01 September 2015

The RBA meets on 1 September for its monthly board meeting where it determines the level of interest rates. The announcement from the meeting is out at 2:30pm (AEST) however the market is not expecting a rate cut and fully expects rates to be kept on hold at 2.00%, a historic low.

Surveys by AAP (16 economists) and Reuters (25 economists) show that all economists surveyed expect rates to be unchanged.

28 August 2015

Fresh after the release of a lower profit result for 2015, Woolworths has been handed a credit downgrade on its long term debt by S&P. The downgrade follows S&P’s change to the retailer’s credit outlook from stable to negative in June. The ratings agency said Woolworths’ supermarket earnings and margins were under pressure from intense competition, Big W was delivering a weak operating performance and the Master’s hardware division was producing “significant losses”. S&P credit analyst Paul Draffin said, “These factors, together with the company’s large and growing fixed cost base and capital investment, are likely to sustain the group’s financial risk profile outside tolerances for the previous ‘A-‘ rating in the next two years.” S&P expects new supermarket entrants such as Aldi to gain market share and thus keep Woolworth’s under pressure at the same time as losses from the Masters hardware division to an “increasingly material impact”. Slowing revenue and earnings growth, in combination with rising fixed costs will “pressure the group’s key credit ratios in the next 1-2 years”. In spite of this, S&P continues to view Woolworths’ business risk profile as “strong” and the current A-2 short term debt rating has been affirmed.

27 August 2015

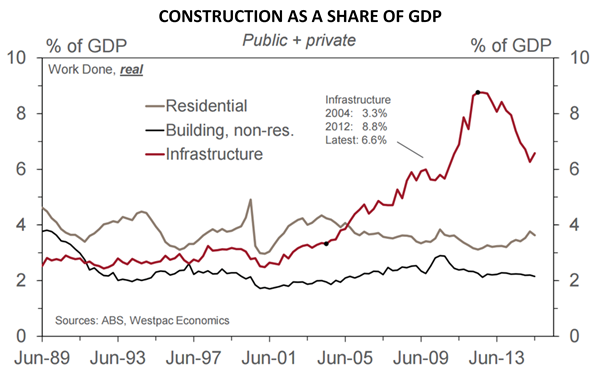

June quarter construction figures showed a rise of 1.6%, up from the March quarter’s fall of 2.0%. The positive result was a surprise to financial markets where the expectation was for 1.5% fall. WA’s mining sector, in particular the construction of the Roy Hill iron ore mine and the Gorgon LNG projects, was responsible for the surprise result. Westpac, however, feels the activity is unsustainable and there is speculation the figures are partly the result of construction at Roy Hill making up for previously lost time. Nationally, the building, residential, non-residential segments were all negative but the 5.6% increase in the engineering segment more than offset these other segments. There was little reaction to the release with attention still focussed on Chinese and US share markets.

27 August 2015

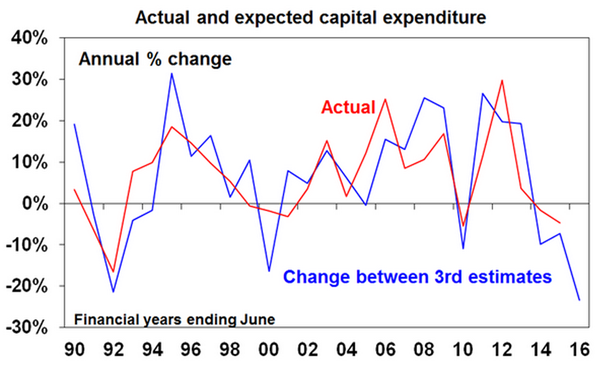

Capital expenditure in the second quarter was weaker than anticipated and declined by 4% compared to the previous quarter. Equipment spending fell by 1.2% and building/structure spending fell by 5.6%. Estimate 3 for 2015/16 capex plans was $114.8bn, 10% higher than May’s Estimate 2 of $104bn but well down on the previous year’s Estimate 3 of $145bn. Given the relationship (see below chart) between the capex plans and actual expenditure, AMP’s chief economist Shane Oliver said the capex plans imply a 38% drop in mining investment in the 2016 financial year and a 7%-8% drop in non-mining investment, resulting in an overall fall of 23%-26%. Westpac said prior to the report they saw capex plans of $113bn as neutral but investment intentions in the services sector will be of more than passing interest to the RBA, which has previously stated it expects the near-term outlook for non-mining investment to be subdued.

26 August 2015

Two senior Federal Reserve officials recently said a September rise in US official rates was less likely. William Dudley, is seen as “dovish” but more importantly he is regarded as being close to Yellen on views on monetary policy and is a voting member of the FOMC. In an unscheduled interview, he said a September rise was “less compelling” in light of international developments which include global financial markets gyrations, the slowing Chinese economy and falling commodity prices. “From my perspective, at this moment, the decision to begin the normalisation process at the September FOMC meeting seems less compelling to me than it was a few weeks ago.” He added he hoped the US could raise rates this year but added the move would be data dependent in what has become a Federal Reserve mantra in recent months. He noted US data has been positive, citing improved August consumer confidence figures and good July new home sales. In another sign the Fed may delay the expected September rate rise, Kansas City Fed chief Esther George said the Fed should take a “wait and see” approach on hiking rates, although as non-voting member of the FOMC her view is perhaps less influential than Dudley’s.

26 August 2015

The spread on US high yield bonds above has blown out to levels last seen in 2012. Based on flows in exchange-traded funds (ETFs), high yield ETFs have experienced an exodus recently as investors jump to the safety of US Treasury bonds. Bonds with a credit rating below BBB- from S&P or Baa3 from Moody’s are colloquially known as below investment grade or “junk” bonds but their attraction to some investors lies in the high rate of interest paid on them. In the haste to get out of high yield ETFs, yields have shot up and the gap between junk bond yields and Treasury bonds yields has approached 650bps.

26 August 2015

Australian consumer confidence figures surged in July and US consumer confidence figures have been released showing a similar surge. The US Conference Board survey for August showed a bounce back to 101.5 after July’s drop to 93.4 which was a similar move to Australia’s bounce. The survey indicated US consumers had become more optimistic “primarily due to a more favourable appraisal of the labour market.”

Consumer confidence typically increases when the economy expands and decreases when the economy contracts. It is seen as an important indicator of an economy’s short term health and in Western countries an estimated 60-70% of economic activity, or GDP, is in the form of private sector consumption.

The last two months’ US figures are likely to be the result of the Greek crisis taking centre stage in late June and early July, and a subsequent resolution a few weeks later. However, the latest figures are the result of a survey ending 13 August and thus don’t include the latest bout of share market volatility and so there’s some chance consumer confidence may be affected in the next survey.

26 August 2015

The People’s Bank of China (PBoC) surprised markets by announcing cuts to the lending and deposit rates, while reducing the amount of capital banks most hold against loans. In a move normally made on a weekend, the one year lending rate and deposit rate was reduced by 25bps to 4.6% and 1.75% respectively and the bank reserve requirements was reduced from 18.5% to 18%.

The surprise cuts initially put a rocket under global equity markets and reversed the flow to bond markets. However, it was short lived and US equity markets ended the day in the red and Treasury bond yields falling. While the cuts were a surprise, the change in the reserve requirement had been discussed for weeks and were partially seen as form of quarantining the tightening effects of recent foreign exchange interventions by the PBoC.

Credit Suisse questioned the effectiveness of the measures on the real economy saying China’s attempt at replacing private investment with public investment was mistaken. However, the bank said injecting liquidity “after the interest rate and RRR cuts is another small step by the PBoC towards its goal of restoring market confidence.”

26 August 2015

The ABS preliminary estimates of the Australia’s June quarter trade deficit and terms of trade were published indicating a deterioration in Australia’s export earnings and prices received. The trade deficit widened to $9.6bn, more than double the March quarter figure of $4.7bn. Exports were down nearly 6% as prices and volumes slid, while imports volumes were steady. The terms of trade were down an estimated 4.3% and while export volumes fell they were still 7% higher than the June 2014 figure, while import volumes were close to those in June 2014.

25 August 2015

The index representing a basket of credit default swaps, iTraxx (series 23), has jumped to 115.3, a level not seen since October 2013. This period was the aftermath of the so-called ‘taper tantrum’ when bond markets were worried about the US Fed raising withdrawing its monetary stimulus by winding back its US$85bn a month bond buying programme.

Credit default swaps are essentially insurance contracts where buyers are paid out if a bond issuer defaults. These contracts are analogous to a house insurance: the insurance company will pay an owner of an insured house which has been destroyed by fire.

iTraxx is an index of credit default swap contracts over bonds issued by large, well-known companies such as BHP and the major banks. The index is rebalanced each March and September with the most active credit default swaps included in the index. The current iTraxx series is the 23rd.

An upward movement in the index indicates the cost of insuring against default by the issuers has gone up on average. This is often used by the market as a proxy for rising concerns about the likelihood of a corporate bond default. In general terms, the more negative the outlook on the economy is, the higher the risk of a corporate defaulting on its debt.

The iTraxx Australia index has been moving up since a low of 81 in March 2015 but recently the moves have become larger. In mid-August the index was at just over 100 points with typical movements of 1 or 2 points a day but with only a few days to the end of the month the index has jumped sharply to 115pts. This has been put down to rising fears of a slowdown in Chinese and global growth and the subsequent higher likelihood of a corporate bond default.

Read More:

What is iTraxx?