Summary:

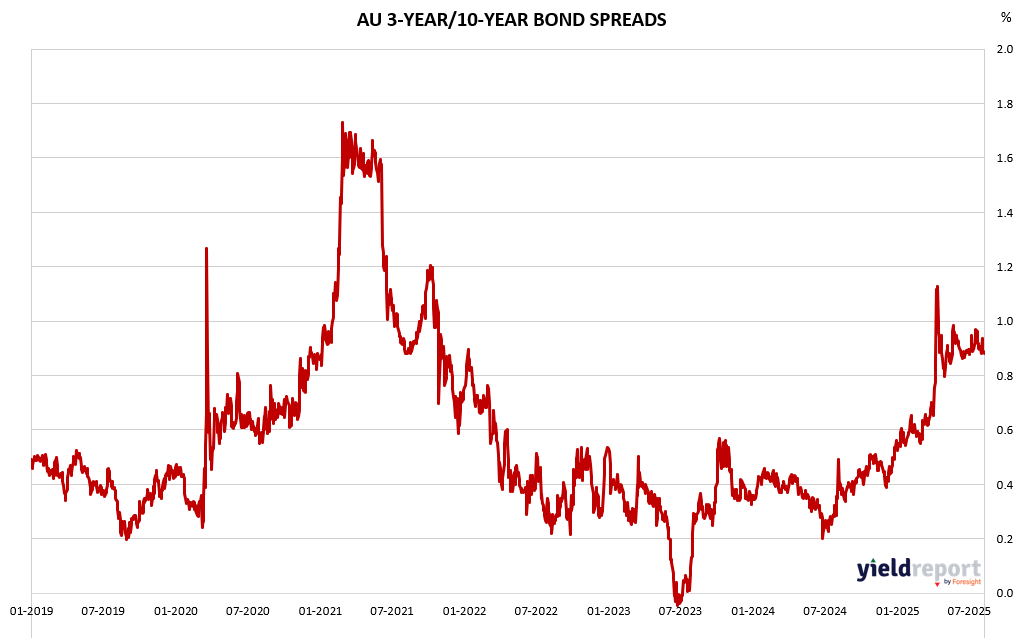

The Australian yield curve showed subtle but meaningful shifts this week, reflecting evolving market expectations around inflation, monetary policy, and global economic sentiment. The spread between 3-year and 10-year government bond yields narrowed slightly, suggesting a cautious recalibration of long-term growth and inflation outlooks.

Key Observations

- 3-Year vs 10-Year Spread: The yield spread between 3-year and 10-year bonds compressed modestly, indicating a flattening curve. This often signals investor uncertainty or a transition phase in monetary policy expectations.

- Short-Term Yields: Yields at the short end of the curve remained relatively stable, anchored by the Reserve Bank of Australia’s current cash rate stance. The market appears to be pricing in a pause in rate hikes, with inflation data showing signs of moderation.

- Long-Term Yields: The 10-year yield edged lower, reflecting subdued long-term inflation expectations and possibly increased demand for longer-duration assets amid global risk aversion.

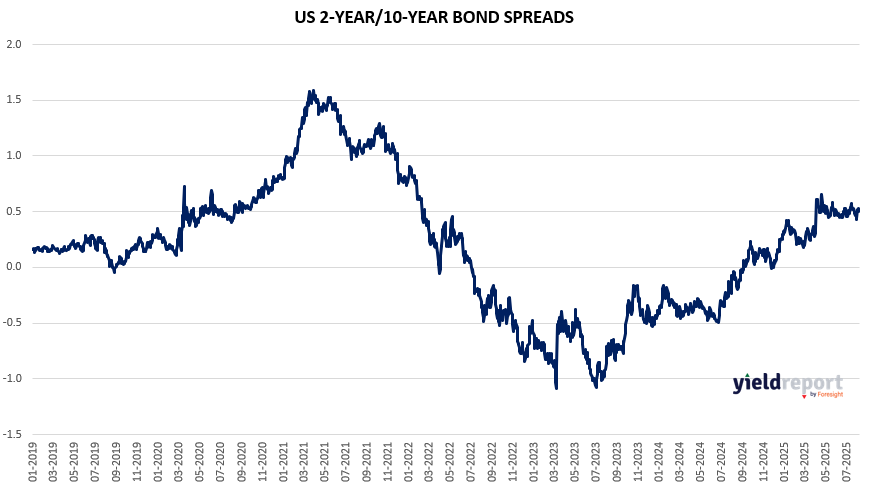

- Global Comparison: The US 2s10s spread remains deeply inverted, contrasting with Australia’s flatter but still upward-sloping curve. This divergence underscores differing macroeconomic trajectories and central bank strategies.

Figure 1: Australia 3 and 10-year Bond Yield Spread

Figure 2: US 2 and 10-year Bond Spread

To learn more about yield curves and their predictive power, visit this article or this one.