Summary: Slope of ACGB curve almost unchanged; US Treasury curve gradient more inverted.

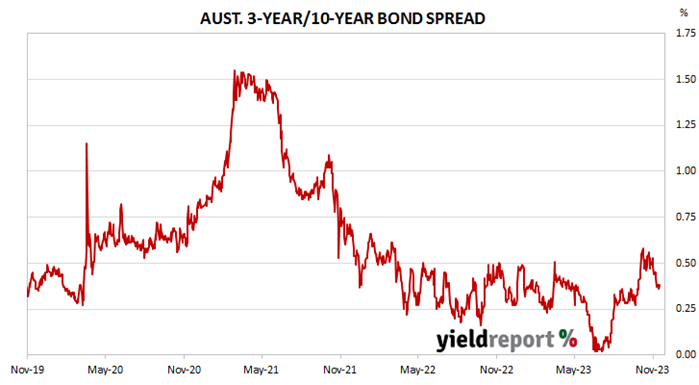

The gradient of the ACGB yield curve barely changed as yields fell. By the end of the week, the 3-year/10-year spread had returned to its starting point at 38bps while the 3/20 year spread finished 1bp higher at 70bps.

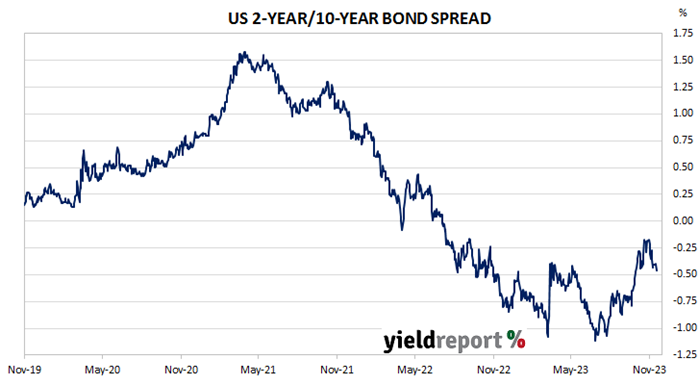

The gradient of the US Treasury curve became more inverted again this week. The 2-year/10-year spread lost 5bps to -46bps while the 2 year/30 year spread finished 2bps lower at -31bps. The San Francisco Fed’s favoured recession-predicting measure, the 3-month/10-year Treasury spread, finished 20bps lower at -93bps.

To find out more about the yield curve and its usefulness, click here or here.