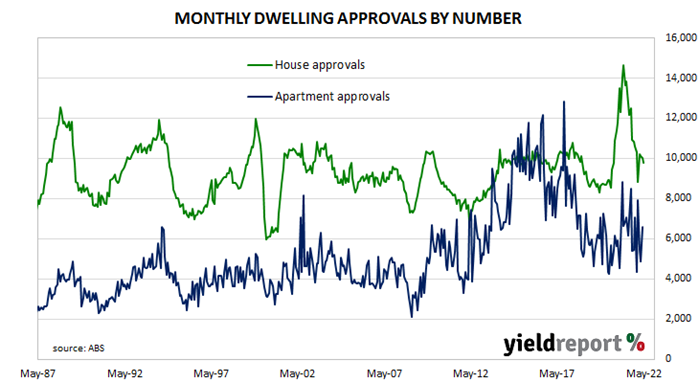

Summary: Value of loan commitments up 1.7% in May; housing downturn emerging; too early to see impact of May’s rate increase; value of owner-occupier loan approvals up 2.1%, investor approvals up 0.9%; number of home loan approvals up 2.9%.

After the RBA reduced its cash rate target in a series of cuts beginning in mid-2019 the number and value of approvals began to noticeably increase, potentially ending the downtrend which had been in place since mid-2017. Figures from February through to May of 2020 provided an indication the downtrend was still intact but subsequent figures then pushed both back to elevated levels.

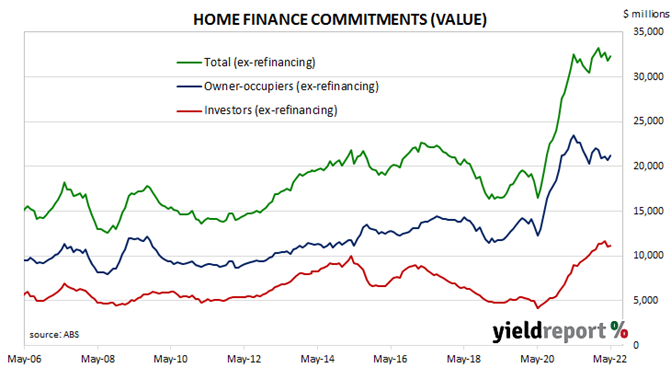

May’s housing finance figures have now been released and total loan approvals excluding refinancing increased by 1.7% In dollar terms over the month, in contrast to the 2.5% fall which had been generally expected as well as April’s -2.8%. On a year-on-year basis, total approvals excluding refinancing declined by 0.4%, down from the previous month’s comparable figure of +2.6%.

“The April and May results still leave in place a housing downturn emerging in 2022,” said Westpac senior economist Andrew Hanlan. “However, the rate of decline to date in official figures paints a more orderly adjustment than appeared to be the case a month ago.”

The figures were released on the same day as several other domestic data reports and Commonwealth Government bond yields fell modestly. By the close of business, the 3-year ACGB yield had shed 4bps to 3.16%, the 10-year yield had lost 3bps to 3.62% while the 20-year yield finished 2bps lower at 3.84%.

“It’s too early to see the impact of the RBA’s first rate hike since 2010 in these May numbers,” said ANZ senior economist Felicity Emmett. “But higher rates will eventually bite and drive housing finance and building approvals lower.”

The total value of owner-occupier loan commitments excluding refinancing increased by 2.1%, in contrast to April’s 1.7% decrease. On an annual basis, owner-occupier loan commitments were 9.7% lower than in May 2021, whereas April’s annual growth figure was -9.6%.

The total value of investor commitments excluding refinancing arrangements increased by 0.9%. The rise followed a 4.8% fall in April. On an annual basis, the value of loan commitments in the month was 23.7% higher than in May 2021, down from 37.1% in April.

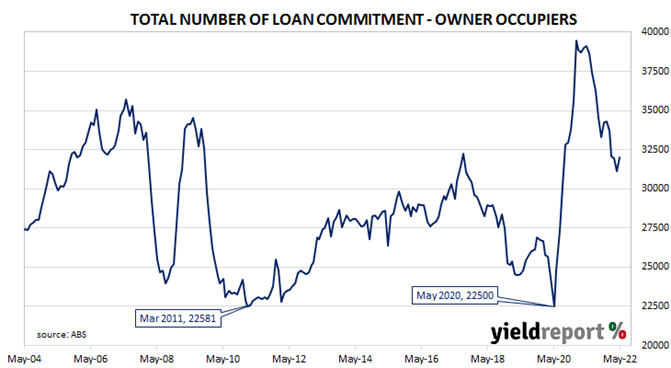

The total number of loan commitments (excluding refinancing loans) to owner-occupiers rose by 2.9% to 32,035. The increase contrasted with April’s 2.5% fall and the annual contraction rate eased slightly, from -20.1% in April to -18.1%.