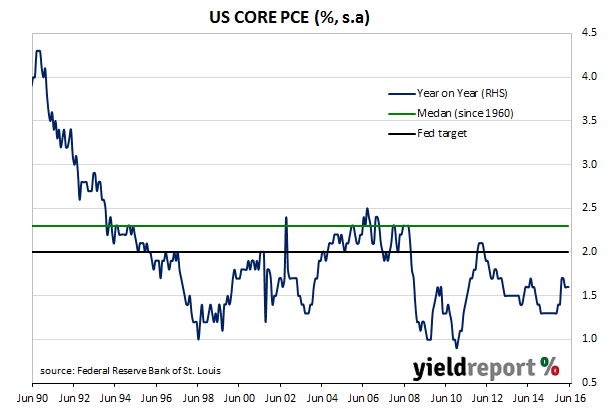

The US Fed takes into consideration several price indices when evaluating the rate of inflation. It says it does so because “various indexes (sic) can send diverse signals about inflation”. One of its favoured measures of inflation is the core personal consumption expenditure. The core version of consumer spending strips out energy and food components, which are volatile from month to month, in an attempt to identify the prevailing trend. It’s not the only measure of inflation used; the Fed also tracks the Consumer Price Index (CPI) and Producer Price Index (PPI) from the Department of Labor. Its view of inflation is important as it forms the basis for the FOMC’s interest rate settings.

The latest core PCE figures have been published by the Bureau of Economic Analysis as part of May figures for personal income and expenditures. At 0.2% for the month and 1.6% year on year, they came in as expected. Even though the data was in line with expectations, ANZ Research viewed the numbers as more on the positive side. “Overall, the data suggest the US consumer remains in a healthy position. Rising incomes, coupled with elevated consumer confidence….bode well for spending in the second half of the year – as long as Brexit fears continue to fade.” Other views were more neutral. St George senior economist Janu Chan said, “We would need to see a further pickup to give the Fed greater confidence that inflation is moving towards their 2% target.” AMP Capital’s Shane Oliver viewed the data as giving the Fed “plenty of flexibility to keep delaying on rates“.

According to US cash futures markets there no chance of a rate rise in July and perhaps remarkably, a small chance of a rate cut. US 2 year bond yields finished the day 3bps higher at 0.64% while 10 year bonds yields finished 5bps higher at 1.52%.