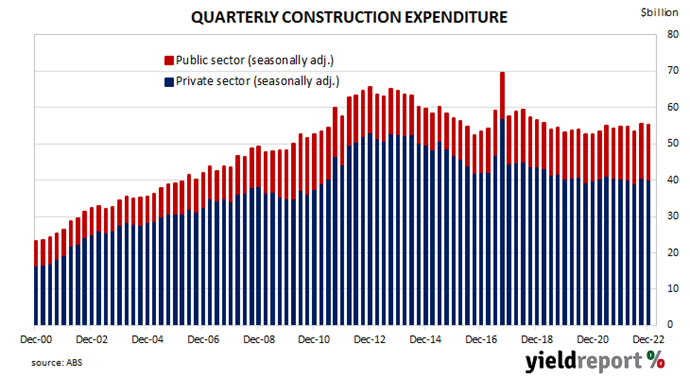

Summary: Construction spending down 0.4% in December quarter, contrasts with expected increase; constraints around output rather than shrinking demand; residential sector up 0.9%, non-residential building down 5.1%, engineering up 1.0%.

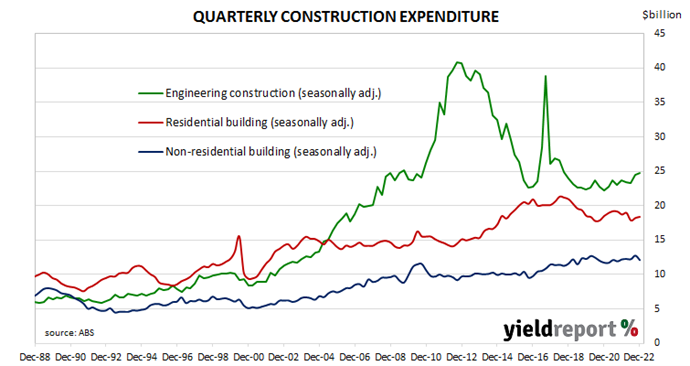

Construction expenditure increased substantially in Australia in the early part of last decade following a more-steady expansion through the 2000s. A large portion of the increase came from the commissioning of new projects and the expansion of existing ones to exploit a tripling in price of Australia’s mining exports in the previous decade. Growth rates began slowing in 2017 and the return to “normal” investment levels have now taken place.

According to the latest construction figures published by the ABS, total construction in the December quarter decreased by 0.4%. The fall was in contrast with the 1.5% increase which had been expected as well as the September quarter’s 3.7% increase after it was revised up from 2.2%. On an annual basis, the growth rate slowed from 2.4% to 1.0%.

“The decline was driven by a sharp fall in private non-residential construction, as well as a decline in private sector engineering work,” said ANZ senior economist Catherine Birch. “This is likely to be driven more by constraints around output rather than shrinking demand.”

Domestic Treasury bond yields increased moderately, lagging the noticeable rises of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had added 2bps to 3.59%, the 10-year yield had gained 6bps to 3.88% while the 20-year yield finished 4bps higher at 4.22%.

In the cash futures market, expectations regarding future rate rises softened. At the end of the day, contracts implied the cash rate would rise from the current rate of 3.33% to average 3.50% in March and then increase to an average of 3.905% in May. August contracts implied a 4.21% average cash while November contracts implied 4.205%.

Residential building construction expenditures rose by 0.9%, less than the September quarter’s 2.1% increase after revisions. On an annual basis, expenditure in this segment was 1.8% lower than the December 2021 quarter, up from the September quarter’s revised figure of -4.8%.

Non-residential building spending dropped by 5.1%, in contrast to the previous quarter’s 4.3% increase. On an annual basis, expenditures were 0.8% lower than the December 2021 quarter, whereas the September quarter’s comparable figure was +7.0% after revisions.

Engineering construction increased by 1.0% in the quarter, less than the 4.7% increase in the September quarter. On an annual basis, spending in this segment was 4.3% higher than the December 2021 quarter, down from the September quarter’s comparable figure of +5.9% after revisions.

Quarterly construction data compiled and released by the ABS are not considered to be of a “primary” nature, unlike unemployment (Labour Force) and inflation (CPI) figures. However, the figures are viewed by economists and analysts with interest as they directly feed into quarterly GDP figures.