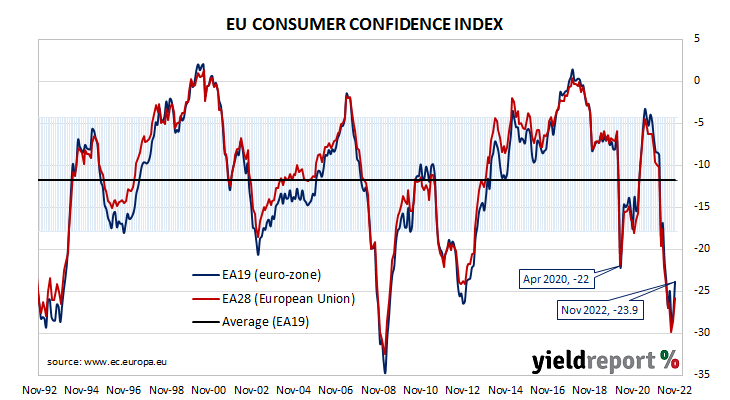

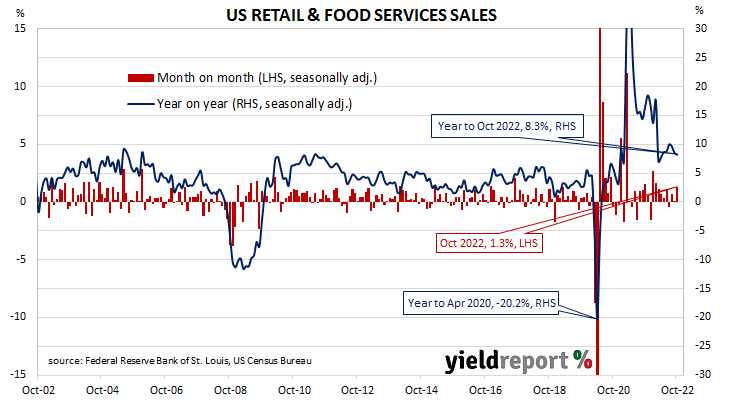

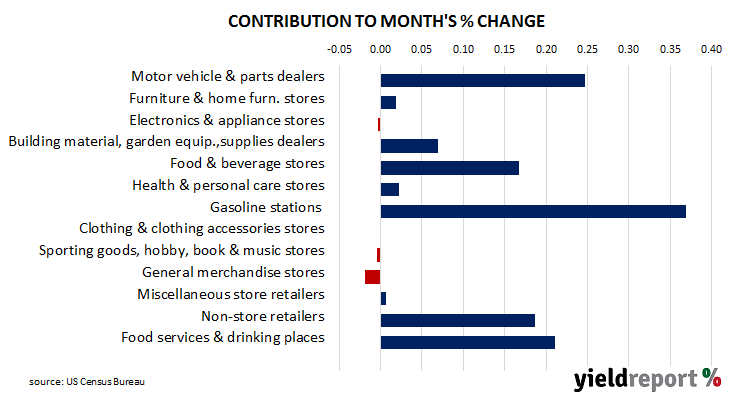

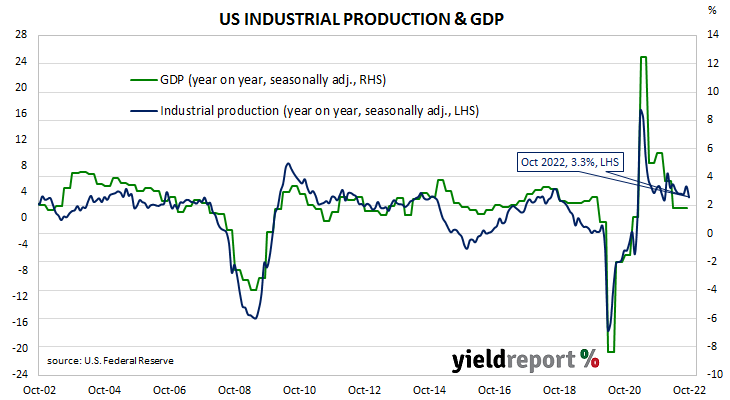

08 November 2022

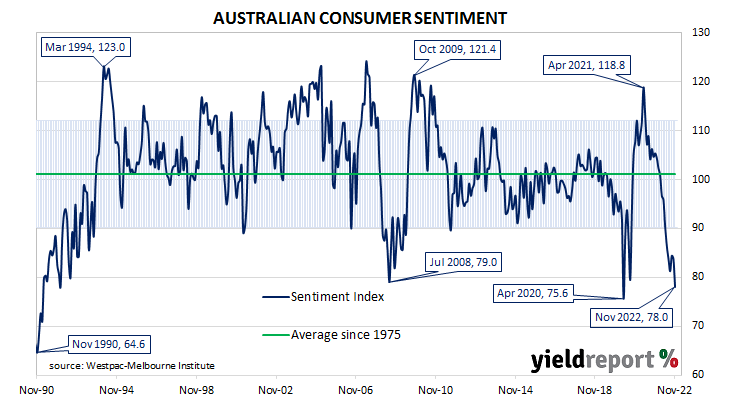

Summary: Household sentiment deteriorates again in November; only slightly higher than April 2020; rate increases, forecasts of higher electricity prices play roles in latest reading; UBS: “historically consistent” with falling real consumption; all five sub-indices lower; more respondents expecting higher jobless rate.

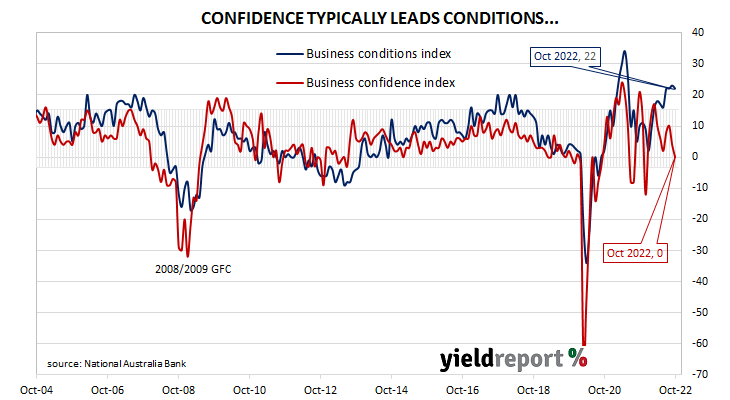

After a lengthy divergence between measures of consumer sentiment and business confidence in Australia which began in 2014, confidence readings of the two sectors converged again in mid-July 2018. Both measures then deteriorated gradually in trend terms, with consumer confidence leading the way. Household sentiment fell off a cliff in April 2020 but, after a few months of to-ing and fro-ing, it then staged a full recovery. However, consumer sentiment has deteriorated significantly over the past year, while business sentiment has been more robust.

According to the latest Westpac-Melbourne Institute survey conducted in the first week of November, household sentiment deteriorated again in November. Their Consumer Sentiment Index fell from October’s reading of 83.7 to 78.0, a reading which is well below the “normal” range and significantly lower than the long-term average reading of just over 101.

“Sentiment continues to plumb historic lows,” said Westpac Chief Economist Bill Evans. “This print of 78.0 is now below the low point of the GFC and only slightly higher than when the COVID pandemic first hit in April 2020. Prior to that, we need to go back to the deep recession in the early 1990s to find a weaker read.”

Any reading of the Consumer Sentiment Index below 100 indicates the number of consumers who are pessimistic is greater than the number of consumers who are optimistic.

Commonwealth Government bond yields moved substantially higher on the day, outpacing the overnight rises of their US Treasury counterparts. By the close of business, the 3-year ACGB yield had gained 14bps to 3.56% while 10-year and 20-year yield both finished 13bps higher at 4.05% and 4.40% respectively.

In the cash futures market, expectations regarding future rate rises firmed. At the end of the day, contracts implied the cash rate would rise from the current rate of 2.81% to average 2.995% in December and then increase to an average of 3.225% in February. May 2023 contracts implied a 3.815% average cash rate while August 2023 contracts implied 4.15%.

Evans noted respondents surveyed after the announcement of the RBA’s latest rate increase were generally more pessimistic than respondents surveyed prior to the announcement. However, he also suggested the Federal Budget may have played a part. “Consumers would also have been unnerved by forecasts in the Government’s October Budget showing electricity prices are expected to increase by 56% over the next two years.”

UBS economist George Tharenou expects pessimism in the household sector to eventually result in a fall in real household consumption figures. “At face value this is historically consistent with real consumption growth turning negative,” he said. “This indicates a very sharp slowing over coming months, albeit still likely only after the current very large boost from economic re-opening fades, which has been underpinned by a rapid drawdown of excess household savings.”

All five sub-indices registered lower readings, with the “Family finances – next 12 months” sub-index posting the largest monthly percentage loss.

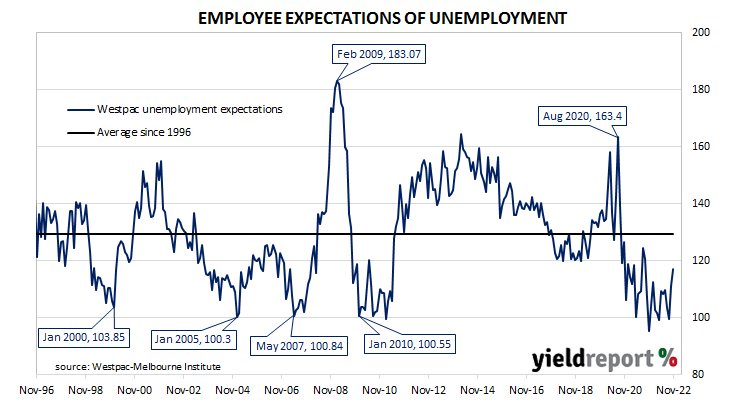

The Unemployment Expectations index, formerly a useful guide to RBA rate changes, rose from 111.3 to 117.3. Higher readings result from more respondents expecting a higher unemployment rate in the year ahead.