Summary:

Australian Bond Market

-

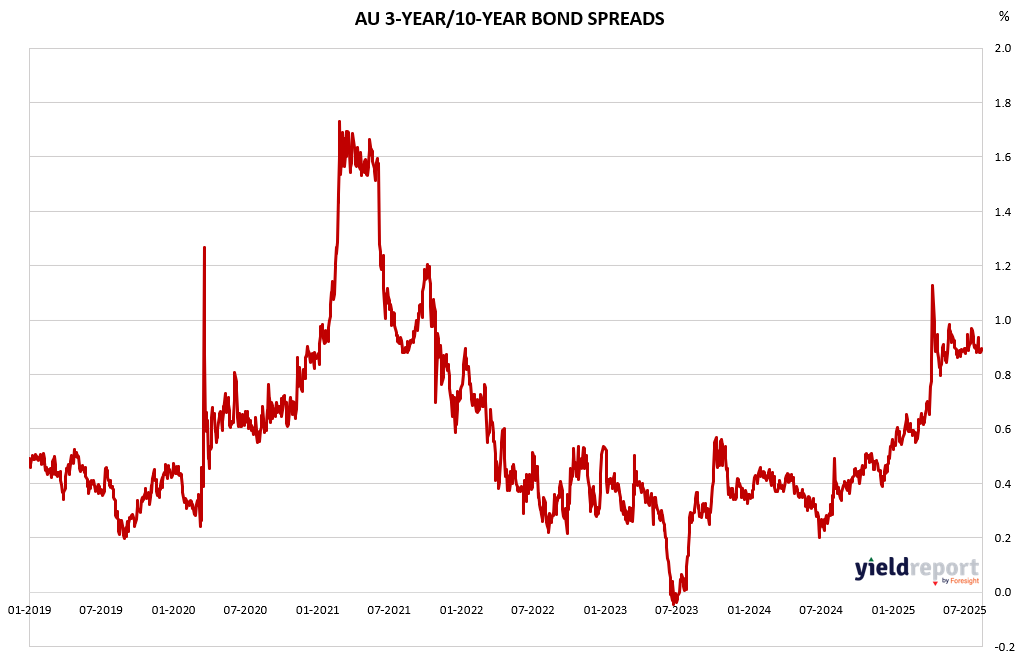

The Aussie yield curve nudged upward across the board, especially at the long end. Rising wage growth—0.8% quarterly and 3.4% annually—suggests inflation pressures remain sticky, even after the RBA cut rates to 3.6%

-

Markets had anticipated further easing, but stronger-than-expected wages and subdued employment tempered that outlook/

-

That said, CPI inflation is still cooling into the RBA’s 2–3% target zone, reinforcing expectations of only gradual easing in the coming months

US Treasury Market

-

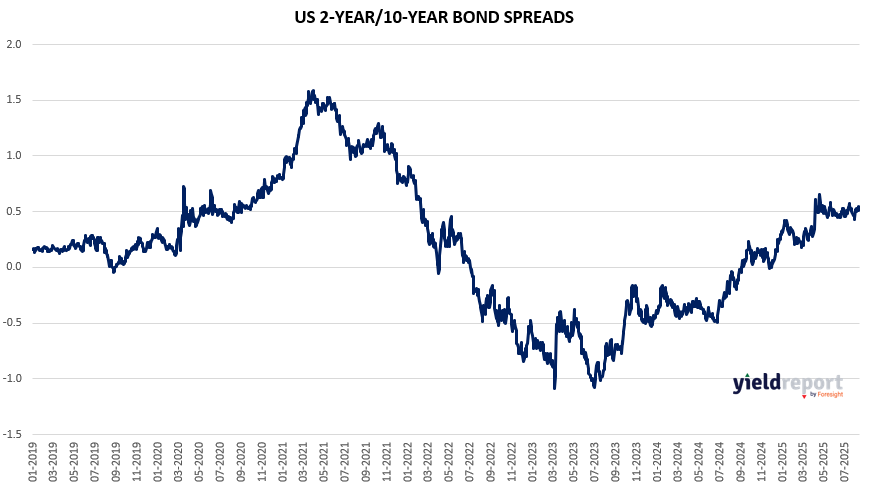

Treasury yields across maturities edged higher, driven by a mix of persistent inflation signals and mixed data on growth and activity.

-

Despite hopes for rate cuts, moderating—but still elevated—inflation (Core CPI at 3.1% annual and 0.3% monthly) is keeping markets cautious.

-

Meanwhile, factors like ongoing debt issuance and geopolitics continue to add volatility and upward pressure on yields.

Figure 1: Australia 3 and 10-year Bond Yield Spread

Figure 2: US 2 and 10-year Bond Spread

To learn more about yield curves and their predictive power, visit this article or this one.