09 October 2015

Suncorp-Metway announced it has mandated several banks to arrange meetings with debt investors during early-to-mid October. Suncorp’s last foray into the domestic debt markets was in late August when it issued fixed and floating covered bonds but the bank’s previous uncovered bond issue was in the week prior when it issued $200m worth of 1.5y FRNs at BBSW + 52bps.

09 October 2015

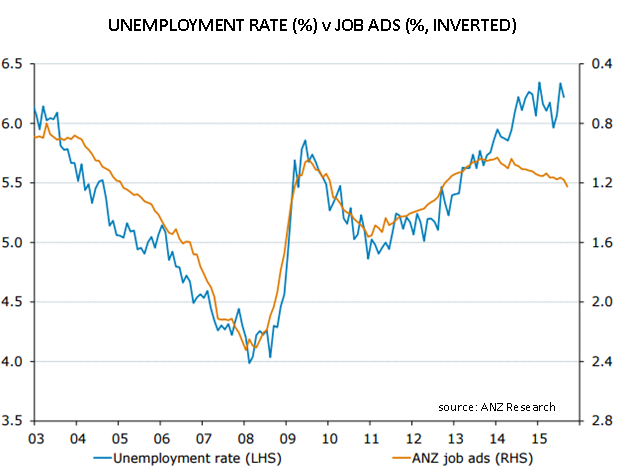

ANZ’s monthly job ads survey was released showing ads were up 3.9% (seasonally adjusted) compared to August and up 12.8% from September, 2014. The comparable August figures were +1.0% and +8.7% respectively. Internet ads were up 4.0% for the month while newspaper ads were down 2.7%. Compared to a year ago internet ads were up 13.7% while newspaper ads were down 19.6%.

ANZ’s chief economist Warren Hogan said, “The positive trend in job advertising is a sign that the economy is so far adjusting relatively well to significant headwinds from falling commodity prices and mining investment.” However, he expects “the significant support to growth from the factors above will wane heading into 2016.”

Westpac welcomed the “small positive revision to August” but said the trend “is much softer than past recoveries”. It also added newspaper ads “are virtually redundant.”

09 October 2015

Last month BHP announced its intention to issue multi-currency hybrid capital securities after holding a series of investor briefings. The design of the hybrids would allow them to be classified as part equity, thus keeping BHP’s balance sheet in shape and maintaining its A+ credit rating. Earlier in the year ratings agencies had put BHP’s and Rio’s debt on a “credit outlook negative” watch and now Commonwealth Bank thinks that outlook will be converted into an actual downgrade. In a brief mention regarding BHP’s upcoming subordinated debt notes, the bank said its “base case” scenario is for BHP to be downgraded to A in the 2016 financial year.

09 October 2015

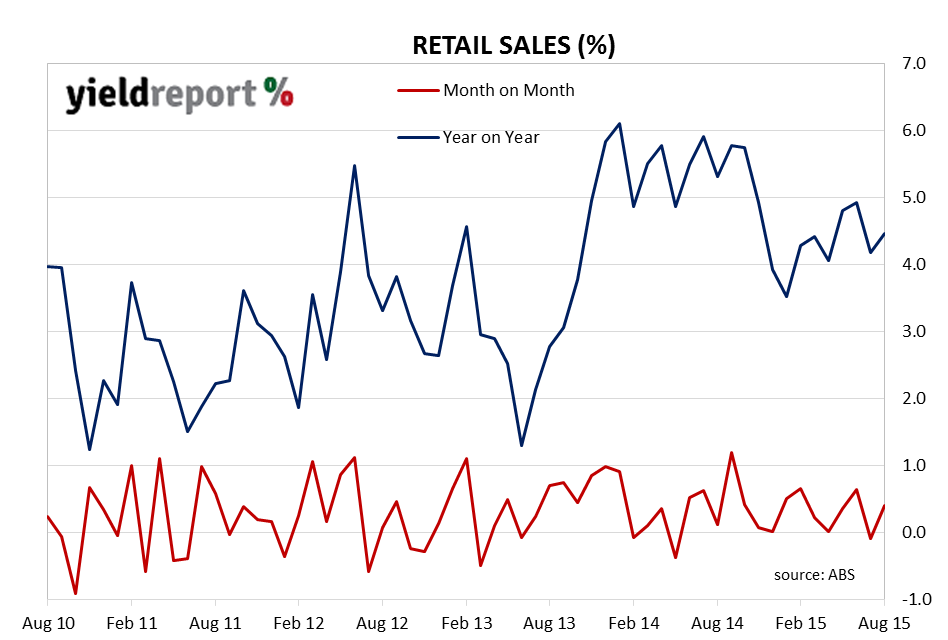

Last month AMP’s Shane Oliver had said he expected a bounce in retail sales and this month his prediction proved to be correct. August retail sales increased by 0.4%, in line with market expectations and a reversal of the previously recorded figure of -0.1%. On a year-on-year basis, sales were up 4.5%, slightly up on July’s annual figure of 4.2%. UBS expects retail sales to grow at around 4%-5% and within that sees the pick-up in department store sales to 7.0%. It also sees a paring back of growth figures in the ‘dining out’ and household goods categories as ‘worthy of note’. Perhaps this is what Macquarie is referring to when it said, “The retail sector is in need of further stimulus to drive a broad based improvement in sales growth beyond selected categories.” Westpac said the real disappointment was around the household goods segment which rose just 0.2% as “this discretionary category is a key cyclical driver.”

08 October 2015

Pepper Australia announced it has mandated several banks to arrange meetings in Sydney with potential investors during mid-October. The aim is to explore funding options “across a range of markets.” Pepper was last in the debt market in late July when it placed the Class AR-U bonds of Pepper Prime 2013-1 RMBS at BBSW+100bps.

06 October 2015

Once again the RBA’s decision to maintain the official cash rate at 2.00% came as no great surprise to the markets, with banks such as Westpac saying prior the meeting there was “little chance” of a cut and cash markets had priced in a slim 6% chance of such a reduction. The statement from the meeting pointed to the domestic economy expanding moderately, offshore weakness, a strong US economy, but with some small changes from the September monthly statement. The deletion of the words “most of” in reference to the economy and the inclusion of Melbourne with Sydney as cities where house prices are rising strongly was seen by Commonwealth Bank as “marginally hawkish” but as Westpac’s Bill Evans noted, the statement had the “fewest number of changes to the previous month’s statement that we have ever seen.”

In spite of this, the market remains priced for a rate cut in Q1 2016 and a 50:50 chance of a second before August 2016, which Commonwealth Bank said was appropriate while at the same time saying that it can’t see rates reducing before January. Westpac’s view was the RBA statement would have been disappointing to “doves” and noted the small rise in 3y and 10y bond yields on the day.

ANZ said the RBA is “in wait-and-see mode” and a loss of momentum in the residential construction and the services trade sector will lead to a rise in unemployment and thus provide the impetus for 25bps rate cuts in February and May.

AMP’s Shane Oliver seemed a little less confident of a rate cut after this meeting even though he said the RBA still sees spare capacity in the economy and inflation contained. The statement “suggests only a very mild easing bias at best.”

Westpac’s Bill Evans said he thought the RBA will not change its 2015 and 2016 growth forecasts, which would mean the cash rate remains unchanged. He did, however, suggest “risks on rates remain to the downside particularly around the global outlook; the terms of trade; and the labour market.”

The full RBA statement can be read here.

05 October 2015

Origin Energy has announced a capital raising that should soothe the nerves of its hybrid investors (ASX Code: ORGHA). The company will raise $2.5bn via a heavily discounted equity raising, cut dividends for the next two years, slash spending and sell some assets in order to bolster its balance sheet. Like most energy producers, Origin has been hit by low prices, large debt and high capital expenditure programmes. The company treasurer, Peter Rice confirmed that the company would be exercising its option to redeem its hybrid securities on the ‘first call’ date in December 2016.

The Origin hybrids have been trading at a sharp discount to the face value at around $94 per security. With a first-call date in December 2016 the market was hoping the company would take up the opportunity to redeem them at that date but there has been conjecture they may not – hence the sharp trading discount to the $100 face value.

In essence, the conjecture centred around the different ratings agencies’ views of the securities and whether they were deemed to be equity or debt. You can read our previous article here but as it stood, S&P gave the notes a 50% equity credit. Had Origin announced that they would redeem the notes without having made alternate arrangements to raise other capital, Origin’s debt rating would likely have been downgraded and put pressure on the company to bolster its balance sheet. In the end, Origin has bitten the bullet and it’s the equity holders that will suffer dilution or have to stump up more cash.

Recent hybrid purchasers that risked buying the hybrids at a shade over $94 will see a $6 capital gain on top of the distribution income over the next 12 months. Existing holders will heave a sigh of relief that the securities will be redeemed at $100.

01 October 2015

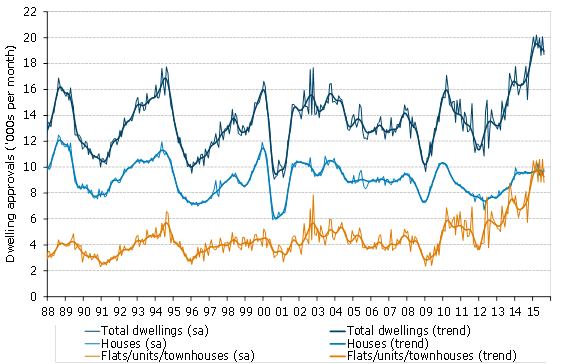

The Australian Bureau of Statistics released August building approval figures which were weaker than expected. Total approvals fell 6.9% compared to the expected figure of -2.0% but the fall comes off a revised July figure of 7.9% (initially recorded as a 4.2% rise). The fall was driven by an 11.4% fall in units which appears to be centred in NSW, where unit approvals dropped by 28.5%, although NSW’s unit approval was still up 24.6% on August last year.

Private house approvals were up 4.9% for the month and 3.0% for the year while units were down 11.4% for the month and up 8.6% for the year. Total approvals were up 5.1% for the year to August.

Westpac said the figures suggest the ‘high rise’ boom is over in Victoria but noted approvals for non-high rise buildings in NSW “are showing a renewed rise.” ANZ said the data was “broadly consistent with our view that the housing market is beginning to soften.” Although the bank noted housing approvals are likely to stay at high levels as long as interest rates stay low it noted further growth “appears remote” and may have been part of the rationale behind the bank’s view the RBA will cut rates next year.

Source: ABS, ANZ Research

01 October 2015

Warren Hogan, ANZ’s chief economist, now expects the RBA to cut rates next year and not just once, but twice. Since the last 25bps cut in May this year, he has maintained the view the RBA has been leaning towards a rate cut but that “lean” is now more a definite expectation. It is worth noting Mr Hogan correctly predicted in January this year the RBA would cut the cash rate twice in the first half of 2015.

The firming of opinion has been put down to the view that Australian economic growth will not be high enough to reduce the spare capacity present in the economy. There are two factors why it won’t be high enough: lack of global growth and a softening Australian non-mining sector.

Global growth and more specifically, growth among Australia’s trading partners such as China and Japan, is slowing and expected to slow further. Volumes of exports are under pressure and the prices paid for those exports, such as coal and iron ore, have come down dramatically. Prices of imports may also be weaker but not to the same degree and thus Australia’s terms of trade will have weakened, effectively reducing Australia’s export income.

The non-mining sector has been supported by construction in the housing market and the fall in the exchange rate. ANZ expects housing construction to pull back from its recent strength while the exchange rate is expected to settle after having fallen substantially through the first three quarters of 2015. The net effect is a non-mining sector which is travelling at trend with “little prospect of improving”, while mining investment is expected to fall further.

Under the above scenario, Mr Hogan says “it is difficult is difficult to see how inroads can be made into an elevated unemployment rate” and his view is that the risk of higher unemployment is therefore greater. Hence the bank’s view of pressure on the RBA to cut rates.

There are two caveats to ANZs reasoning: a massive stimulus package out of China and/or the domestic economy staying stronger for longer. ANZ expects the domestic figures to remain strong this year but it’s not this year featuring in ANZ’s calculations, “it’s next year where we see things softening.”

29 September 2015

US consumers paid little notice to share market turbulence in August to rack up another month of higher consumer spending. The Bureau of Economic Analysis released consumer spending figures showing a 0.4% increase in August, slightly more than the 0.3% expected and up from the July figures which were revised up from 0.2% to 0.3%. Personal income figures were also released and they showed a 0.3% increase for August, down from July’s number of 0.4% but in line with market expectations. A falling unemployment rate, lower oil prices and a slightly lower rate of savings are thought to be behind the latest increase. An estimated two thirds of US GDP comes from personal consumption and the latest figures have led some financial institutions such as Morgan Stanley to raise their US growth estimates.