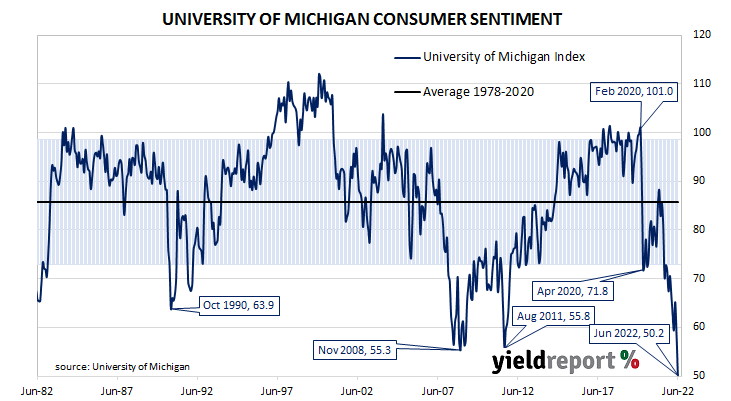

Summary: University of Michigan consumer confidence index down noticeably in June, below consensus expectations; views of present conditions, future conditions both deteriorate significantly; comparable to trough in 1980 recession.

US consumer confidence started 2020 at an elevated level but, after a few months, surveys began to reflect a growing unease with the global spread of COVID-19 and its reach into the US. Household confidence plunged in April 2020 and then recovered in a haphazard fashion, generally fluctuating at below-average levels according to the University of Michigan. The University’s measure of confidence had recovered back to the long-term average by April 2021 but then it plunged again in the September quarter. It has since fallen to historically low levels.

The latest survey conducted by the University indicates confidence among US households deteriorated noticeably on average in June. The preliminary reading of the Index of Consumer Sentiment registered 50.2, well below the generally expected figure of 58.9 as well as May’s final figure of 58.4. Consumers’ views of current conditions and expectations regarding future conditions both deteriorated significantly in comparison to those held at the time of the May survey.

“Consumer sentiment declined by 14% from May, continuing a downward trend over the last year and reaching its lowest recorded value, comparable to the trough reached in the middle of the 1980 recession,” said the University’s Surveys of Consumers chief economist, Richard Curtin. He noted gasoline prices “weighed heavily on consumers” with half of all respondents spontaneously mentioning higher prices during their interviews.

US Treasury bond yields rose materially on the day, although not at the ultra-long end. By the close of business, the 2-year Treasury yield had jumped 25bps to 3.07% and the 10-year yield had gained 11bps to 3.16%. The 30-year yield finished just 2bps higher at 3.19%.

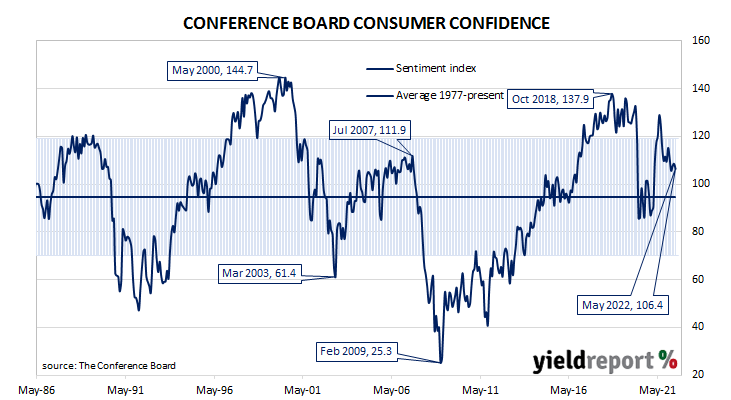

Less-confident households are generally inclined to spend less and save more; some decline in household spending could be expected to follow. As private consumption expenditures account for a majority of GDP in advanced economies, a lower rate of household spending growth would flow through to lower GDP growth if other GDP components did not compensate. However, the University’s survey is one of two widely-followed surveys, the other being produced by The Conference Board, and their indices have diverged markedly over the past two years.