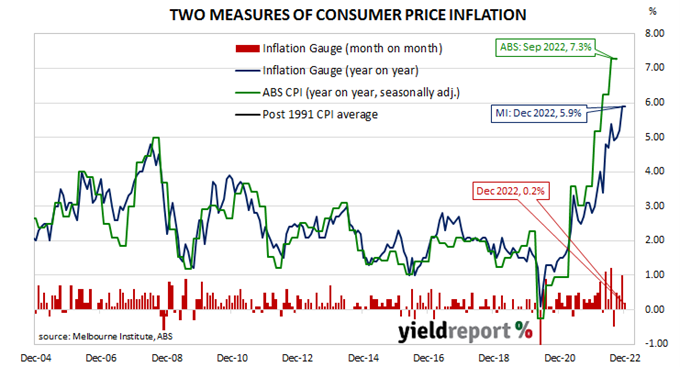

Summary: US core PCE price index up 0.3% in December, in line with expectations; annual rate slows from 4.7% to 4.4%; “all” in goods sector, “not broad-based”; Treasury yields mostly higher; Fed rate-rise expectations largely unchanged.

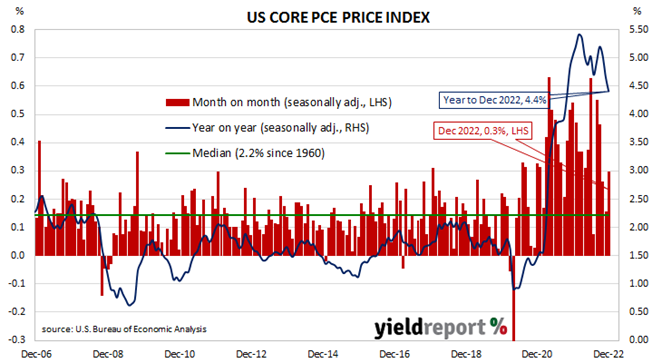

One of the US Fed’s favoured measures of inflation is the change in the core personal consumption expenditures (PCE) price index. After hitting the Fed’s target at the time of 2.0% in mid-2018, the annual rate then hovered in a range between 1.8% and 2.0% before it eased back to a range between 1.5% and 1.8% through 2019. It then plummeted below 1.0% in April 2020 before rising back to around 1.5% in the September quarter of that year. It has since increased significantly above the Fed’s target.

The latest figures have now been published by the Bureau of Economic Analysis as part of the December personal income and expenditures report. Core PCE prices rose by 0.3% over the month, in line with expectations but slightly higher than November’s 0.2%. On a 12-month basis, the core PCE inflation rate slowed from November’s revised rate of 4.7% to 4.4%.

“The fall in core inflation is all in the goods sector, not broad-based,” said ANZ economist Gregorius Steven.

US Treasury bond yields increased modestly on the day with the exception of those at the ultra-long end. By the close of business, the 2-year Treasury bond yield had inched up 1bp to 4.19%, the 10-year yield had added 2bps to 3.51% while the 30-year yield finished 2bps lower at 3.62%.

In terms of US Fed policy, expectations of higher federal funds rates over the next 12 months remained largely unchanged overall. At the close of business, contracts implied the effective federal funds rate would average 4.575% in February, 25bps higher than the current spot rate, and then climb to an average of 4.645% in March. May futures contracts implied a 4.885% average effective federal funds rate while December contracts implied 4.545%.

The core version of PCE strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It is not the only measure of inflation used by the Fed; the Fed also tracks the Consumer Price Index (CPI) and the Producer Price Index (PPI) from the Department of Labor. However, it is the one measure which is most often referred to in FOMC minutes.