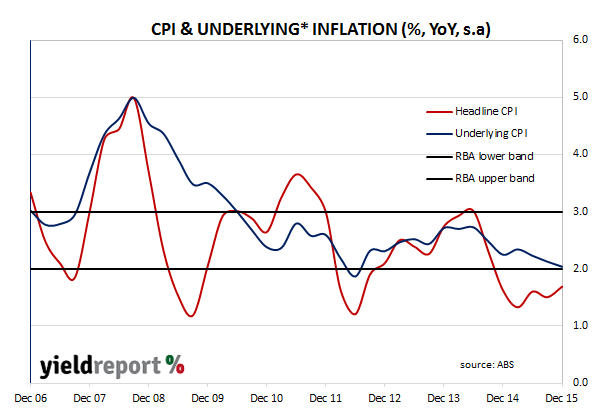

The December quarter CPI was released this week showing a headline quarterly rate of inflation of +0.4% (seasonally adjusted) or 1.7% for the year to the end of December. This surprised markets which were expecting 0.3% for the headline rate and an annual inflation of 1.6 per cent.

The “core” or underlying rate, the RBA’s preferred measure of inflation that strips out volatile food and energy prices, recorded an average 0.5% for the quarter (0.5% expected) and 2.0% over the year (2.1% expected).

The underlying inflation rate of 2.0% is at the very bottom of the RBA’s target range of 2.0% to 3.0%, as shown in the chart below, reinforcing the RBA’s easing bias but not being seen as the smoking gun required to immediately cut rates.

*average of trimmed mean & weighted median CPI measures

Economists agreed the RBA was unlikely to change their rate setting in the short term and the cash markets reacted by dialling back expectations of rate cuts this year, although pricing still indicates an official rate reduction by August is still a very high probability. Pricing for a RBA rate cut in February fell from 19% to 6% and for a May cut the odds fell from 82% to 62%. Bond markets were largely unaffected but yields in the futures markets for 90 day banks bills rose sharply, rising between 5bps and 7bps for 2016 contracts, while the Aussie dollar jumped against the greenback.

Here’s what the economists thought:

Michael Workman, CBA

Inflation is not dead. It is just resting. Today’s 0.4% rise in the headline inflation rate was slightly above market, and our, expectations of 0.3%. The underlying measures averaged out at 0.5% which was in line with expectations. The annual inflation rates of 1.7% for headline and 2.0% for the underlying measures show that inflation is well under control. The RBA’s first 2016 meeting is next Tuesday. We believe the low inflation outcomes will give them room to maintain their conditional easing bias. But they are unlikely to act on it unless there are signs of deterioration in the jobs market. And the improvement in the jobs data is remarkable. There have been an extraordinary 300k extra jobs added over the past year and the unemployment rate is at 5.8%.

Jo Masters, ANZ

The low inflation environment is unlikely to be a catalyst for policy action given our expectation that underlying inflation will move back within the RBA’s 2%-3% band in early 2017. However, it not a constraint on policy action should demand need a boost. We continue to closely watch demand indicators, including the December partials next week.

Tapas Strickland, NAB

The underlying inflation rate for Q4 is exactly in line with the RBA’s November Statement on Monetary policy which was for underlying inflation at 2.0% year-on year. NAB’s view remains that the RBA will continue to hold interest rates at current levels on continuing signs that the domestic economy is performing somewhat better in recent months – evidenced by above average business conditions and solid employment growth.

Paul Bloxham, HSBC Australia

Importantly, for the moment, the RBA can afford to tolerate low inflation because the jobs and activity indicators have been lifting. The unemployment rate fell to a two-year low of 5.8% in December and a key survey also shows that business conditions have been around 7-year highs recently (albeit falling back a little in the December print). While the labour market and activity surveys are still holding up, the RBA is unlikely to cut rates. This pretty much rules out a cut next week.

Scott Haslem, UBS

Today’s CPI was broadly in line with market & RBA expectations, with the headline of 1.7% continuing to drift up toward the bottom of the target, while core measures…have converged on a 2% pace. Pleasingly, the areas we’ve been highlighting as possibly flagging an era of lower inflation due to more competition in telecoms & food, rents & slowing administered prices (health & utilities), continue to moderate. While today’s CPI is no impediment to a rate cut, nor is it a smoking gun compelling the RBA to cut, given the economy’s ongoing moderate growth.

Shane Oliver, AMP Capital

As December quarter inflation was in line with RBA forecasts it is probably not low enough to bring on another rate cut from the RBA on its own. But with inflation running at the bottom of the 2-3% inflation target it leaves plenty of room for another rate cut and helps reinforce the RBA’s easing bias. While the RBA may not be ready to cut the cash rate again next week our assessment remains that the ongoing downside risks to growth, further falls in commodity prices and global growth uncertainties along with low inflation will see the RBA cut rates again at some point in the next few months. Market pricing continues to allow for at least one more rate cut over the year ahead.

Chris Caton, BT Financial Group

We continue to think that the cash rate is on hold for several months yet, and that the next move is just as likely to be up as to be down. The RBA will hold its first monetary policy meeting for 2016 on February 2. Cash rate futures put the probability of a 25bps interest rate cut at just 6%, down from 21% before the CPI report was released. Despite the diminished expectations for a near-term interest rate cut, markets are still fully priced for a reduction in the cash rate to 1.75% by September this year.

The breakdown of figures are as follows:

December quarter CPI: +0.4% (headline figure)

September quarter CPI: +0.2%

CPI to December year end: +1.7%

Underlying December quarter CPI: +0.5% Avg

Underlying September quarter CPI: +0.5% Avg

Underlying CPI to December year end: +2.0%

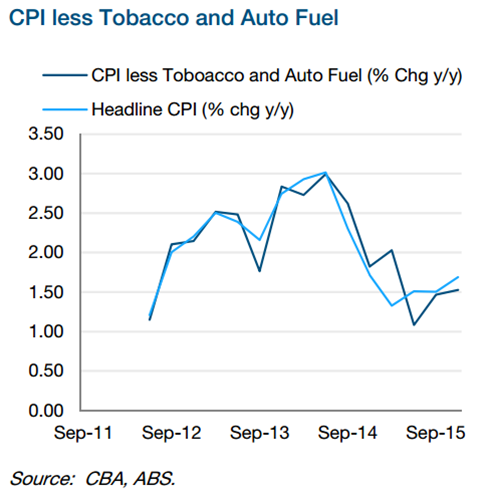

Analysis of the CPI by CBA showed that the impact of petrol prices is less that most people’s assumptions and that the greatest impact on the CPI was, in fact, tobacco prices. For the quarter petrol subtracted 0.18% from the CPI while tobacco added 0.26%. This is interesting for several reasons: the CPI is low but would be lower if not for tobacco; tobacco tax is large and controlled by the federal government. A chart of the CPI excluding tobacco and petrol is included below.