Summary:

Well, given Wednesday’s events, the term premium on US treasuries, which has been rising for weeks now, jumped higher this week. On Wednesday 21 May, the US term premium hit 0.92, a level not seen for over a decade going back to the beginning of 2014. The US term premium has now been on an upward trend for 18-months, starting from December 2023. The curve is likely to steepen further over the next six to 18 months because the front end will eventually follow the Fed cuts. In contrast, in the long end there is likely only a modest reduction from here because of the budget deficit issues and what appears to be a supply/demand mismatch. So, unless the treasury cuts back on long-end issuance, the curve can continue to steepen.

For those following the markets closely, it has been clear for all of 2025 that bond managers are favouring the shorter end of the curve (0-3 year) or the belly of the curve (5-7 years). This weight of money, or movement out the long-end, in itself may prove self-reinforcing. And given the current risks at the long-end, higher yields are likely required to entice bond investors back to that part of the curve. All in all, not great news for the real economy / main street nor is it great news for the US government’s interest expense payments.

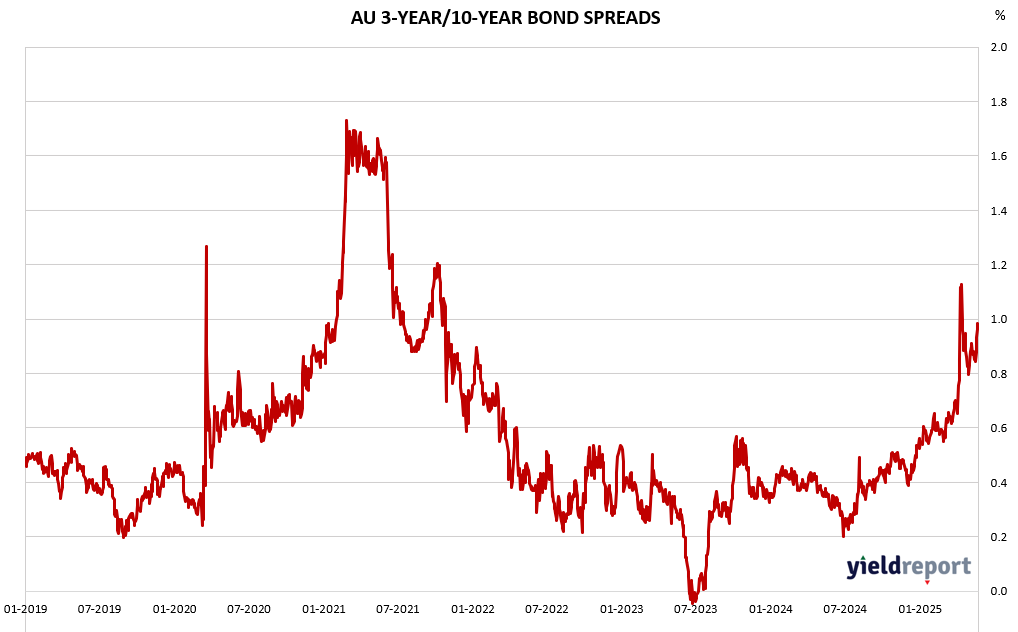

Exhibit 1: Australian 10-yr minus 3-year Spread |

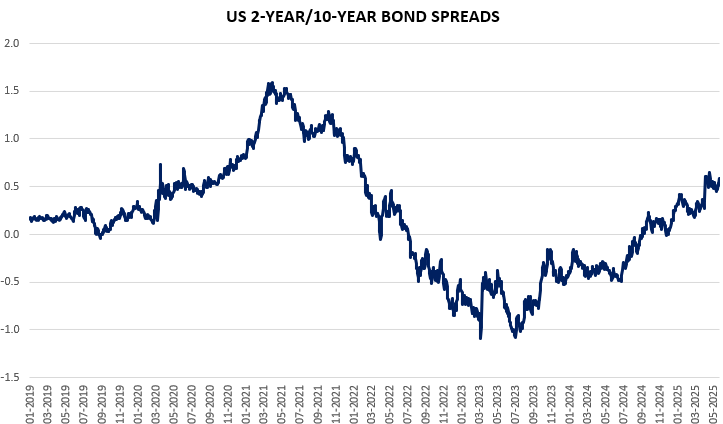

Exhibit 2 : US 10-yr minus US 2-yr Spread |

To find out more about the yield curve and its usefulness, click here or here.