25 February 2016

The International Monetary Fund has today called on the G20 group of nations to take “bold actions” to generate growth as the global economy is now “highly vulnerable to adverse shocks”. The warning comes at a time when there is increasing market talk that the limits of monetary policy are being reached and that ultra-loose policies are not stimulating aggregate demand.

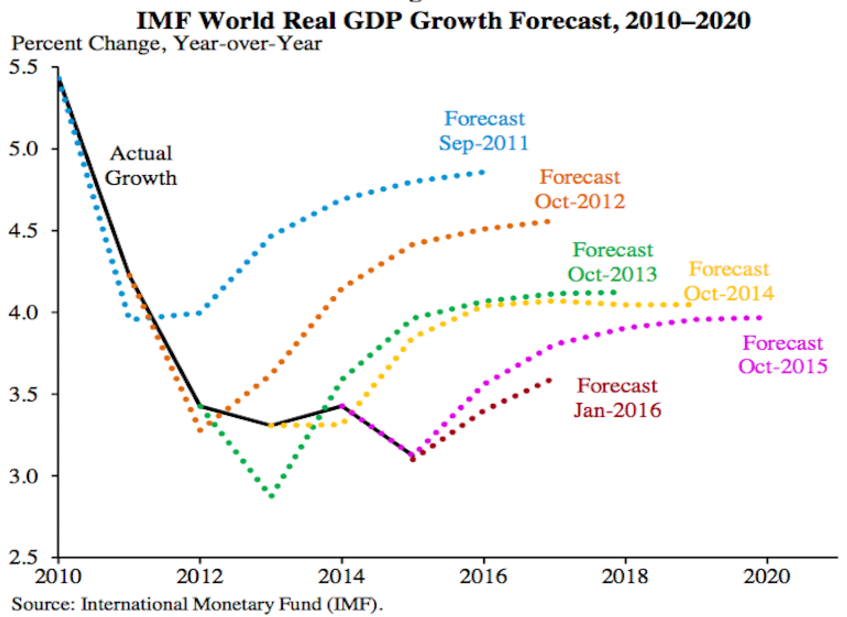

The IMF itself has been a less-than-impressive forecaster of growth rates with the chart below showing just how over-optimistic it continually is.

25 February 2016

Moody’s Investor Service has lowered its credit rating on senior unsecured bonds, in all of Rio Tonto’s group entities, to Baa1 from A3. The outlook is negative.

The view from Moody’s is that there has been a fundamental downward shift in the mining sector with the downturn being deeper and prospects for a recovery extended, resulting in increased credit risk and weaker metrics for Rio Tinto as well as the global mining sector. Supply imbalances in the mining sector, particularly in iron ore, the major earnings and cash flow driver for Rio Tinto, will maintain pressure on prices for several years.

25 February 2016

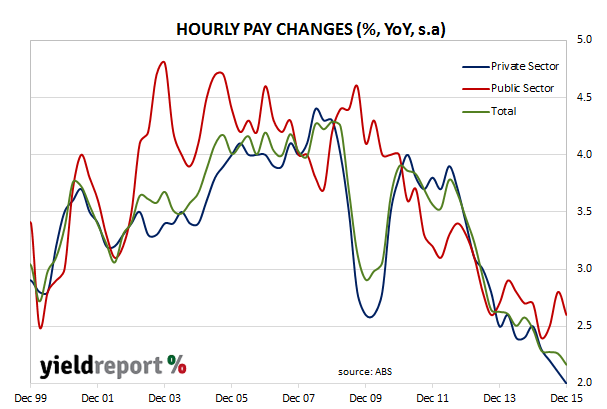

Private sector wages growth continued to hit new lows since the data series began in September 1997, totalling offsetting a higher rate of growth in the public sector. Seasonally adjusted private sector wages growth for the year to the December quarter 2015 was 2.0%, while the comparable public sector rise was 2.6%. Total wages grew by 2.2% for the 12 months to December, which is also the lowest on record and slightly less than expectations of 0.6% for the quarter and 2.3% for the year.

The Finance/Insurance segment had the highest rate of annual increase while the Administrative/Support segment had the lowest. The largest quarterly rise of 0.7% was recorded by South Australia while Tasmania recorded the smallest quarterly rise of 0.1%.

ANZ’s Justin Fabo said lower wage growth may be behind last year’s unexpected employment growth but he expects “modest improvement in wages and household income growth, and hence consumption growth, over the year ahead.”

24 February 2016

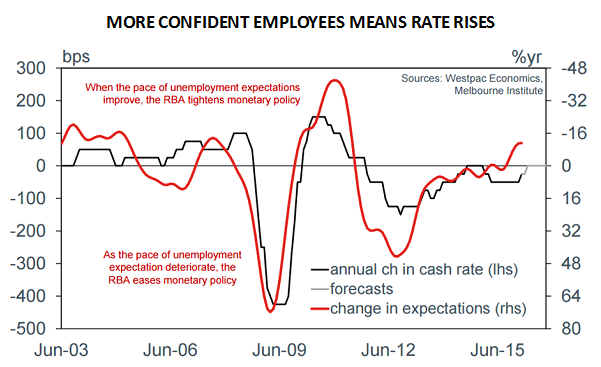

Every so often one comes across a chart where you look at it and the implications seem obvious. Westpac recently published its Westpac Melbourne Institute Consumer Sentiment Unemployment expectations chart pack for February and YieldReport and overlaid it against a chart of the RBA cash rate.

One part of the Westpac-MI survey relates to unemployment expectations (see below chart, red line). As people in the survey thinks their chances of being unemployed fall (the red line becomes more negative; the axis is inverted) and they are more confident of keeping their jobs, the RBA is more likely to raise the official rate (see below chart, black line). The valuable aspect of this sort of chart is the unemployment expectations line (as opposed to the actual unemployment rate) would appear to be a leading indicator of the RBA’s actions.

Currently, opinion among economists at the major banks and other financial institutions is divided when it comes to the next RBA move but many are expecting the RBA’s to cut rates. Cash markets are pricing 2016 and 2017 interest rate contracts with at least one rate cut built in. Even Westpac, the co-owner of the consumer sentiment survey, thinks the official rate will stay steady all through 2016 and into 2017.

Despite markets pricing in one rate cut as a certainty and even a small chance of a second rate cut, the unemployment expectations survey would seem to indicate the next move from the RBA is likely to be an increase in the cash rate.

24 February 2016

Volkswagen has been in the press for all the wrong reasons since September when their emissions testing software was first exposed as cheating the results. The company is paying the price with respect to the issue terms of VW bonds around the world as issue yields for VW bond and asset-backed securities (ABS) have risen. However, VW still continues to sell cars and still continues to provide finance to some of the purchasers.

Given the recent financial market turmoil, Volkswagen Financial Services decision to meet with ABS investors has surprised some observers. The meetings are a prelude to the issue of securities, in this case backed by VW car loans, and the term sheet indicates the Class A component is worth $436 million while the Class B component is worth $27 million. Recent ABS issues by VW in offshore markets have cost the company around 50bps more than in the months prior to the scandal breaking and so it would be likely that the same will happen here. VWFS’s last ABS transaction in Australia was in February 2015 and the Class A and Class B securities were issued at 1m BBSW + 75bps and 1m BBSW + 135bps.

24 February 2016

Despite financial markets recent preoccupation with commodity prices and China, US consumer inflation figures are still possibly the single most important piece of data for US bond markets.

The U.S Bureau of Labor Statistics has now released January CPI figures and the headline inflation rate came in at 0.00% for the month, the same as December’s figure and higher than the market’s estimate of -0.10%. Energy and food prices registered price falls and it appears these are the parts of consumer spending which are keeping the CPI at or near zero. All other categories experienced price increases over the month.

The year-to-date CPI figure rose +1.4% for the 12 months to January, up from December’s +0.7% and slightly higher than market expectations of +1.3%. Core inflation, which strips out the more volatile food and energy components, rose +0.4% for the month and +2.2% over the last 12 months, up from December’s respective figures of +0.3% and +2.1%. Revisions to past data over the last five years indicate monthly CPI and core CPI readings through 2015 were a little higher than previously-published figures.

US bond yields rose on the day with the yields of 2 year and 10 year bonds rising 5bps and 2bps respectively. In US cash markets, the odds for an increase in the Fed rate at the March meeting are still less than 10% and the odds of any increase in 2016 are less than 50%.

23 February 2016

Toyota Finance Australia is a regular issuer of bonds in the domestic market and the finance arm of the automotive giant was last active in the local market in September of last year. However, this time the Netherlands branch of Toyota Finance has issued worth $99 million worth of Aussie-denominated March 2021s into the euro-bond market. Kangaroo bond issues, as they are known, typically pick up when the company can raise funding more cheaply by issuing in AUD and swapping the funds back into euros. Currency and interest rate markets sometimes produce pricing anomalies which are quickly exploited by banks and other participants, resulting in transactions such as this euro-bond issue.

22 February 2016

Svenska Handelsbanken has returned to the Australian bond market after an absence of nearly two years and the bank has just announced a two-tranche fixed and floating bond issue, which is in keeping with their past practice. It is their first issue in the Kangaroo market since April 2014 when they issued $450 million fixed and $200 million floating April 2019s at Swap/BBSW + 95bps. This time the floating component is made up of $500 million at BBSW + 150bps and the fixed component worth $150 million was done at Swap + 150bps, so the pricing has deteriorated substantially from two years ago. Svenska is a Stockholm-based commercial bank rated AA- by Standard & Poor’s, Aa2 by Moody’s and AA- by Fitch.

19 February 2016

It’s not just energy producers such as Origin, Santos and Woodside being on wrong end of credit downgrades from ratings agencies as oil prices have fallen back to 2004 levels. Countries, or “sovereigns” as they are known in financial markets, are experiencing it as well. Standard & Poor’s announced a two-notch downgrade to Saudi Arabia’s credit rating, from A+ to A-. Neighbouring oil and gas producers Oman and Bahrain also received downgrades. Oman now has a BBB- credit rating, which is still investment grade but only one notch above “junk” status while Bahrain’s credit rating is B, which is well into sub-investment grade territory.

18 February 2016

The central bank of Mexico last night raised interest rates by 50bps to 3.75%. Mexico’s last rate rise was in December 2015 when it raised the official rate by 25bps following the US Fed’s rate raise. The move surprised markets and saw the peso rally sharply. The Mexican currency had recently tested lows against the USD but the bank is concerned about inflation rising and was keen to nip any moves in the bud.

The Mexican economy relies heavily on the state-owned oil company Pemex whose taxes fund about 20% of the Mexican Government budget. Oil revenues had plummeted recently causing a collapse in the peso and subsequently a potential rise in inflation.