Summary: ACGB bond yields down in Australia; ACGB 10-year spread to US Treasury yield rises to +13bps; 10-year bond yields down in US, major European markets; $3.5 billion of bonds, notes issued by AOFM.

Locally, long-term ACGB yields see-sawed in modest way through much of the week. By the end of it, 3-year and 10-year ACGB yields had both slipped 1bp to 3.53% and 3.93% respectively while the 20-year yield finished unchanged at 4.32%. The spread between US and Australian 10-year Treasury bond yields rose from +6bps to +13bps.

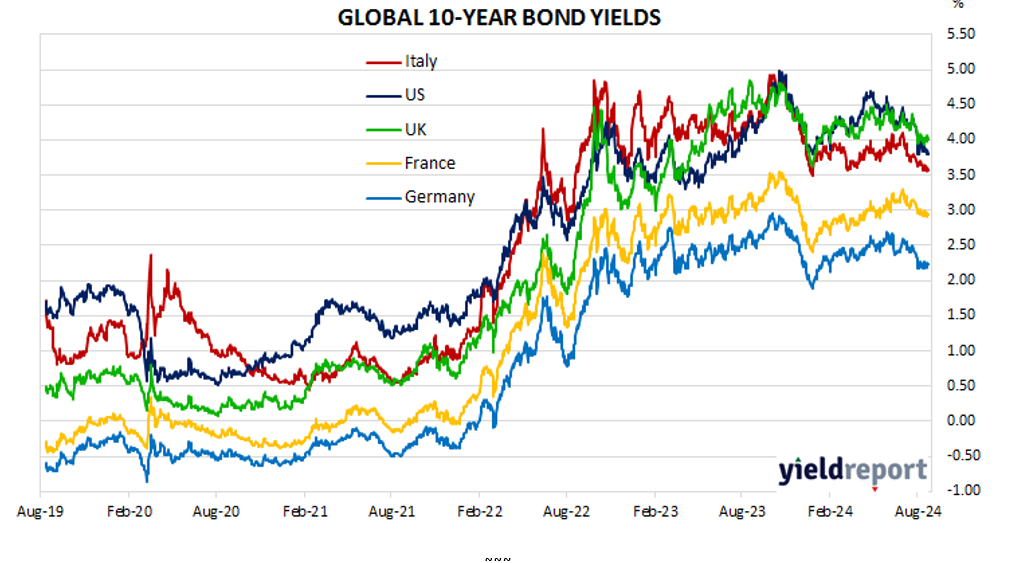

Over in the US, 10-year bond yields fell each day of the week with one exception, the exception being Thursday when yields rose moderately.

The Conference Board’s July reading of its Leading Index posted a 0.6% fall at the start of the week, another decline in a long list of them since early 2022.

Minutes of the FOMC July meeting came out midweek. They indicated the FOMC will almost certainly move to cut its federal funds target range next month.

S&P Global’s August flash reading of its US composite index were released the next day, posting a small decline from 54.3 in July to 54.1. The manufacturing index decreased from 49.6 to 48.0 while the services index increased from 55.0 to 55.2. S&P Global Market Intelligence Chief Business Economist Chris Williamson noted “inflation is continuing to slowly return to normal levels and that the economy is at risk of slowing amid imbalances.”

The New York Fed’s Nowcast model was updated at the end of the week as usual. The September 2024 quarter forecast was raised from 1.8% (annualised) to 1.9%.

By this point, the US 2-year Treasury bond yield had shed 14bps to 3.91%, the 10-year had lost 8bps to 3.80% while the 30-year yield finished 5bps lower at 4.09%.

In major euro-zone markets, 10-year bond yields moved in a similar fashion to their US counterpart.

S&P Global released its August flash PMI figures for the euro-zone on Thursday. The preliminary reading of the composite index was 51.2,up from July’s final reading of 50.2. “It’s a tale of two worlds. The manufacturing sector remains mired in recession, while the services sector still appears to be growing at a decent clip.”

By the end of the week, the German 10-year bund yield had lost 2bps to 2.23% while the French 10-year OAT yield shed 6bps to 2.93%. The Italian 10-year BTP yield ended up 7bps lower at 3.57% while the British 10-year gilt yield finished 2bps lower at 4.01%.

The AOFM held two vanilla bond tenders this week. $800 million of November 2033s and $700 million of November 2028s were priced at nominal yields of 3.87% and 3.55% respectively. The usual two Treasury note tenders also raised $2.0 billion on a short-term basis.

The gross value of all bonds issued by the AOFM in the 2024/2025 financial year (not taking into account short-term Treasury note tenders) is $22.30 billion. There are currently $859.85 billion of Treasury bonds and $41.285 billion of Treasury index-linked bonds on issue. The next series to mature does so on 21 November 2024 when $41.30 billion worth of bonds are due. There are also $26.00 billion of short-term Treasury notes outstanding.