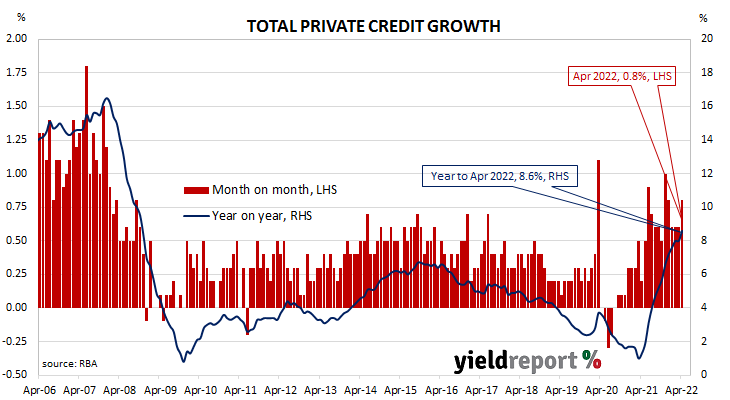

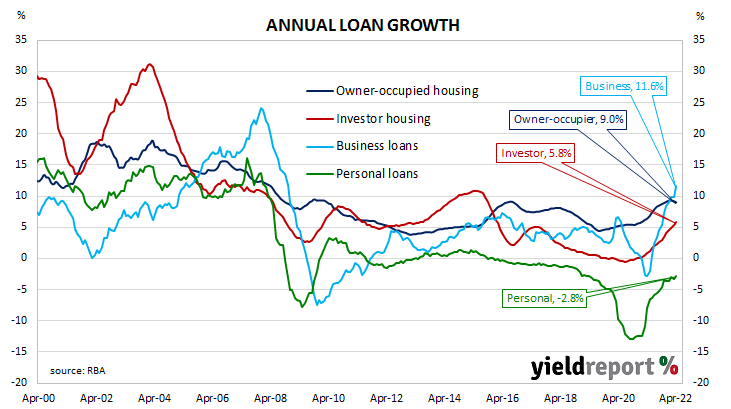

Summary: Private sector credit up 0.8% in April, above expectations; annual growth rate up from 8.0% to 8.6%; business loans account for about 50% of net growth.

The pace of lending to the non-bank private sector by financial institutions in Australia followed a steady-but-gradual downtrend from late-2015 through to early 2020 before hitting what appears to be a nadir in March 2021. That downtrend ended later in the same year and now annual growth rates are above the peak rate seen in the previous decade.

According to the latest RBA figures, private sector credit increased by 0.8% in April. The result was substantially greater than the 0.5% increase which had been generally expected and higher than March’s 0.6% increase after it was revised up from 0.4%. On an annual basis, the growth rate accelerated from March’s revised figure of 8.0% to 8.6%.

“The surprise again was business credit, which tends to be volatile month-to-month,” said NAB senior economist Tapas Strickland.

Commonwealth Government bond yields rose significantly on the day. By the close of business, the 3-year ACGB yield had gained 8bps to 2.93% while 10-year and 20-year yields both finished 10bps higher at 3.37% and 3.69% respectively.

In the cash futures market, expectations of a steeper path for the actual cash rate over time firmed. At the end of the day, contract prices implied the cash rate, currently at 0.31%, would rise to 0.59% in June and then rise to 1.36% by August. May 2023 contracts implied a cash rate of 3.345%, 302bps above the current cash rate.

Business loans accounted for a little over 50% of the net growth over the month, while owner-occupier loans and investor loans accounted for most of the balance. Total personal debt increased a touch.

The traditional driver of loan growth rates, the owner-occupier segment, grew by 0.6% over the month, in line with March’s increase. The sector’s 12-month growth rate slowed from 9.2% to 9.0%.

Total lending in the business sector jumped by 1.4%, up from the 0.6% increase recorded in March. Growth on an annual basis accelerated from 9.9% to 11.6%.

Monthly growth in the investor-lending segment slowed to a halt in early 2018. Shortly into the 2019/20 financial year, monthly growth rates slipped into the red before posting a series of flat or near-flat results until mid-2020.

In April, net lending grew by 0.6%, in line with March’s increase. The 12-month growth rate accelerated from 5.3% to 5.8%.

Total personal loans expanded by 0.3%, up from March’s 0.1% contraction, taking the annual contraction rate from 3.3% to 2.8%. This category of debt includes fixed-term loans for large personal expenditures, credit cards and other revolving credit facilities.