19 January 2016

Bond issues by unrated corporates are not particularly common in Australia. FIIG Securities is doing its best to change this and has rolled out another unrated bond issue, this time for Impact Homes. The new issue is for $40 million of 5 year bonds paying an 850bps coupon. An additional $5 million worth of oversubscriptions will be accepted.

Borrowers seeking to diversify their funding away from the major banks can seek to tap the corporate bond market but it’s a more difficult prospect for companies that doesn’t carry a rating from a credit rating agency or operate under a continuous disclosure regime as would be the case for an ASX listed company.

In the case of the FIIG issues, FIIG issues its own credit assessment and regularly updates investors on the company’s financial position.

Before the Impact Homes deal was announced the previous FIIG issue was from Sunland Group in early November. Sunland, an ASX listed company, raised $40 million by way of a 5 year bond, although those bonds carried a 755bps coupon rather than the 850bps on the Impact Homes bonds.

15 January 2016

Mark Carney, the Band of England chief, had previously said the decision to raise rates “will likely come into sharper relief around the turn of this year”. We are now in the first quarter of 2016 but the BoE kept rates steady at its latest meeting with an 8 to 1 vote in favour of no change. Given the turmoil in international markets in recent weeks, the decision is not a surprising one. A recent Reuters poll of economist over the past week expects the central bank to start raising the official rate in the third quarter of 2016, later than the previous poll which saw a rate hike in the second quarter.

UK 10 year bond yields were slightly lower, dropping nearly 1.5bps to 1.73%, amid higher US and German comparable bond yields, perhaps as the market digested the Bank’s statement of a lower trajectory for rising rates than in the past. “All members agreed that, given the likely persistence of the headwinds weighing on the economy, when Bank rate does being to rise, it is expected to do so only gradually and to a level lower than in recent cycles.” The currency markets took a contrary view, pushing sterling higher against the US dollar and the euro after the Bank’s announcement but even so, the pound is trading near a 5 1/2-year low against the dollar and has been weakening against the euro since July.

Local reaction focussed on the tone of minutes from the meeting. Westpac said, “The BoE did not appear unduly concerned by recent price falls, rather noting the strong labour market. Rate hikes this year remain on the cards.” ANZ said the BoE had “acknowledged the net mild positive impact of low oil prices on the economy (despite weighing on inflation).”

14 January 2016

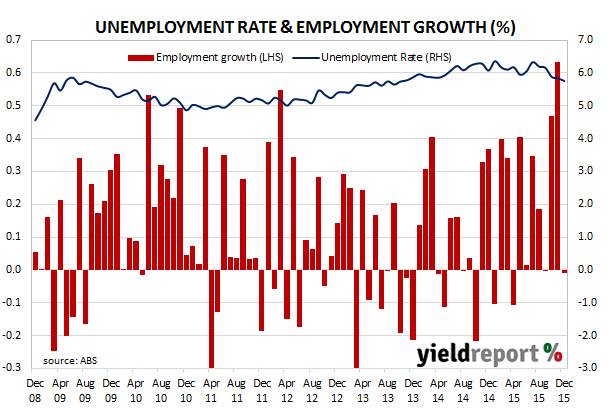

After a “jumbo” October employment result and an even bigger jump in November – both of which were met with slight scepticism in the market – analysts were generally expecting some sort of statistical reversal for the December employment figures. ANZ said prior to the release “we are due a softer print and expect employment to have remained broadly unchanged in the month” while Westpac said, “Actual jobs are running ahead of our indicators…However, December is normally a strong month in original terms so this leaves a level of caution.”

The ABS has now released the December Labour Force figures and they came in at a seasonally adjusted -1000, again higher than the market expectation of a 10k fall. The local bond market was largely unaffected by the numbers as spot 10 year bond yields rose a point immediately after the data release before reverting back while the story in the currency markets was a similar one. Cash rate markets increased the odds of a rate cut by June 2016 from 68% to 78%.

The labour force figures from late last year attracted a degree of scepticism from respected economists who questioned the sampling process. This latest result has also been questioned. AMP Capital’s chief economist Shane Oliver said the result was “unbelievably strong” given Australia’s 2.5% GDP growth rate although he conceded, perhaps jokingly, the growth in jobs may be from “low cost cafe jobs, perhaps”.

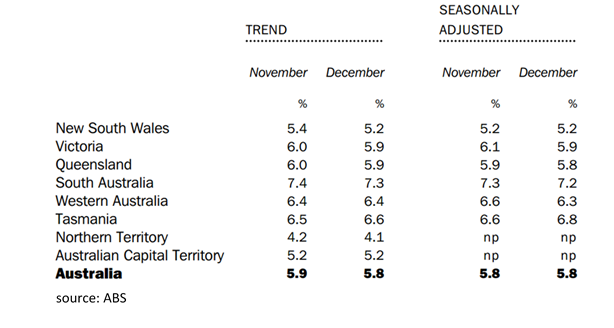

The unemployment rate remained steady at 5.8%, driven by a fall in the participation rate from 65.3% to 65.1% and a fall of 10.9k in the total number of unemployed people. While total employment fell, full time employment rose 17.6k while part time employment fell 18.5k. Total employment increased by 2.7% in the year to December while seasonally adjusted monthly hours worked in all jobs was effectively steady at 1645.2m hours and up 3.4% for the year.

Westpac’s Justin Smirk said, “While the December survey was a less upbeat update than we have seen in recent months, it is still a positive outcome and one that would give comfort to the RBA as they return from their summer recess…the improvement in the labour market has been the greatest in NSW where the unemployment rate has dipped to a national low of 5.2% and the state’s pace of employment growth is a very robust 4.4% which is consistent with a rebalancing of growth away from resources and towards services.”

12 January 2016

The credit team at RBS has gone out on a limb and advised clients to “sell everything”. In a note to clients it advised only to keep high quality bonds. “This is about return of capital, not return on capital. In a crowded hall, exit doors are small.” RBS said global trade and total private sector credit are contracting and global debt ratios have reached record highs. It believes equities and corporate debt “have become very dangerous” and conditions are reminiscent of 2008.

RBS forecasts German 10 year bond yields will fall in time to an all-time low of 0.16% and may even go negative. The ECB official rate will fall to -0.7% and US Treasury bonds will fall to exceptionally low levels. The investment bank also says the tightening cycle by the Fed and the Bank of England is already over and the next action by the Fed will be a rate cut, despite the Fed raising its official rate only recently.

18 December 2015

Korea National Oil Corporation (KNOC) has announced it will be holding a series of meetings with investors in Australia in January. Such meetings are usually a prelude to a bond issue in which the issuer gauges the level of demand by investors and gains an estimate of the likely pricing. The last issue of bonds by KNOC into the Kangaroo market was in September 2014 when it sold $350 million worth of fixed and floating August 2019 bonds at Swap/BBSW + 108bps. KNOC is rated AA- by Standard and Poor’s and Aa3 by Moody’s.

17 December 2015

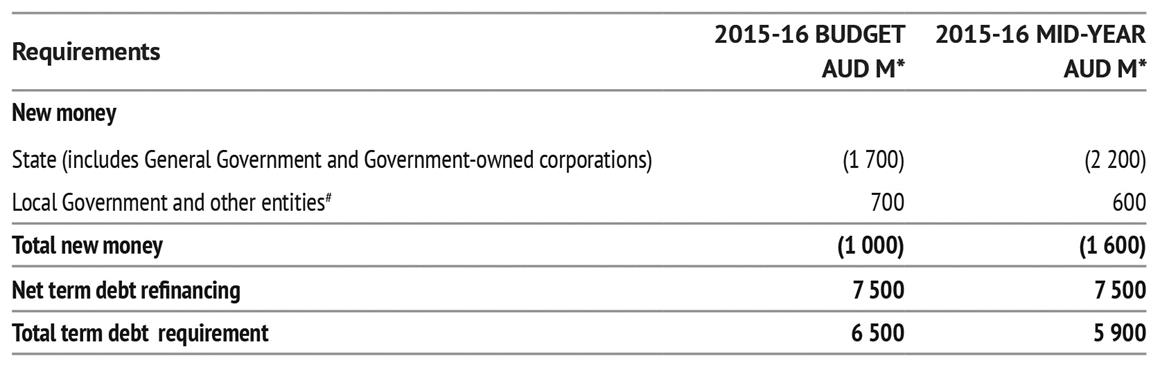

Following the release of the Queensland Mid-Year Fiscal and Economic Review (MYFER), the Queensland Government has published its amended funding programme for the year to June 2016. It was previously expecting to require $6.5 billion to cover maturing bonds and government spending but the figure has been revised down to $5.9 billion on the back of a reduction in expected government borrowing, even though the budget deficit will be higher than previously expected. State government bodies will seek $500 million less than previously expected and local government and “other entities” will require $100 million less. Queensland Treasury Corporation said it will continue to issue benchmark bonds to maintain liquidity in existing debt series but it will also seek to issue non-benchmark securities, including floating rate notes, to smooth its maturity profile over time.

*Numbers are rounded to the nearest AUD100 million. source: QTC

# Retail water entities, universities, grammar schools and water boards.

Click here for the full Mid-Year Fiscal and Economic Review document.

17 December 2015

Oil and gas prices will stay down for longer than anticipated, according to Moody’s latest price assumptions, and this has resulted in the outlook for Woodside being changed from “stable” to “negative”. While Woodside’s senior unsecured credit rating remains at Baa1, the ratings agency thinks Woodside’s financial ratios are “weak” in relation to its credit rating but it is willing to leave the rating intact on the basis it sees an improvement in the prices of Woodside products in 2017. “Woodside’s negative outlook reflects Moody’s expectation that earnings and credit metrics in 2015 will be weaker than previously expected, and will take longer to rebalance to more appropriate levels for the rating under our revised base case assumptions.”

16 December 2015

Shortly before Christmas 2015 the Australian Office of Financial management released an updated economic and budget forecast providing updated details on planned issuance of Australian Government bonds for the period to June 30.

ACGB issuance in total for 2015-16 is expected to be around $86 billion in face value terms. Issuance to date this financial year has totalled $43 billion. After accounting for maturities and repurchases of $33 billion this represents net issuance of $53 billion.

A new ACGB maturing on 21 November 2027 is planned to be issued by syndication in January or February 2016. This will provide another issuance point around the 10-year part of the yield curve.

As previously announced, the AOFM plans to issue new Treasury bonds maturing in late 2021, and 2028. The 2028 bond will be issued sometime in calendar 2016 but not prior to the release of the 2016-17 Budget.

Issuance of Treasury index-linked bonds in 2015-16 is expected to be around $4.5 billion in face value terms. Issuance to date this financial year has totalled $2.6 billion.

16 December 2015

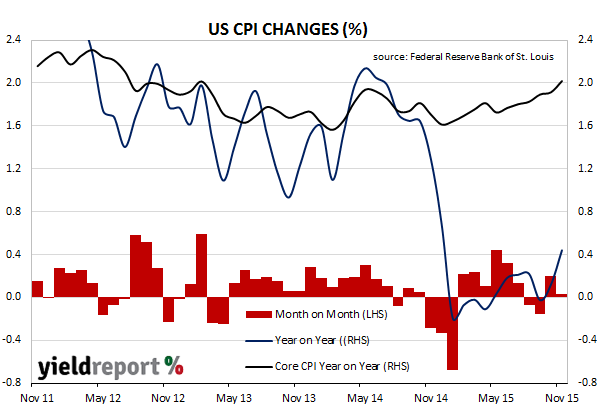

The U.S Bureau of Labor Statistics released November CPI figures which were largely in line with market expectations. The headline inflation rate came in at 0.0% for the month, a drop from October’s +0.2%, as rents, airfares, new car and medical prices rose while petroleum prices fell. The year-to-date figure was +0.4%, up from October’s comparable figure of 0.1% and in line with market expectations. Core inflation, which strips out the more volatile food and energy components, rose 2.0% over the last 12 months, up from October’s figure of 1.9%.

US bond yields went higher on the news; the yield on 2 year bonds rose 5bps to 0.98% and 10 year bond yields rose 9bps to finish the day at 2.29%. In the cash markets, the odds for an increase in the Fed rate rose slightly to around 80% as the latest inflation figures were seen as additional ammunition for the Fed to raise rates for the first time since 2006.

11 December 2015

ASX listed MyState Bank, formerly MyState Financial, has announced Standard & Poor’s has affirmed the bank’s BBB rating and upgraded its outlook from stable to positive. Standard & Poor’s view of MyState’s improved asset quality was behind the improved outlook.

MyState Managing Director Melos Sulicich said, “Credit quality remains the cornerstone of our business as we continue to diversify our asset base.” The bank was pleased by the rating agency’s change and it would continue to “prudently” increase its loan book.

MyState has two banking brands; the Tasmanian-based MyState Bank and the Rockhampton-based The Rock. Its last foray into domestic bond markets was in August when it issued Tier 2 Basel 3 compliant subordinated bonds.