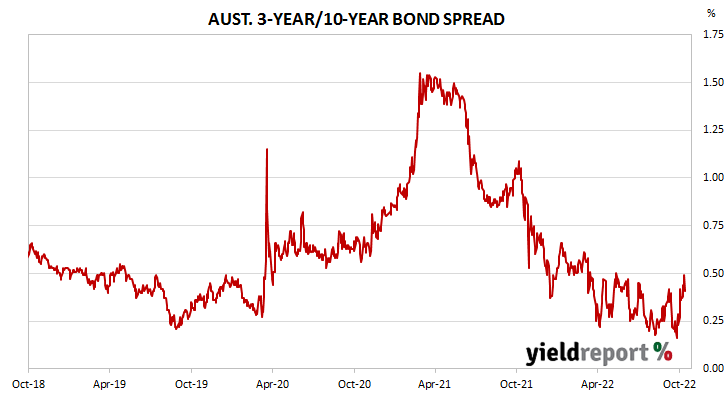

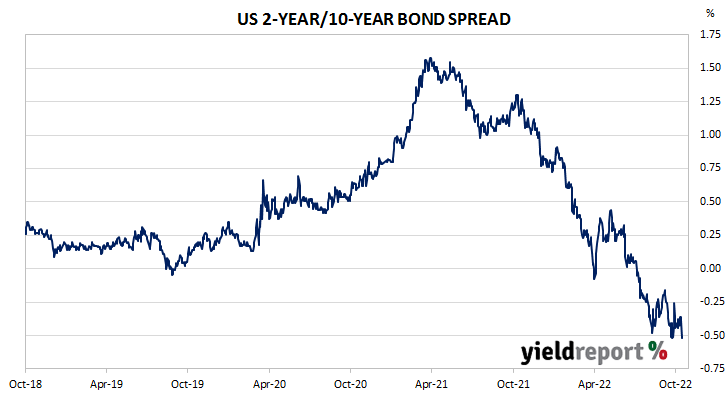

Summary: ACGB curve steeper; US Treasury curve more negative.

The gradient of the ACGB yield curve became steeper as yields rose by greater amounts at the long end than at the short end. By the end of the week, the 3-year/10-year spread had gained 4bps to 41bps while the 3/20 year spread finished 7bps higher at 69bps.

The traditional measures of the gradient of the US Treasury curve became more negative. The 2-year/10-year spread shed 9bps to -52bps over the week while the 2 year/30 year spread lost 7bps to -54bps. The San Francisco Fed’s favoured recession-predicting measure, the 3-month/10-year Treasury spread, finished 27bps narrower at +23bps.

To find out more about the yield curve and its usefulness, click here or here.