Summary:

While there has been a backup in the 2-year as the market has reset Fed cuts, the term premium actually further rose this week. Why? – a combination of longer term fiscal concerns and policy uncertainty. And Friday’s after market move by Moody’s, lowering the US credit score to Aa1 from Aaa, will almost inevitably lead to a further steepening the curve this week. How could it not.

In fact, if you look at the curve, it should steepen over the next six to 18 months because the front end will eventually follow the Fed cuts. In contrast, the long end there is likely only a modest reduction from here because of the budget deficit issues.

Essentially, bond managers are requiring higher yields on longer maturities, with the term premium at its highest since 2014, and are becoming more cautious in their investments, favouring shorter maturities and limiting their exposure to longer-term bonds. In the new world order, call it the Fear of the Long Bond. And we can’t see that changing over the foreseeable future, and partly because the demand is increasingly moving to the front and circa 5-year part of the curve. In fact, the yield curve will likely steepen from here. If it does, obviously long-end yields will start to become more attractive.

Beyond last week and more broadly, rates on the long-end of the yield curve have risen steadily since the April 2nd tariff announcement, with 30-year nominal rates climbing 27bps and real 30-year rates popping 36bps. The dramatic move in the long-end of the curve has seen 10-year term premium push up to 10-year highs. Some of the move may be attributable to positioning and other temporary factors – the notable plunge in prime brokerage leverage data and the sharp move towards even more deeply negative swap spreads are consistent with the unwind of levered curve bets by hedge funds and other speculative actors. However, there are reasons to believe that long rates may continue to be volatile or even move higher, including a continued deterioration in the fiscal outlook, as noted above.

While the unwind of leveraged curve trades has sparked a sell-off on the long-end and a steepening of the yield curve, the front-end of the curve (0 to 5 years) has stayed elevated and relatively flat. Many fixed income managers believe that income and carry look attractive on the front end of the Treasury curve as well as in select corporate credits is the more attractive part of the curve.

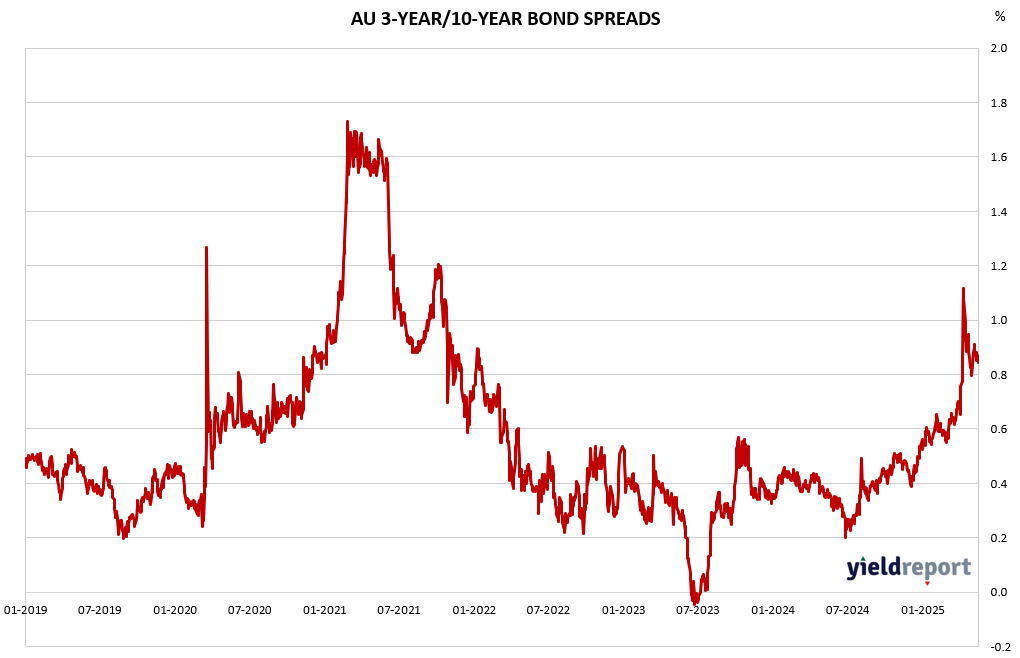

Exhibit 1: Australian 10-yr minus 3-year Spread |

Exhibit 2 : US 10-yr minus US 2-yr Spread |

To find out more about the yield curve and its usefulness, click here or here.