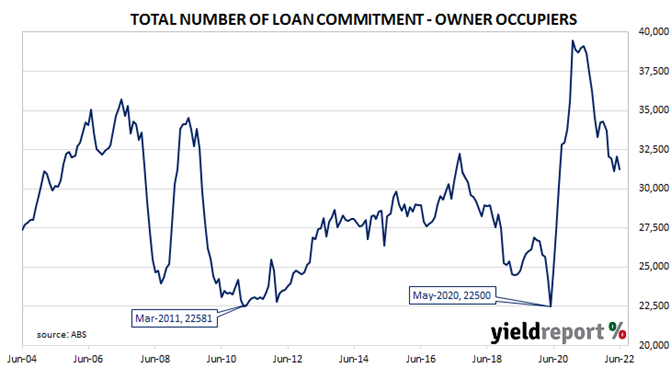

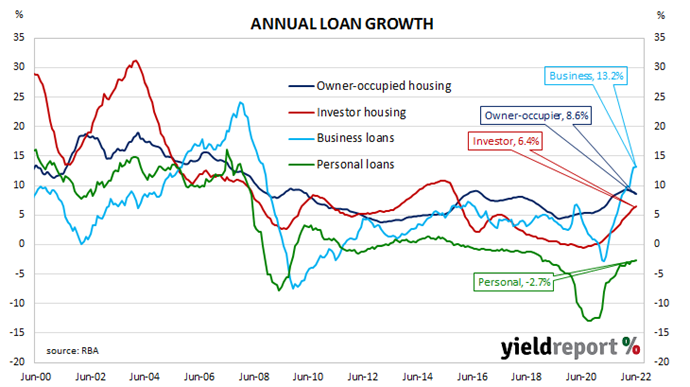

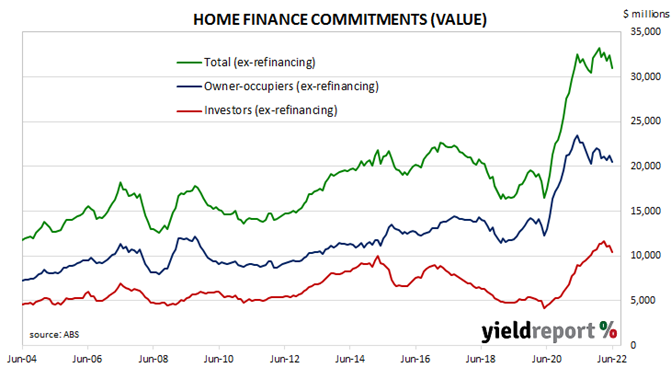

Summary: Value of loan commitments down 4.4% in June; “more significant declines to come”; holiday disruptions in April, May conceal “turning point”; value of owner-occupier loan approvals down 3.3%, investor approvals down 6.3%; number of home loan approvals down 2.6%.

After the RBA reduced its cash rate target in a series of cuts beginning in mid-2019 the number and value of approvals began to noticeably increase, potentially ending the downtrend which had been in place since mid-2017. Figures from February through to May of 2020 provided an indication the downtrend was still intact but subsequent figures then pushed both back to elevated levels in 2021.

June’s housing finance figures have now been released and total loan approvals excluding refinancing decreased by 4.4% In dollar terms over the month, slightly worse than the 3.0% fall which had been generally expected and in contrast with May’s +1.8%. On a year-on-year basis, total approvals excluding refinancing declined by 2.0%, down from the previous month’s comparable figure of -0.4%.

“Even sharper falls in the value of property sales since the start of the year point to more significant declines to come,” said Westpac senior economist Matthew Hassan.

Commonwealth Government bond yields fell significantly on the day, to some degree following the falls of US Treasury yields overnight. By the close of business, the 3-year ACGB yield had lost 9bps to 2.74%, the 10-year yield had shed 12bps to 3.00% while the 20-year yield finished 6bps lower at 3.37%.

“The ABS previously advised that the timing of public and school holidays disrupted approvals in previous months, with delays in April and a catch-up in May,” Hassan added. “That is likely concealing a turning point in activity.”

The total value of owner-occupier loan commitments excluding refinancing decreased by 3.3%, in contrast to May’s 2.2% increase. On an annual basis, owner-occupier loan commitments were 9.6% lower than in June 2021, the same as in May.

The total value of investor commitments excluding refinancing arrangements fell by 6.3%. The drop followed a 0.9% increase in May, taking the growth rate over the previous 12 months to 17.3%, down from 23.7% in May.

The total number of loan commitments (excluding refinancing loans) to owner-occupiers declined by 2.6% to 31,243. The decrease contrasted with May’s 3.0% rise and the annual contraction rate worsened slightly, from -18.0% to -19.2%.