, May, August, and November meetings.” RBA meetings in these months precede the quarterly Statement on Monetary Policy which Westpac thinks will be needed to justify any change. AMP Capital’s Shane Oliver said the RBA retained its “easing bias” and he still anticipated another rate cut while conceding it was a not a done deal.

ANZ‘s Justin Fabo singled out the RBA’s attempt to “jawbone” the currency down but the attempt, if it was one, failed as the Aussie gained half a cent against the greenback. About the only other thing which looks vaguely controversial is the implied dig at the world’s central banks. The RBA statement noted how “globally, monetary policy remains remarkably accommodative” and this was taken as a dig at several central banks’ policies of zero or near-zero interest rates.

A full text of the statement is available at http://www.rba.gov.au/media-releases/2016/mr-16-08.html

06 April 2016

TCorp, the financing arm of the New South Wales Government, has announced it intends to issue a new line of March 2028 bonds in order to raise at least $500 million. TCorp said the new bonds would be sold via a syndication process later this week and were intended to lengthen TCorp’s debt maturity profile. It intends the new bonds to be given “benchmark” status, which means the issue size will be large and its liquidity supported in the secondary market.

TCorp has been quiet for the last 12 months but given the state of the NSW budget, this is perhaps not a surprise. NSW is one of only two Australian states running a budget surplus and therefore it does not require the sale of bonds to finance a budget shortfall. Its last transaction in the domestic bond market was in April 2015 when it bought back $1.9 billion of April 2016 FRNs and sold an equivalent face value of October 2020s, leaving the remaining $600 million to be redeemed later this week.

06 April 2016

Last month the Australian Securities and Investments Commission (ASIC) launched legal action against ANZ relating to the bank’s involvement in the manipulation of the bank bill swap rate (BBSW). ASIC had been conducting an investigation of the 14 member BBSW panel since mid-2012 following similar investigations by UK authorities relating to the comparable British benchmark known as LIBOR (London Inter-Bank Offer Rate). These benchmark rates are used to establish the final rates for many thousands of corporate loans and investments. As part of its brief of evidence, ASIC tendered chat room and telephone conversations which ASIC says is evidence of ANZ traders’ plans for moving the BBSW rate in a certain direction.

This week, ASIC has launched action against Westpac and ASIC will allege in the Federal Court that Westpac and its agents created an artificial price for bank bills on 16 occasions between 6 April 2010 and 6 June 2012. Banks such as Westpac facilitate investments, swaps or hedging transactions for their customers by taking the opposite side of the transaction. Many of these transactions are priced using BBSW as a reference point and movements in BBSW therefore effect the value of a bank’s “house” positions which are accumulated over time. There are also the banks’ trading desk positions, which are essentially bets made by bank employees, many of which are a priced relative to BBSW. Major Australian banks have the financial firepower to temporarily move prices at important times and this is what ASIC has alleged Westpac has done. “ASIC alleges that Westpac was seeking to maximise its profit or minimise its loss to the detriment of those holding opposite positions to Westpac’s.”

Two banks have already admitted some wrong-doing. Both UBS and Royal Bank of Scotland have given enforceable undertakings to the ASIC in 2014 after admitting their traders had engaged in conduct at odds with their obligations. There are likely to be further claims made against some of the other banks in the BBSW panel and although ASIC has said publicly that it would prefer not to have to go to court, it is clearly prepared to pursue those it believes have breached their obligations.

05 April 2016

A Canadian corporate issuing bonds into the Kangaroo market is not unusual; Toronto Dominion, the Provinces of Manitoba, Quebec and Ontario have all been regular issuers into the Australian bond market over the years. This time it is Canadian Imperial Bank of Commerce’s (CIBC) turn but unlike its fellow Canadian players in the Kangaroo market, it tends to issue covered bonds and usually ones which pay floating rates of interest. CIBC had $700 million worth of March 2016 FRNs mature recently and they are possibly back again for some sort of replacement funding. An investor update is expected to take place shortly and if it is a prelude to a debt capital raising they would probably hope to achieve pricing in the same vicinity as their last covered bond sale in June, which raised $300 million at BBSW + 65bps.

04 April 2016

Job advertisements were up 0.2% in March, suggesting that the jobs growth we have seen for the past 2½ years may be levelling out, although job ads rose 10% year-on-year. ANZ senior economist Justin Fabo said the job ads have been broadly unchanged since November 2015, signalling hiring intentions are easing. “To some extent this is unsurprising given the strong pace of jobs growth over much of 2015 and modest improvement in the unemployment rate,” he said.

04 April 2016

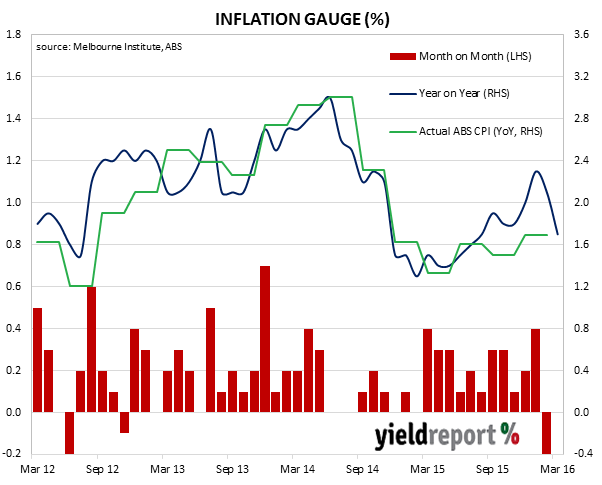

Consumer prices were largely unchanged in March as the prices of fruit, vegetables and electrical equipment and computers offset price rises tobacco, travel and accommodation. According to the latest reading of the Melbourne Institute Monthly Inflation Gauge, inflation over the 12 months to March fell from 2.3% to 1.7%.

The Monthly Inflation Gauge has been a good forecaster of headline inflation numbers (see below chart) which are an important component in determining interest rate policy.

One of the underlying reasons for low headline inflation rates around the world has been falling oil prices. West-Texas Intermediate (WTI) was at USD$100 per barrel in April 2014. By April 2015 it had halved in price and in and in February this year it reached a low of USD$28. However, WTI has risen recently USD$38 per barrel and so headline inflation measures which include consumer fuel prices are likely to see fuel prices add to inflation in the future. “Core” measures of inflation do not include fuel and so have consistently been higher than headline figures in the last two years.

The Melbourne Institute’s Dr Sam Tsiaplias said, “After two months of substantive falls in the price of automotive fuel, this month saw a small increase in the fuel price. If we exclude volatile items, quarterly inflation rises to about 0.8 per cent which indicates the significant impact that oil prices have had on inflation in the last few months.”

01 April 2016

CBA has raised a total of $1.45 billion with its latest hybrid offering, PERLS VIII. The offer has now closed after initially seeking to raise around $1.25 billion. The PERLS VIII hybrids replace the maturing PERLS III hybrid and will pay investors the 90 day bank bill rate plus a margin of 5.20%. This represents an initial return of 7.50% pa including franking credits.

This issue was not without controversy. Investors will recall CBA’s previous issue (PERLS VII) that was undertaken at the height of the demand for yield. Investors put their hand up in droves and CBA sold $3 billion worth at a record low margin on BBSW + 2.80%. This latest issue is at a historically high trading margin for a major bank, although it was below other hybrids’ margins available in the secondary market when it was announced. This includes the CBA PERLS VII that had been continuously sold off since its issue date and has never traded above the $100 issue price. Analysts said that the new issue was priced too low but the PERLS VIII offer was rushed with orders. Broker ‘firm’ bids had to be capped at $650 million.

All in all it has been a successful issue from CBA.

01 April 2016

S&P cut the outlook for China’s credit rating in a widely expected move. The outlook was cut from stable to negative with the sovereign debt rating for China remaining at AA-. The move follows an outlook downgrade earlier in March from Moody’s. The change in outlook is based on several factors including: the Chinese government reform agenda proceeding more slowly than anticipated; an ongoing weakening in financial metrics; a continuing fall in reserves; and, nagging doubt about the ability of authorities to carry out large scale reforms.