03 December 2015

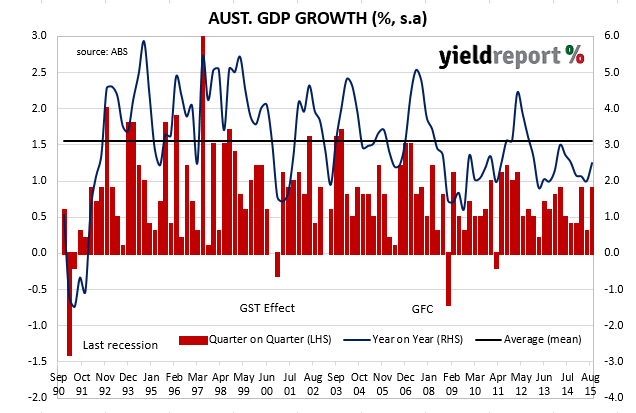

Australian GDP figures for the third quarter came in just above expectations, growing by 0.9% and 2.5% year on year (both figures seasonally adjusted). Financial markets had been expecting 0.7% for the quarter and 2.4% for the year after taking into account recent data.

The second quarter’s sharp drop in export income was reversed as volumes picked up and even as prices for Australia’s commodity exports remain weak. Recently released trade figures days had indicated this and market expectations were adjusted in the lead up to the publishing of the GDP figures.

The bond markets reacted to the data release by marking 10 year bond yields down 4bps to 2.83% while the currency market initially sent the local currency higher before it tapered off over the rest of the day.

A snapshot of views from some well-known economists gives an insight into what this means for economic growth and interest rates:

NAB senior economist David de Garis

The result is within the range of expectations. The economy is growing back towards trend growth. It is growing at a slightly less than potential rate, but it is enough to create sufficient jobs to keep the unemployment rate steady. This must be in line with the RBA’s expectations and I don’t see how this could alter their forecast materially at all. Steady as she goes.

CBA senior economist Michael Workman

We see it as a pretty good result for the quarter, and also through the year. The big issue is still around this dramatic decline in mining investment and how it tends to distort the overall data. Household spending was up, net exports recovered very strongly. 2.5% growth in real terms is good.

UBS economist Scott Haslem

The domestic economy overall remains relatively weak, but is being depressed by a capex cliff (which appears likely to remain a large drag ahead); yet despite this, the moderately positive trends in consumption and housing remain intact. Nonetheless, amid a collapsing terms of trade, economy-wide ‘inflation’ & ‘real income’ are still falling. That said, looking forward, with RBA Governor Stevens saying Q3 GDP was “not a bad outcome” and “just a little below trend”, we continue to expect the RBA to hold rates in 2016

CommSec economist Savanth Sebastian

There is no question that the recovery across the national economy is patchy, but given the array of stimulatory factors, the latest result highlights that the economic landscape looks in far better shape than even a year ago. If there was any disappointment in the latest result it was that, as expected, business investment remains a drag on growth. Corporate Australia continues to hold back from significant investment and as such the growth outcomes over the next year will be patchy.

RBC Capital Markets senior economist Su-Lin Ong

It’s not a bad headline number but that was probably always likely. The composition of growth probably is still a bit disappointing with only modest signs of transition. The details are still consistent with the RBA’s easing bias and that sort of persistent sub-par activity suggests there is still a risk of easing next year. We have a rate cut pencilled in for the first quarter.

HSBC chief economist Paul Bloxham

Growth is clearly rebalancing in response to low interest rates and a lower AUD. Nonetheless, with growth now having been below trend for three years and commodity prices continuing to fall, inflation remains low. Although growth is lifting, the key question for the RBA is whether there is enough growth to keep inflation on target? A lower AUD would help. Otherwise, and despite the RBA’s considerable reluctance, another rate cut may be needed.