Pepper is in the middle of arranging a nine tranche “non-conforming” RMBS issue. Initially the issue was worth $600 million in size but demand must have been good because it has been up-sized to $700 million. It’s non-conforming as a substantial proportion of the loans are to self-employed borrowers and/or borrowers with prior “credit impairment” histories. No loans in the pools have mortgage insurance. Caveat emptor!

News

Pepper “non-conformist”

22 March 2016

Suncorp seeks funds in Asia

22 March 2016

It’s been a few months since Suncorp last came to YieldReport’s attention. Back in January the banking and insurance group issued USD$550 million of October 2020 FRNs into the US market in what seems to be the beginning of a floating-rate note trend amongst Australian issuers. At the current point in the interest rate cycle one would think they would want to issue fixed-rate debt but the fact they issued floating would seem to indicate investors won that battle. Suncorp is now reported to be organising a tour of Asia in mid-April with the aim of another debt capital raising. It will be interesting to see if they continue with the floating-rate theme.

Central banks leave punch bowl out too long

21 March 2016

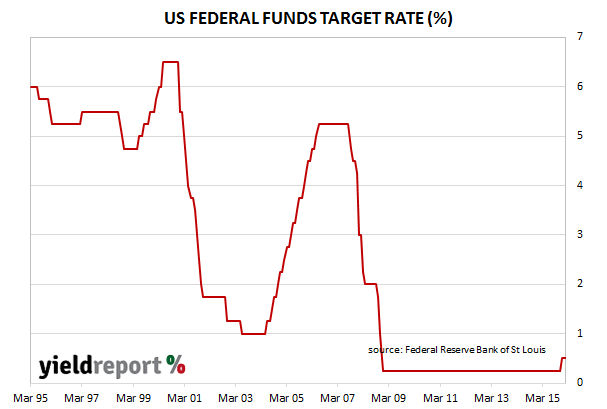

William McChesney Martin, Chairman of the Federal Reserve in the 1950s and 1960s, is quoted as saying the “Federal Reserve is in the position of the chaperone who ordered the punch bowl removed just when the party was really warming up.” In a client note titled “Party Time”, Simon Masnick, Westpac’s global head of fixed income trading, reckons Janet Yellen and the Fed will ignore this tenet of central banking because they are sick of taking the rap for Europe and Japan. He thinks the Fed has capitulated to a desire for a weaker USD, which is entirely inconsistent with rising US interest rates in a world filled with negative ones.

Despite a US economy doing well and “years into a sustained recovery” the Fed went dovish in recent months because it did not want the US to be the economy which “takes the strengthening currency pain for the rest of the world to gain”.

“Janet Yellen and her FOMC decided enough was enough…And so they sprung a dovish surprise on a market that, mistakenly, believed the Fed was in a tightening cycle.”

He has two pieces of advice to bond investors. The first is, don’t fight central banks too early. “Cash bonds are the best place to play, following the adage you want to be on the same side as the ECB and they’re buying bonds, not selling protection.”

The second is to buy inflation-linked bonds. This advice is based on the view the ECB and Fed will be left with a “policy mistake”, which implies the policies of the ECB and the Fed will lead to an outbreak of inflation which vanilla bonds will not have taken into account. “Sure the amount of slack in the US economy is plunging to new lows; sure there are signs of inflation creeping in everywhere; sure the economy still has emergency monetary policy settings despite being years into a sustained recovery…throw in the added Tabasco of an ECB that will buy any bond ever issued in Euros, ever, forever, and you’ve got a big QE/dovish shot in the arm.” In other words, too much money for too long will spark inflation beyond what markets are currently expecting.

More beer

18 March 2016

Anheuser Busch InBev followed up January’s monster bond sale with what is reported to be the largest-ever sale ever of corporate bonds denominated in euros. Bond purchases by the US Fed and the ECB which have pushed yields towards record lows have made conditions ripe for large respected corporates to issue bonds at multi-decade low interest rates.

Initially AB InBev was said to be looking to raise €9.00 billion (AUD$13.5 billion) but it took advantage of the €32 billion in orders from investors and ended up issuing €13.25 billion (AUD$20 billion/USD$15 billion) of bonds across six tranches. While this may be large, it is modest compared to the monster USD$46 billion deal it completed in mid-January , it still makes most other bond sales look puny in comparison.

ORGHA is “great short-term opportunity”: Morgans

17 March 2016

Morgan’s fixed income analyst, James Lawrence, has joined the number of analysts who are keen on Origin Notes as a short term investment. In a recent research note he wrote, “Based on a price of $97.70 we forecast a yield to call for investors of 9.45% which we view as compelling.” He expects the notes to be called in December 2016 because of the company’s previous statements regarding its intention to redeem at that time and the loss of the notes’ “equity credit” in the same month.

S & P and Moody’s viewed the notes as part equity for balance sheet purposes when the notes were first issued in 2011 due to the existence of a 2071 maturity date. The loss of this equity credit will mean the ratings agencies will view the notes as pure debt, which would increase the company’s gearing ratios if the notes are not been redeemed.

Related Articles

Origin clarifies its debt position

Origin Notes at 7.91% a “buying opportunity”

Origin Notes energised after capital raising

Origin Energy to redeem hybrids at ‘first call’

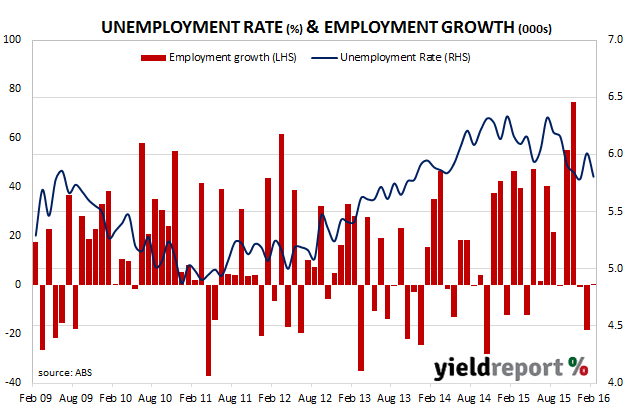

Jobs data muddies water for RBA

17 March 2016

Australia created 300 jobs (net) in February, continuing a poor run of jobs growth in the past 3 months and delivering mixed news for the RBA on interest rates. The good news is there were 15,900 full time jobs created and the headline unemployment rate dropped from 6.0% to 5.8%. However 15,600 part time jobs were shed and a closer look at the numbers suggest the drop in unemployment was a result of around 27,000 people stopped looking for work. The participation rate moved from 65.1% to 64.9%.

The numbers caused 10 year bond yields to drop by around 8bps -10bps and prices in the future cash rate market moved to imply a greater level of confidence in the likelihood of rate cuts in 2016. The chance of a rate cut by November this year is now priced as a certainty.

Adding to the cloudy employment numbers was the seasonally adjusted monthly hours worked in all jobs which fell 0.1% to 1,652.6m hours, which is +2.0% over the last 12 months.

Here’s what the economists thought:

ANZ economist Dylan Eades:

“…the decline in the unemployment rate to 5.8% suggests that underlying conditions in the labour market remain relatively healthy and will be sufficient to keep the RBA on the sidelines for the time being…today’s data puts at risk our call for a May rate cut.”

CBA chief economist Michael Blythe:

“Net, net I would say it is a positive number in terms of the economic outlook. It’s still pretty much the case the unemployment rate is trending lower at the moment. That’s a pretty powerful signal about the economy and is certainly a message for the Reserve Bank as well…so no need for further rates assistance.”

JPMorgan economist Tom Kennedy:

“The participation rate has been moving higher for some time so for it to flick lower today is a little bit odd. We aren’t putting too much emphasis on that and we do think we’ll see a recovery in the participation rate going forward.”

RBC Capital Markets strategist Michael Turner:

“We suspect the unemployment rate will be sticky around 6.0% for most the year. We are still in the camp of two rate cuts in the second half of the year, but you’d need unemployment ticking a bit higher than 5.8%.”

US core inflation creeping up

17 March 2016

Market attention in the past 24 hours has been focussed on the March meeting of the FOMC, even amid expectations of no changes to the official rate, and hence little was written about the CPI release scheduled for earlier in the (US) morning. Which is a surprise, as inflation is one of the three policy objectives of the US Fed, the other two being maximum employment and moderate long term interest rates. It is well-known the FOMC’s preferred measure of inflation is the price index for personal consumption expenditures (PCE) but if other measures of inflation are changing it will not be long before such changes show up in the PCE index.

The U.S Bureau of Labor Statistics released February CPI figures and the headline inflation rate came in at -0.2% for the month, a drop from January’s 0.0%, as energy prices fell again. The year-to-date figure fell to +1.0%, down from January’s comparable figure of 1.3% and in line with market expectations. Falling petroleum prices are again responsible for keeping CPI numbers under control and February’s 13% drop once again held headline inflation below zero.

The big surprise to come out of the data release is the strength of core inflation numbers. Core inflation, which strips out the more volatile food and energy components, rose 0.3% for the month and 2.3% over the last 12 months, up from January’s figure of 2.2%. It’s now the ninth month in a row where core inflation has risen and the last time year-on-year core inflation was higher was in September 2008.

The CPI figures sent yields higher until the dovish comments from the latest FOMC meeting provoked a reversal in bonds markets. 3 and 10 years yields fell, finishing at 0.86% and 1.93% respectively, while the 30 year yield rose 1 basis point to finish at 2.73%.

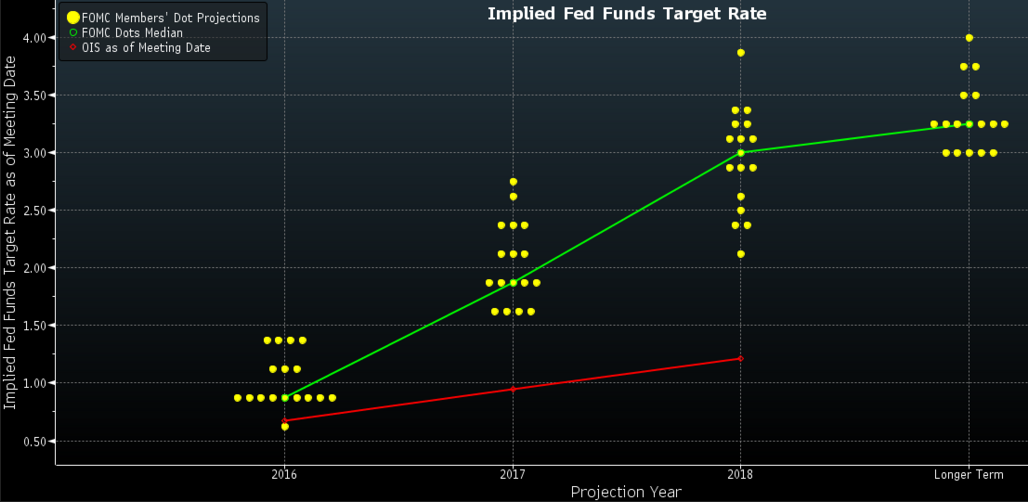

US Fed blinks

17 March 2016

Despite the US Fed talking tough on rates in 2016, at its latest meeting held this week, the FOMC left the federal funds rate target unchanged at 0.25% to 0.50%. No one really expected the US Fed to raise rates at its latest meeting; the odds implied by US cash markets for such a lift were around 5% just prior to the meeting. What has created also created some comment is the lowering of FOMC members’ projections for the path of interest rates in 2016 and 2017, known as the “dot plots” due to the way they are presented as dots on a chart.

Source: Bloomberg

Westpac said the lowering of FOMC members’ projections for the path of interest rates over the next two years “will increase doubts about a June move.” The dot plots now suggest two rates rises this year instead of the four previously expected, while federal funds futures now imply a 50% chance of a July interest rate increase.

Former ANZ chief economist Warren Hogan said the Fed’s latest dot plots “highlight how hard it is going to be to get global interest rates up” and he expects the US rate to remain below 1% in 2016. However, four 25bps increases are still currently expected by FOMC member in 2017.

Baillieu Holst said the FOMC did not want to risk a stronger US currency given the European and Japanese central banks’ fondness for negative interest rates that is driving their respective currencies lower. The broking firm views the FOMC decision as fallout from what has become known as the global currency wars and the desire of countries to have lower exchange rates in order to stimulate exports. The problem is countries can’t all have low exchange rates at the same time; a weakening one country’s exchange means a strengthening of another’s.

February CPI figures were released earlier in the day had sent yields higher until the dovish tone emanating from this latest meeting subdued or reversed the movements. 3 and 10 years yields fell to close the day at 0.86% and 1.93% respectively while the 30 year yield rose 1 basis point to finish at 2.73%.

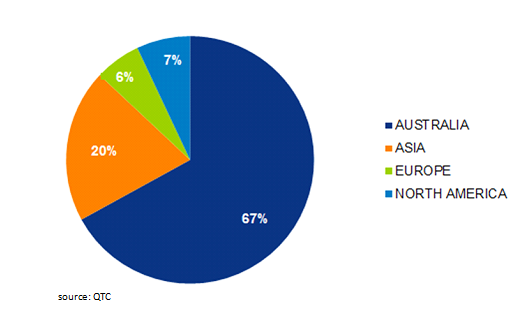

QTC’s last bond sale for 2015/16

16 March 2016

QTC has announced it has tapped its July 2026 benchmark issue in a syndicated issue to the tune of $750 million. The initial indicated range was at EFP + 57.5-61.5bps but after over $1 billion of bids came in the guidance was dropped to EFP + 57.5-60.5bps. The final pricing was at EFP + 58.5bps, which gave a yield to maturity of 3.21%.

Just under 38% of the funds were allocated to fund managers (including hedge funds), 50% to banks and trading desks and 12% to central banks and SSAs (supranational, sub-sovereign and agency). QTC stated it had now completed its 2015-16 term debt borrowing program.

INVESTORS BY REGION

Transurban knocks back funds

16 March 2016

Last week Transurban was on a roadshow through Europe plugging a mooted 8 year FRN issue. It is now understood the plug has been pulled on the planned issue, even though the company was reported to have received enough bids to raise the funds in question. Volatile market conditions are believed to be behind the decision which leads to the likely conclusion that Transurban decided not to accept the terms required by the bidders.

The first two months of 2016 have been good to both bond holders and bond sellers. Bond holders have seen the value of their bonds rise as yields have fallen. Bond issuers have been able to use the low yields to issue debt at multi-decade low interest rates. However, the catch in both cases is the assumption the debt is issued by a sovereign debt or it is well above junk (or as it is more politely known nowadays, high yield) status.

In Transurban’s case it has a group level credit rating BBB+ while its subsidiary Transurban Queensland, which often issues debt, is one rating lower at BBB. So its credit rating is quite respectable, has investment grade status and is two or three notches above high yield. Nevertheless, while benchmark yields are low, it seems as if the spread Transurban was asked to pay proved to be unacceptably high.

Click for more news